A sampling of interesting observations from the Haymaker’s network of market experts and favorite resources.

#1: Grant’s Interest Rate Observer’s Jim Grant quoting banking expert Chris Whalen:

GIRO

…(i)f you include the loan portfolio of U.S. banks in the capital calculation, then most U.S. banks today are insolvent on a fair value, mark-to-market basis because of the FOMC’s actions.

Team Haymaker Take: In recent months I’ve become a big fan of Chris Whalen’s work. He was one of the first to go on record that rocketing interest rates would cause convulsions for the U.S. banking system. When he says “FOMC” he’s referring to the Fed and its open market committee that sets its benchmark rate. He’s got a point in blaming our omnipotent, but far from omniscient, central bank. Its incontinent monetary policies flooded the banks with trillions of deposits for which they needed to find a home. Loan demand was nowhere near large enough to absorb that liquidity.

Consequently, most went into super-safe U.S. government bonds. At least they were safe until the Fed jacked up interest rates at the steepest rate since the early 1980s. This was after assuring the world in 2021 that rates would be held down for years to come. As a result, three of the largest bank failures in U.S. history occurred, with their combined assets equaling $550 billion or roughly 2% of GDP. This is not that much lower than the 2008 Global Financial Crisis when banks with assets equal to around 2½% of GDP failed. Ominously, TheWall Street Journal has reported that over 500 banks have losses on their books even greater than the late, not so great, SVB Financial (the former Silicon Valley Bank).

#2: From Down Under Daily’s Gerard Minack:

“Rate cuts never prevent equities from falling in a recession.”

Team Haymaker Take: How’s that for short but not very sweet? It’s one of those common knowledge myths that as soon as the Fed cuts rates, the stock market rips to the upside. But Gerard is making a crucial point. If there is a soft landing, that’s often the case (see 1995 and 2019). But if it’s a jarring collision with terra firma, the outcome is very different. Just consider what happened in 2000 to 2002 and from mid-2007 until the first quarter of 2009: the Fed was frantically cutting rates in both instances and stocks tanked regardless. In both cases, a recession occurred, though the one in 2001 was comparatively mild. (However, it was enough to scare the Fed into driving interest rates down to Great Depression levels, creating Bubble 2.0 in housing and, ultimately, the Great Recession and Global Financial Crisis.) This is why the recession/no recession debate is of such vital importance.

From my vantage, the economic data indicate a contraction is nigh despite that the massive services portion of the economy is holding up decently well. This is often the situation when a recession is in its infancy, however. The recurring pattern has been that the economy’s manufacturing/industrial segment leads on the way up… and the way down. By the way, despite his genetically sunny disposition, Gerard also sees a U.S. recession on the horizon. Hopefully, he and I are wrong while Jay Powell and Janet Yellen are right. Then again, the latter two’s forecasting record is just this side of atrocious.

#3: David Rosenberg, Arguing Against the Resurgent View That a Soft Landing Is Probable (Possibly Even a No-Landing Scenario):

BWD

This is something else that nobody talked about yesterday: real Gross Domestic Income (GDI) contracted at a 2.3% annual rate in the first quarter. That followed a 3.3% retreat in Q4 of last year. Not once back to 1950 have we ever failed to experience an NBER-defined recession with such back-to-back declines. (emphasis added)

When you average out both real GDP and GDI, this metric came in at a -0.5% annual rate in Q1 on top of -0.4% in 2022Q4 — not to mention slipping in four of the past five quarters. Once again, never before have we failed to see a recession with such a dynamic. Will it really be different this time?

Team Haymaker Take: As I’ve previously admitted, this may be the most challenging time I’ve experienced in my financial industry career, which stretches back to Jimmy Carter’s presidency, when it comes to discerning where the economy is headed. Despite David Rosenberg’s factoids above, plenty of strong data continue to be reported. This includes upward GDP revisions and an improving trend by initial claims for unemployment. Since the latter is a forward-looking measure of the otherwise rearview-mirror-oriented labor statistics, that’s a noteworthy positive.

Perhaps perfectly illustrating the economy’s present split-personality nature is the Chicago Fed’s National Activity Index. It is key because it covers some 85 different indicators. Accordingly, it is one of the most comprehensive snapshots of economic vitality — or the lack thereof. It rose slightly in April, contrary to expectations of another decline. However, March was revised meaningfully lower, almost fully offsetting the upside surprise. But what really caught my eye was Costco’s average transaction. Its ticket size fell 3½% in the U.S. and 4.2% globally. The company’s CFO also noted that COST customers are downshifting from more expensive discretionary items into cheaper “essentials”. This reflects a pattern being reported by most retailers, outside of the luxury segment.

#4: From Luke Gromen, Author of Forest For The Trees

FFTT

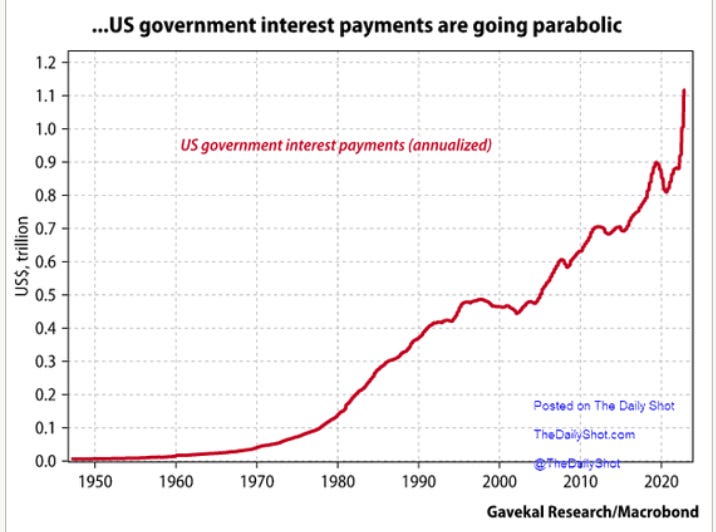

1. Treasury inexplicably decided not to term out as much debt as possible when the 10y (year T-note) yield was below 1.5% for most of the 22-month span from February 2020 to December 2021.

2. US debt and deficits have become so large relative to “large patient investor” demand (foreign Central Banks, large pensions and insurers) that the only part of the UST yield curve liquid enough for the US Treasury to finance such large deficits is at the short-end, (dominated by) increasingly fickle creditors like hedge funds and traders…

…history is very clear that when debt gets this high, it is eventually inflated away as a % of GDP.

Team Haymaker Take: Luke is spot-on when he criticizes the Treasury — and, implicitly, its head honcho, Janet Yellen — for whiffing on the chance to “term out” its financing needs when rates were 1½%, or lower, during the pandemic. (This phrase refers to extending maturities far out into the future, like 10 years or more.) As a result of this policy failure, the Treasury is facing a mountain of maturities over the next few years. Accordingly, with rates having more than doubled at the longer end, and up by 10 times on the shorter end, the U.S. government’s interest outlays will continue to do an Nvidia (the stock market equivalent of a moonshot). This elevates the odds of one of my scariest scenarios — a Federal Fiscal Funding Fiasco, the dreaded 4Fs — will occur in this year’s second half. Sustainable stock rallies and extreme Treasury market dysfunction don’t go hand-in-hand. Rather, we may be looking at some serious hand-to-hand combat between bulls and bears, with the latter likely to come out on top.

To learn more about Evergreen Gavekal, where the Haymaker himself serves as Co-CIO, click below.

#5: The Wall Street Journal on Houses, Apartments & Bonds

WSJ

Defaults are rising for a niche mortgage bond used primarily to fund apartment-building purchases, another sign that rising interest rates are upending the property sector.

This product, known as commercial real estate collateralized loan obligations, or CLOs, are mortgages packaged into bonds that are sold to investors. These mortgages helped fuel the rise in housing costs across Sunbelt states such as Arizona, Texas and Nevada, facilitating the purchase of buildings where property owners saw opportunities to raise rents.

Rental apartments accounted for two-thirds of these CLOs issued in 2021 and 81% of those issued in 2022, according to real-estate data firm Trepp.

The mortgages associated with CLOs appeal to property owners because they can put down less equity and take on more debt than with bank mortgages. They also have shorter terms and floating interest rates that make it easier for owners to sell or refinance their buildings after a few years.

But some of the same characteristics that made these loans attractive to property owners also made them riskier and more vulnerable to sudden changes in borrowing rates. Last year’s surge in interest rates, a softening rental market and rising expenses mean many landlords no longer earn enough money to pay back their loans.

Team Haymaker Take: So, what are the landlords to do? The economy, the Federal reserve, inflation, and a host of other interlocking variables appear collectively intent on creating confusion in a market that seemed pretty easy to forecast a couple of years ago. Housing was in short supply, interest rates were stable at next to nothing, and many among the middle-class were just looking for stable, quality housing, even if that meant signing on for a long-term apartment lease. But the nation’s residential chessboard has seen a few pieces move, and others leave, meaning the calculation that once warranted bold rental property expansion, even as recently as early 2022, just doesn’t make sense at the moment.

Taken on its own, this has the look of an economic woe that will sort itself out as rent prices and rent payers inevitably reach a loose equilibrium. But taken instead as part of the market confusion that’s frozen activity on the home-buying/selling side of things, there’s reason to wonder if more misery is ahead for those who just want some indication as to what the market signals are trying to say. If apartment investors are uncertain, what on earth does that mean for apartment residents?

The days of the big city auto show luring in potential buyers with high-priced dream machines to sell them reasonably priced cars are gone. Now reasonable options are priced high enough to make wallets groan.

According to the latest data from the car consumer guide Edmunds, the average transaction price for a new vehicle was $47,713; that’s a third more than what Americans paid five years ago. “We’ve come to this where you look out there in the field, and there are so few options that are even cheap,” says Jessica Caldwell, Edmunds executive director who analyzes the habits and transactions of car consumers. “Just talking with my team in the genesis of our research, I was like, ‘Can you even buy anything new for $20,000?’”

At the New York show, on the Jacob Javits Center floor, the pickings were sprawled out, slim and largely confined to the subcompact class. The Corolla, Toyota’s entry-level four door, can still be had at that price – as can the rival Honda Civic. A fully loaded Kia Rio rings in at around $20,000; $5,000 more buys a four-wheel drive Subaru Impreza. Throw in the plucky Nissan Versa and the market has essentially belonged to the Asian automakers since the big three scrapped small sedan production three years ago to focus on higher-returning SUVs and trucks.

“And people were only buying those small cars because they offered a ton of rebates and discounts on the hood to make them cheaper than the imports,” says Tom McParland, a veteran car buying consultant. “They were losing money on every unit they sold.”

Overall, the segment of $20,000 or less vehicles has shrunk to 0.3% from 8% five years ago, according to Edmunds. Equally stunning: the market of new vehicles priced under $30,000 has diminished to 17% from 44% over that same span. For the most part, adds Caldwell, people aren’t snatching up these cars for individual use. “It’s fleet buyers and rideshares,” she says. “Individuals aren’t saving their money with the goal of buying one of these either.”

Team Haymaker Take: Picture it — the year is 2030, and four out of every five vehicles on the road are of the “classic” pre-2020-make/model variety, with the other 20% being government-subsidized EVs or ultra-fuel-efficient Vespa scooters outfitted with bulky storage bins and the like. Given time, American transportation will be an amalgamation of Italian roadways and Tesla marketing brochures.

Or the market will sort all this out before that strange outcome can materialize. The global economy is undergoing a reshuffling of sorts, one that will see supply lines, material sourcing, chip manufacturing, and domestic competition congeal, right as vehicle manufacturers/sellers respond to both changing consumer tastes and agenda-driven government stipulations. It does stand to reason that a blend of sustainability emphasis and greater production costs will result in vehicle owners looking to keep vehicles in the family for decades rather than merely a few years. Logically speaking, we might then see a return to the days when parents gifted their teenagers not with new cars (or newly purchased used cars), but with family vehicles nearly as old as the teenagers themselves.

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.