The Lost Decade, The Japanese Experiment Part II

Did we learn anything from the LOST DECADE in Japan?

Does anyone even remember the events that tilted the island nation with a once mighty economy? It is always worthwhile to review historical events. We should always strive to learn, gain knowledge, develop, and get better, but it seems that some of the most painful lessons of the past have been forgotten, erased from our collective memory banks.

Walk with me to 1985, The Plaza Accord. That was one of the most, if not the most, momentous meetings in Foreign Exchange History. France, West Germany, Japan, the United Kingdom, and the United States met and decided to depreciate the US Dollar in relation to the Japanese yen and the German Deutsche Mark by intervening in currency markets. The US dollar depreciated significantly until 1987, when the Louvre Accord was signed.

That event was the catalyst for what ultimately became the Lost Decade(s) for the Japanese economy. The Plaza Accord also fueled a tremendous asset price bubble in Japan. As with every asset bubble it was caused by the excessive loan growth quotas dictated on the Japanese banks by the Bank of Japan. The bank of Japan engaged in a policy called “window guidance.” The result being Japanese banks lending more than anyone else, inflating a monstrous bubble. Cheap credit! Loose credit conditions! Asset price mania! Oh my! Any of that sound familiar?

In a move to attempt to slow down the mania, the Bank of Japan embarked in a tightening policy and raised rates sharply in 1989. Talk about a taper tantrum. What ensued was the largest stock market correction Japan had ever seen. A complete melt-fest.

The equity market crash left Japanese institutions, which were severely overleveraged, full of bad debt. Those firms had to be bailed out by the Bank of Japan. The situation was so dire that what followed was a long period of stagflation. Zombie banks and insurance companies had such atrocious balance sheets, that the capital infusions they received from the government kept postponing the recognition of losses,

making the situation significantly worse. This happened in the late 1980’s, and it continued until the late 1990’s. The Japanese economy was shackled for almost 30 years.

Fast forward to the Great Financial Crisis of 2008-2009. The play book used by Western central banks was eerily similar. Some can argue that the same playbook has been used. To avoid a complete melt down, the FED acted with extraordinary swiftness, bailing out banks and insurance companies in the US. There is no doubt that the remedies were needed. Without central bank intervention the credit crisis would have turned the GFC into a global depression, but the cycle has never been normalized. We have been under emergency funding conditions for over 12 years. Failure was never an option.

Here is a staggering statistic. In 1980 the total level of US corporate bonds outstanding was $ 468 billion, or about 16% equivalence of US GDP. Currently it is $ 10.6 Trillion, or 50% equivalence of GDP. The current pace of the FED’s QE program continues to be torrid, and funding continues to be extraordinarily cheap.

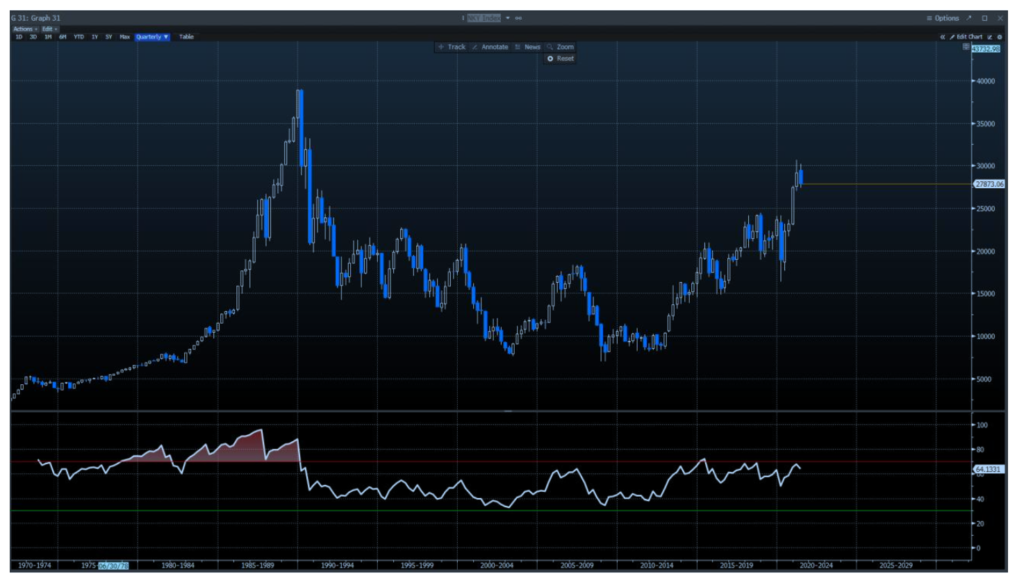

It appears that the lessons learned from the Japanese lost decade have been forgotten. The overlay of the Japanese Stock Market and the SPX for the last 40 years can be summed up with three words, Balance Sheet Recession.

Balance sheet recession is a type of recession that occurs when high levels of private sector debt cause companies to focus on savings by paying down debt rather than spending or investing, causing economic growth to slow, or worse, decline. We’ve reached a point where our system cannot afford rate increases and we face a very uncertain future. At some point the FED will raise rates in an attempt to slow down inflation. My hope is that our fate will not be as grim as that of the Japanese. Hope is not an investing strategy.

Oscar G. Salem

Founder, Managing Partner

BCM Partners, LLC

https://biscuitcapital.com/bcm-partners/