Making Hay Monday – May 6th, 2024

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Charts of the Week

Hartnett, Flow Show

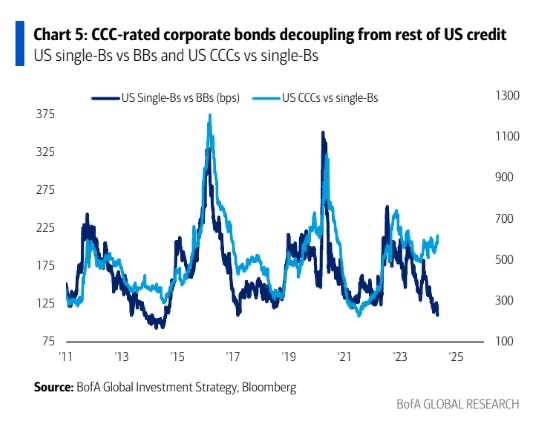

One of the most powerful financial forces is the direction of credit spreads. These represent the difference between the yield level of corporate and Treasury bonds. When they are materially widening, stock and debt markets are typically under pressure. When they are narrowing, markets tend to be buoyant. With corporate bonds there are many different quality tiers, unlike with Treasurys. In the former case, ratings can range from pristine AAA to totally dodge D which might, coincidentally, stand for default. The cut off from investment-grade to high-yield — aka, junk — is at BBB-. However, there is a vast difference between bonds rated BB, which very rarely default, and those rated CCC which have a high propensity to enter bankruptcy. Lately, there has been an intriguing divergence occurring between BBB, B, and CCC-rated bonds. While spreads are very tight (indicating little stress and/or credit concerns) with BBBs vis-à-vis Bs, CCCs spreads have risen close to their post-pandemic highs. This flags potential problems in the junkier realms of corporate credit and a possible contagion up the quality chain. (The chart below is in basis points; 600 is the equivalent of 6%, meaning that a CCC-rated bond yields 6% more than a single B credit and about 9% more than a BBB-rated bond.)

Cembalest

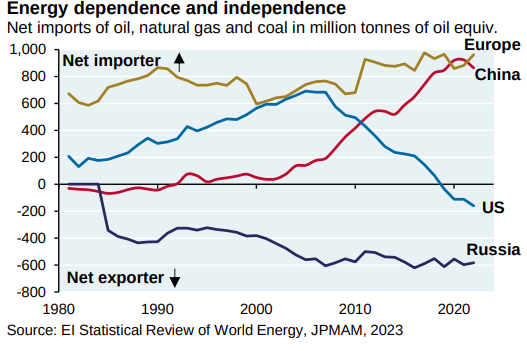

Despite America’s abundant problems and, even, existential threats, arguably the most positive development of the last 20 years has been its shift from one of the world’s largest energy importers to a net exporter. It is sobering to consider what the USA’s trade deficit — currently, almost $800 billion annually — would be had the shale miracle involving domestic oil and gas production not occurred. Arch environmentalists, naturally, consider this to be an anti-miracle. However, most Americans likely have a much more positive view of attaining energy security after so many decades of being beholden to unstable and, often, hostile foreign oil-and-gas producers. By contrast, Europe’s status in this regard has continued to worsen. Thankfully for the Continent, America is now able to deliver large and rapidly increasing quantities of liquefied natural gas (LNG) to its shores.

Evergreen Compatibility Survey

I just look at shale production charts…and think, “This is going to be so bad, and no one outside energy understands it.’” -Matt Miller co-founder of Grey Rock Energy partners, as quoted by Luke Gromen in his May 3rd Forest For The Trees

“Poverty is the worst form of violence.” -Mahatma Gandhi

Champions

Back on December 11th, I highlighted five energy stocks I felt you might want to more closely examine. They were Coterra (CTRA), Atlas Energy Solutions (AESI), APA Corp (APA), Diamond Back Energy (FANG), and one of America’s finest oil-and-gas drilling companies (to be revealed beyond the paywall). Since then, FANG and AESI have been standout performers while Coterra has done decently well. The dog has been APA which is actually down 17%. The soon-to-be-disclosed driller is up about 8%, somewhat trailing the energy sector’s 13% rally from December 11th.

Due to the poor performance by APA, it’s worthy of a revisit soon. However, the focus of today’s Making Hay Monday (MHM) is on the thus far unnamed driller. (A quick comment on APA is that its ultra-depressed trading price leaves it vulnerable to an unwanted takeover offer by a larger competitor.)

For this week’s spotlight company, it has been a nasty decade. Its earnings per share peaked at roughly $6.50 back in 2014. At the bottom of the most recent downcycle — a function of the Covid lockdowns — it lost $2.52/share.

Sales also collapsed by roughly a third and have yet to fully recover. On the positive side, the trend is definitely encouraging. Revenues more than doubled last year versus 2021 and earnings per share hit $4.16. The balance sheet is pristine, in stark contrast to the Down For The Count name to be soon revisited. Net of cash and other working capital, it has essentially no debt.

However, sales growth is forecast to flatten out and Wall Street is projecting profits to ease slightly this year and next. It’s my contention that this outlook might be excessively conservative for reasons to now be cited…

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240507