Making Hay Monday – March 18th, 2024

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Charts of the Week

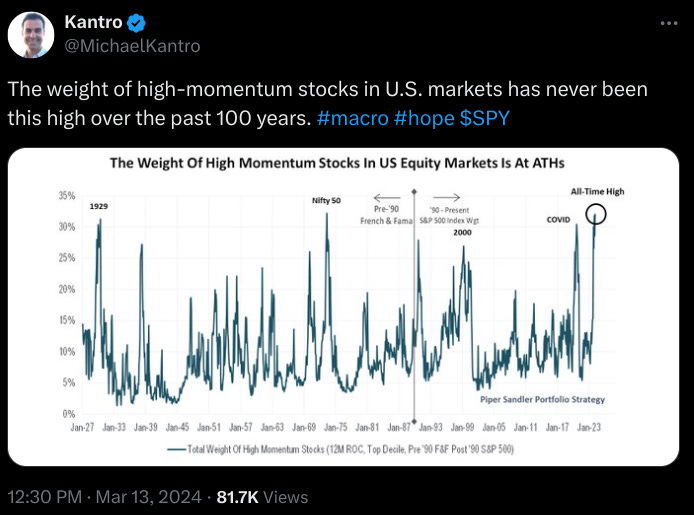

Kantro (Shared by Jesse Felder)

As I’ve previously observed, the amount of financial commentary devoted to the contention that market conditions don’t qualify for the “B” — as in, “Bubble” — word has been voluminous. The usual point made is that valuations aren’t as extreme as they were in early 2000. Related to this view is that stocks like NVIDIA — where the extreme price appreciation has been driven by equally, if not greater, upside earnings increases — wasn’t typically the case 24 years ago. Those arguments are sound, but they ignore the multitude of lesser-quality companies that have been caught up in this latest market moonshot. The above visual on high-momentum stocks being at an all-time high (ATH), as a percentage of the U.S. market, should cause bubble-deniers to reflect on what happened after prior readings around the 30% level.

Image sourced from X, per the above, by Luke Gromen

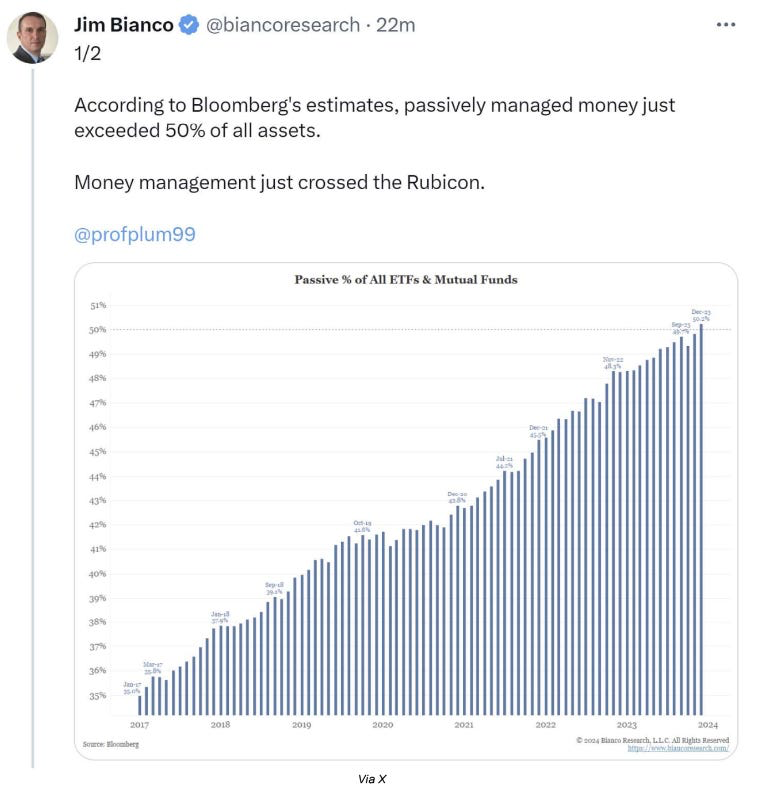

One reason why there is such a long list of nonsensically valued stocks is that so little actual research is performed these days. As the ultra-astute Jim Bianco recently pointed out, “money management just crossed the Rubicon”. (Thanks to Luke Gromen for highlighting Jim’s post on this.) Over 50% of the ETF and mutual fund universe is now passive (i.e., indexed). The late, very great, Jack Bogle, the founder of the first index fund, warned that should this happen the core thesis of passive investing would be called into question. When one considers how much additional capital is managed on a “closet-index” basis, as well as the overwhelming majority of new flows into equity funds that go into passive investing, this phenomenon is even more worrisome. The reality is that thinking investors are currently a highly endangered species in the investment world. Accordingly, it’s likely to be a much more volatile and dangerous environment for investors on this side of the Rubicon.

Evergreen Compatibility Survey

“If investing is entertaining, if you’re having fun, you’re probably not making any money. Good investing is boring.” -George Soros, as relayed in the February 23rd MacroTourist Weekly Round-Up.

My Favorite Style

Champions

What the heck is a style, anyway? When it comes to the stock market, we’ve all repeatedly heard the term “sector”. But styles are a different story; they tend to be rarely discussed, at least by that name. It’s actually odd, because they are much bigger than sectors.

Underlying each style are several sectors, and underneath the S&P there are various styles. You could very loosely say styles are to the S&P 500 as multi-planet solar systems are to a galaxy like the Milky Way. In my analogy, the sectors are the planets and, I guess, running with this a bit more, stocks are the moons that orbit them. However, instead of a few hundred billion stars making up each galaxy, the S&P is composed of nine basic styles. Those are: Large-Cap, Large-Cap Value, Large-Cap Growth, as well as three of the same for Mid-Cap and for Small-Cap. Three times three is, last time I checked, nine.

When it comes to the dollars involved, the Large-Cap S&P styles can put stars to shame with, in some cases, trillions invested in them. These days, the market value heavyweight is, of course, Large-Cap Growth, where the Magnificent Seven are mostly domiciled.

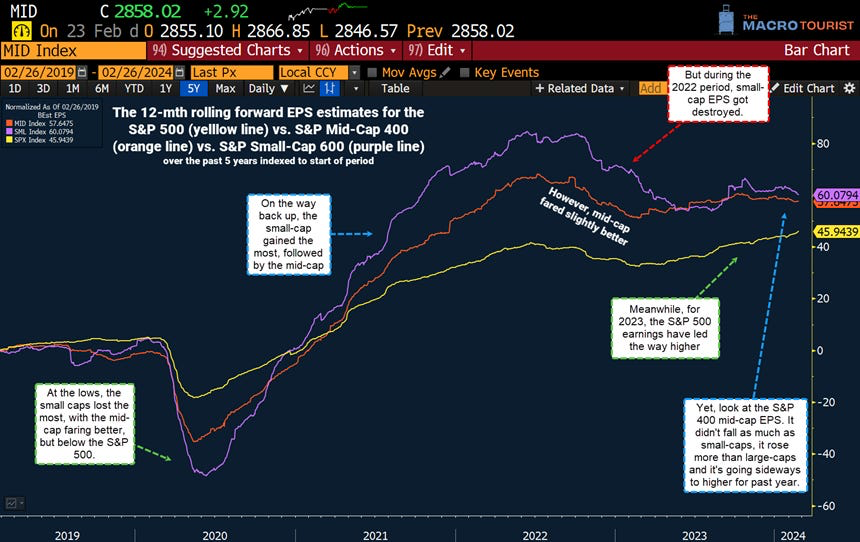

Despite all the attention focused on the Large-Cap style currently, particularly growth, I have long preferred the Mid-Cap cohort. This is because companies that make it to this status are large enough to be resilient, with generally stronger balance sheets and superior business models (i.e. competitive moats) vs Small-Caps. You can see that in the chart below from Kevin Muir, author of, in my view, one of the finest financial publications, The MacroTourist.

Purple Line: Small-Cap Earnings Per Share (EPS); Red Line: Mid-Cap EPS; Gold Line: S&P 500 EPS

Muir

You’ll notice that Small-Cap earnings plunged during Covid, came roaring back after that, then took it on the chin again during the 2022/2023 earnings recession. (A side note: as many Haymaker readers can attest, I did often opine I thought a profits recession back then was more likely than an actual economy-wide downturn.) With Mid-Caps it was a much smoother ride, as you can also discern. Frankly, what surprised me is that both have meaningfully exceeded the earnings rise by the S&P 500. The latter, of course, has greatly benefited from the profits eruption by the Magnificent Seven. …

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240318