Making Hay Monday – August 7th, 2023

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Quick Note

We realize that Haymaker going paid has been traumatic for some. Like I’ve often said in my podcast appearances, free is everyone’s favorite price. But it’s also not a sustainable one.

However, as you know, we will continue to provide a fair amount of content free of charge. But that should really only be for the market tourists among you. For serious investors, receiving our guidance-rich Friday Haymaker editions should, at the cost of about seven lattes a month, be a no-brainer. In this week’s issue, I am going to make a passionate case for an area where almost everyone either has zero exposure or is only lightly invested. In my view, it is one of the best risk/reward situations I’ve come across in my 44-year career.

Even more attractive on a bang-for-the-buck basis, in my admittedly biased opinion, is our Founding Member level. Another admission is that this tier is meant for those who are managing their own portfolios or are doing so for others. One of the services I’ll provide for these subscribers is access to the content I come across in my exhaustive readings that I feel is particularly noteworthy. We’ll also relay a daily note from our partner firm, Gavekal Research. Periodically, I’ll switch those out when I feel they are of marginal interest and substitute in a compelling piece from another source.

The monthly Zoom meetings we’ll be hosting (to include a substantial Q&A section) will allow me more latitude to get into investment specifics — though with copious disclaimers. Because this forum is meant for sophisticated investors, you should be able to do further research on any ideas discussed.

To all those opting for the free version of Making Hay Monday, we welcome you along for the ride. It’s likely to be a thrilling one… even if there are times when you are hanging on for dear life. One of the greatest services I believe we can offer is to keep you from overreacting during good times, like now, and, especially, when fear takes control of the markets. As the author of Dune, Frank Herbert, long ago wrote in that very book: “Fear is the mind-killer.” Nowhere are those words more applicable than they are in financial markets, where it has been repeatedly shown that fear is even more powerful than greed. Please allow Haymaker to help you keep both of those toxic emotions in check.

-David “The Haymaker” Hay

To learn more about Evergreen Gavekal, where the Haymaker himself serves as Co-CIO, click below.

Charts of the Week

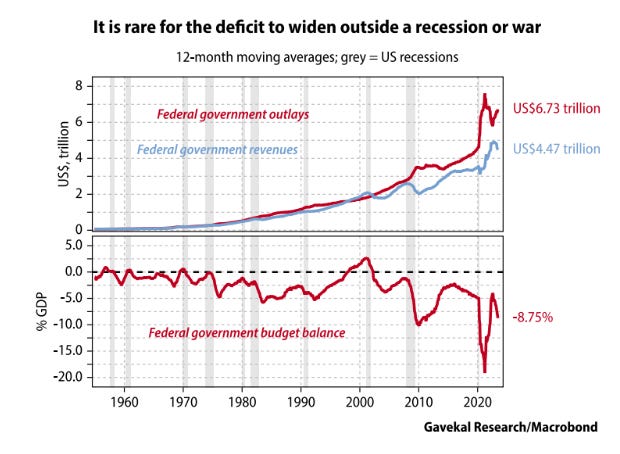

While Fitch’s downgrade of the USA’s credit rating received the most press, the real jaw-dropper was the Treasury’s announcement that it plans to sell $1.85 trillion of new debt in the second half of the year. Even prior to this shocker, the Federal government’s hemorrhaging of red ink was appalling. This elevates the odds that one of my two biggest fears for 2023 — a Treasury market convulsion due to a deluge of new supply — might be unfolding. The fact that Fitch still has a AA+ rating on America’s sovereign debt strikes me as more than a little charitable.

Perhaps the rating agencies need to adopt a two-tier structure: one rating based on holders being repaid in depreciating dollars and the other discounting inflation. There is no question the U.S. can fund its debts via the Fed’s Magical Money Machine (once it is restarted, as I think is inevitable). Thus, in that regard it deserves to be rated AAA. However, adjusting for currency debasement I would argue it should be assigned a junk bond rating… and not a very high one at that.

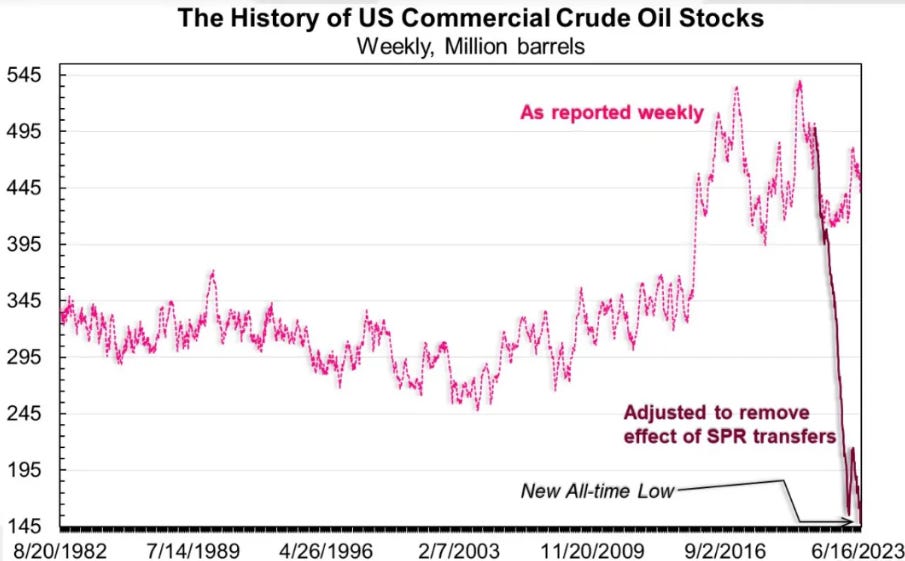

Just six weeks ago, bearish sentiment dominated the crude market, with pundits such as Jim Cramer asking why investors would want to invest in a commodity that was falling in price. From the mid-60s trough in June, crude is now trading over $80/barrel, roughly a 25% surge. The above chart, showing oil inventories adjusted for the SPR releases, is a powerful visual regarding what a dangerous game the administration is currently playing. Bloomberg reported on July 26th that gasoline prices are ripping all over the world.

Also at the end of July, it was reported that U.S. commercial crude stocks plummeted by 17 million barrels, the greatest weekly drop since the early 1980s. Accordingly, a powerful short squeeze of both the hedge fund community (which had significant bearish bets on oil) and Team Biden appears to be underway. The Saudis and the Russians are likely to increase the pain for the shorts in the weeks and months ahead. (By the way, Mike Rothman, creator of the above chart and my favorite oil market expert, nailed it once again back in June when he was strongly urging his readers to go long oil and energy stocks.)

“US real retail sales are falling 1.6% YOY…this indicator has faithfully coincided with US recession since 1967.” -BofA Investment Strategist, Michael Hartnett

“Interest rates rise and fall but the gargantuan amount of debt created over the last 20 years is forever until destroyed by inflation, currency debauchment or default. It can never be repaid in constant dollars because the global economy lacks the productive capacity to generate sufficient earnings to do so.” -Michael Lewitt, author of The Credit Strategist, a constant source of outside-the-box common sense.

Point of No (Real) Return?

The question of whether this is time to go long on long-term Treasury bonds is one of the most important decisions investors face, at least those desiring to lock in today’s high or, at least, higher yields. Given the current set-up, which I’ll delve into shortly, I would normally answer in the emphatic affirmative. However, because the objective with any investment should be to earn a positive return, net of inflation, my typical late-in-an-economic-expansion enthusiasm is significantly curbed. Going one step further, the prospective gain should also be above zero when taking taxes into account.

For example, with a 10-year T-note now yielding a bit over 4%, to someone in the 30% tax bracket, the after-tax return is 2.8%. (Obviously, this doesn’t immediately apply to securities held in IRA-type accounts though, ultimately, tax does need to be paid.) With inflation in the 4% range presently, the net-net return is negative. If you assume inflation gets back down to the Fed’s 2% target, and stays there, then a small return after both inflation and taxes would result. To my way of thinking, the “and stays there” part is the most dubious.

As anyone who watches CNBC or reads the financial press is aware, the investment community at large is convinced of two things: a recession will be avoided and inflation will continue to fall. While I am a confessed contrarian, that’s not the reason I take issue with both views. Rather it is the weight of economic data that is driving my parting of the ways with the cheery consensus.

Let’s start with inflation. Longer term readers are aware that I felt that inflation was poised to surge in late 2020. As the calendar flipped into 2021, I became increasingly convinced that was the case. (In May of 2021, I even had a spirited debate with the legendary Ed Yardeni on this topic at that year’s Mauldin Strategic Investment Conference). Once 2022 rolled around, I was of the opinion that an inflationary boom (i.e., strong growth with persistent inflation) was probable.

For the first half of 2022, we got the inflation but without the boom. In fact, GDP was actually negative in quarters one and two of last year. (Very few seem to recall that these days, when GDP is back to running in the black.) The war in Ukraine spiked commodity prices, exacerbating what was already the worst inflation in decades. But then a funny thing happened: those same commodities began to plunge in price.

*On the recession debate, over the weekend I listened to a data-dense podcast by my friend Adam Taggart and economic analyst extraordinaire Eric Basmajian. If you are in the soft-landing camp, I’d strongly suggest you check this out. Getting the recession call right is critical to your portfolio’s performance over the next year. We’ll be including a link to that at the end of this Making Hay Monday for paid subscribers.

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20230808