Making Hay Monday – April 8th, 2024

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Charts of the Week

Rosenberg, BWD

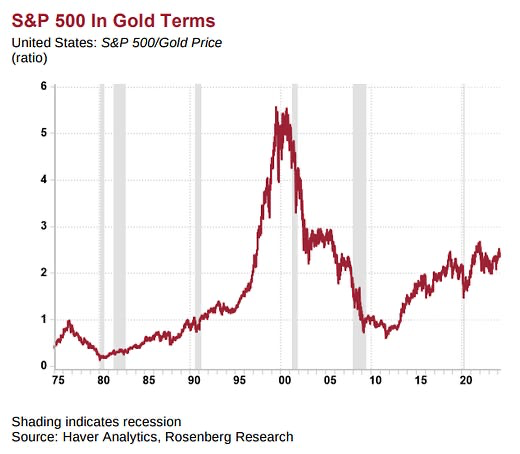

There are likely very few investors who are aware that the S&P 500 remains far below its 2000 peak when measured in terms of a store of value that can’t be debased. That would, of course, be the “barbarous relic” known as gold. Accordingly, it’s reasonable to consider how much of the S&P’s returns this century have been a function of a “money illusion”. This is essentially the superficial return created by inflation and a chronically weakening dollar.

Minack, Downunder Daily

On the topic of real, or after-inflation, market returns, Chinese stocks have been duds going back all the way to the early 1990s. This is despite that China has enjoyed one of the greatest economic booms in world history. On the positive side, Chinese stocks are now at rock-bottom valuations. However, geopolitical risks are immense and, for now, communism is ascendant in the Middle Kingdom, while capitalism is in an eclipse.

Evergreen Compatibility Survey

“What generates the evils is the (monetary) expansionist policy. Its termination only makes the evil visible. The termination must at any rate come sooner or later, and the later it comes, the more severe are the damages which the actual boom has caused.” -Ludwig von Mises, ‘The Causes of the Economic Crisis’

“I cannot teach anybody anything. I can only make them think.” -Socrates

Royalty on the Cheap

Shutterstock

Champions

It is pretty much accepted wisdom that it is impossible to beat the S&P 500 on a long-term basis. As many Haymaker readers are aware, there’s nothing I like better than to challenge the accepted wisdom… if I have strong data to back up my views. That’s exactly what I intend to provide you with in this edition of Making Hay Monday.

First, since we are talking about long-term results, let’s consider the total return generated by another well-known index. Admittedly, it has fallen into disfavor over the past decade and particularly since the end of 2015. Here’s a chart of how it has done versus the S&P over that timeframe. (The red line is the S&P 500; the white line is our, for now, mystery index):

Bloomberg

A 46% price lag, 146% vs 192%, is certainly significant. In fact, it’s large enough, and long enough, to cause many investors to abandon the index represented by the white line. (As usual, that will be revealed only to paying subscribers.)

However, zooming out to the start of what would turn out to be the Roaring ‘90s, for both stocks and the U.S. economy (now, that was a real boom!), tells a radically different story. As you can see, that white line has absolutely trounced the S&P 500.

Bloomberg

Clearly, there is something powerful at work here that, for some reason, hasn’t been exerting itself, or has been overwhelmed by other factors, for nearly a decade. Without giving too much away at this point, my contention is that “something” is called dividends…

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240409