It’s a He Says, She Says Week

It’s a He Says, She Says Week

The week looks to start quietly despite S&Ps diffusion indexes, published worldwide today, which will show signs of a slowdown in economic activity. Unless there is an almighty shock equal to getting a full day’s play at Old Trafford, it’s unlikely that they will move the currency markets ahead of Wednesday and Thursday’s Central Bank meetings. Interestingly for the markets but annoyingly for the Fed and the ECB, the days after their announcements will see instant judgment on their actions. In the U.S., the Fed’s favoured measure of inflation is published on Friday, whilst France and Germany report their respective inflation readings.

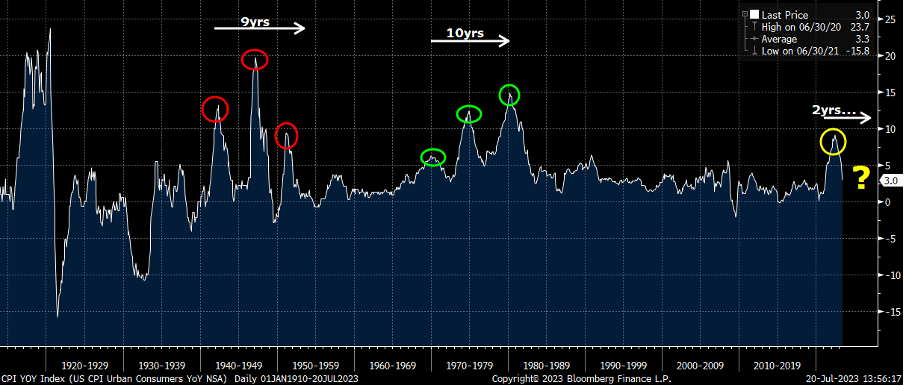

Washington, D.C., will become the financial world’s centre of attention at 7.00 on Wednesday night when Chair Powell will announce the Fed’s interest rate decision and give the markets some hints and guidance to their future policy. Let’s get the easy bit done first and say, without a doubt, they will raise rates by another 25bp. The question is, what signals will they give as to future policy? With the Labour market still looking pretty robust, despite some economic clouds appearing, it is exceedingly unlikely that they will signal any softening of policy and will leave the door ajar for further tightening. Inflation is, without doubt, heading in the right direction, but the Fed, as are all central banks, are cognisant that their record on inflation forecasting is, to say the least, flaky. Us somewhat more senior members of the financial community remember the bounces that inflation had in the 1970s (but not the 1940s!), as the accompanying chart prepared by my friend and top analyst Michael Brown illustrates.

As they say, past performance is no guarantee of future replication, but we, and the central banks, should be wary of a so-called “trampoline landing “.

Underlying these fears are the adverse effects of extreme weather and the war in Ukraine on crop prices. With Wheat futures, on the CBOT in Chicago, going limit up twice last week and India doing what West Ham wished they had done, banning Rice exports, it is perhaps time to start watching for signs of food inflation reappearing. With this in mind, a weakening dollar also potentially feeding inflation and stock markets still bubbling, it’s hard to see Jay Powell being anything other than hawkish at his Press conference. Having seen the dollar put on its largest weekly rise for five months last week, will he be hawkish enough to encourage further gains? I’m not so sure, especially if Friday’s inflation shows additional signs of disinflation.

Closer to home, the ECB meets on Thursday, the day after the Fed’s announcement. In reality, the ECB is very much the supporting act, but again, a 25bp hike is expected. With the ECB matching the Fed’s move, no significant volatility is expected in the USDEUR market; indeed, the options market isn’t looking for any action larger than 60 pips. With such a well-telegraphed move, again, what is said after will be of as much interest as the actual move itself, and the market will be looking for a steer on the timing of the next 25bp. With uncertainty over the economy, the most likely outcome of the press conference will be that Christine Lagarde deliberately says a lot about nothing, and we end up none the wiser. If I had to have a bet, I would favour September for another 25bp hike, but whether that comes to pass remains unsure.

Sterling will be out of the limelight this week as attention focuses elsewhere, which will probably be a relief for the Bank of England and Rishi Sunak’s under-fire government. Slightly worrying for the authorities, the pound came under some quite intense selling pressure towards the end of last week as the softer-than-expected CPI figure cast doubt over the resolve of the Bank of England to raise rates much further. Finally, to complete the week, the Bank of Japan meets on Friday with some traders expecting tweaks to its Yield Curve Control. We may, at last, get some excitement from a BoJ meeting, although it’s far from certain!

Button up; it’s going to be a lively week!

20230724