Haymaker Friday Edition with Kevin Muir, The MacroTourist!

Haymaker Friday Edition with Kevin Muir, The MacroTourist!

Charts of the Week

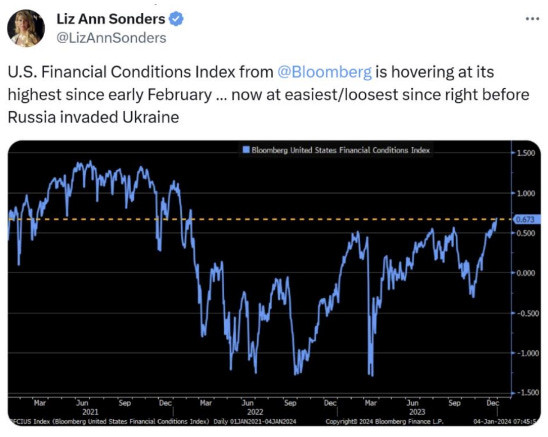

If you are wondering why the stock market keeps going up — at least, the former Magnificent Seven which is now down to five, with Apple struggling and Tesla swooning — this image from Charles Schwab’s Liz Ann Sonders is explanatory. As you can see, financial conditions are now the easiest in almost two years. This was prior to the worst of 2022’s brutal bear market in both stocks and bonds. Considering how much tightening the Fed has done since then, this is a remarkable development. It speaks to how much financial markets have eased by reducing interest rates and narrowing credit spreads. (The latter involve the yield gap between government and corporate debt; when that narrows, as it has dramatically since the summer of 2022, stocks and bonds typically rally hard which has indeed occurred.)

Shared via Gromen/FFTT

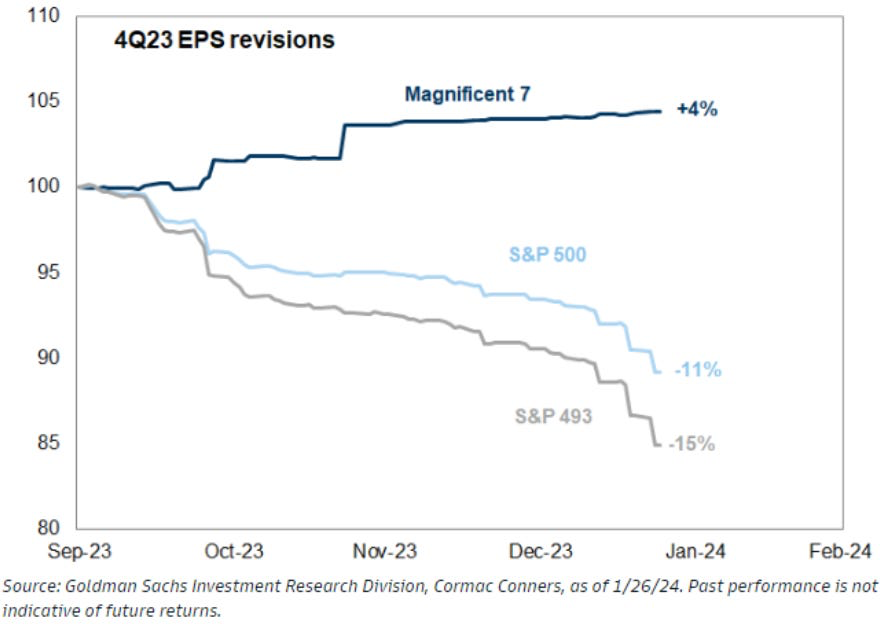

Related to the continuing outperformance of the Magnificent Seven (Five?) is the far better earnings performance they have been delivering and/or are expected to deliver. The fact that fourth quarter profits estimates have been slashed as much as they have for the S&P 493 is surprising. This is because an earnings recession already played out last year, though a mild one. But even more perplexing is that the federal government deficit doubled in fiscal year 2023 (ended September 30th ). Moreover, federal red ink is hemorrhaging even more profusely in the first quarter of fiscal 2024. High levels of deficit spending nearly always correspond with soaring corporate profits. This is a reality stock market bulls are currently overlooking.

Goldman Sachs

“Demand for raw materials is at record levels, inventories are low, and spare production capacity is largely exhausted. This is just classic ‘own commodities.’” -Jeff Curie, former head of commodities research at Goldman Sachs.

Muirly a Coincidence…

Shutterstock

If adversity makes you stronger, assuming it doesn’t kill you, it’s reasonable to conclude that it was a positive and resilience-building experience. That sounds so comforting. However, as someone who is one of the few oil-and-gas bulls left on the planet, I will admit that rigor mortis may set in for me at any moment.

The one thing staving off the grim reaper might be my willingness to take advantage of “dead-cat bounces”. Those are the feeble rallies that typically accompany asset classes that have been on the receiving end of a constant flagellation that could make the Marquis de Sade wince. For almost two years now, the rebound off of terra firma by feline cadavers has been pretty much as good as it gets in the desolate world of energy investing. (Fossil-fuel investors, take heart — it could have been worse; you could have been holding that ripping bag known as alternative energy securities, which have been anything but secure.)

The most recent case in point was the sneaky rally that oil performed since early December. Last week, that amounted to a 12% pop from trough to peak — not bad for less than a month. This was enough of a reversal to cause me to downgrade crude to a hold a week ago. Said rating reduction was despite an untimely 2% swoon on the same day that Making Hay Monday (MHM) went out the digital door. In that edition of MHM, I stated my intent to run in today’s Haymaker one of the rarest of all research notes: an actual bullish piece on oil. Further, I explained it was from Kevin Muir who has given me permission to rebroadcast his first-rate work whenever I am so inclined. Today, with oil getting slammed for the third day in a row, I am very much inclined to showcase any credible analysis that offers hope to the shrinking herd of wounded energy bulls.

Before getting to Kevin’s latest persuasive musings, I will elucidate that, as most Haymaker readers are aware (I hope), I have used the occasional fleeting rallies oil has seen since the hockey-stick move caused by the war in Ukraine to cash in some gains. This was, of course, after buying into at least two of the plunges seen since then. (The rebound coming out of last June was particularly rewarding.)

One of the techniques I’ve used to get a sense of when the worst of oil’s bungee jumps might have been over is when sentiment has become exceedingly bearish. This can be measured in several ways, as Kevin describes near the end of this note. As my team and I at Evergreen also do, he uses positioning in the futures market as a critical input. Per numerous previous comments I’ve made on the participants behind these readings, their hyperactive nature makes them excellent contrary indicators. In other words, when they are all-in with bearish bets you usually want to be adding exposure and vice versa. (It’s been a lot more versa than vice since the spring of 2022.)

As you will read, Kevin has also been waiting for a sign that the most recent downtrend, which started in late September, has been broken. The aforementioned rally gave him just such a signal. Alas, as has been the pattern for these last nearly two years, its life cycle was about as long as a tsetse fly. After the drubbing since Tuesday, oil is now down 8% from last Friday’s close — i.e., really bad in just a week. To put this in perspective, that would be like the Dow shedding 3000 points. A stock market decline of that magnitude would, of course, be front-page news. For the oil market, it’s simply another week at the office. Yet, despite this latest setback, I think Kevin’s reasoning is sound and his timing is, as our title indicates, unusually coincidental. His point about the exceptionally low levels of oil inventories is spot-on, in my view. In fact, I think it’s utterly brilliant since it’s one I’ve made repeatedly over the last year or so. As you will see, his last visual in that regard would seem to be consistent with oil prices and sentiment at lofty levels instead of in the dumpster, as they are presently.

He’s also right that the futures market is currently in backwardation (spot prices higher than future prices as opposed to the far more normal opposite condition). This is another indication of an undersupplied condition. Why the sellers come out of the woodwork at the slightest whiff of bad news given this backdrop is a mystery. However, it’s merely stating the obvious that many in positions of power prefer to see prices depressed. Of course, consumers do, too.

The problem is, as the old saying goes, the cure for low prices, is low prices. If they are being artificially driven down, this may ultimately lead to serious shortages and a future cost of crude well into triple-digits. The fact that the drilling rig count is down sharply and is continuing to fall is one example of the law of unintended consequences.

Evergreen Compatibility Survey

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240203