Haymaker Friday Edition

Haymaker Friday Edition

In The Ring – December 8th, 2023

Making Gains Out Of (Tax) Losses

Shutterstock

“… (when) futures prices go down so fast, physical buyers wait to try to get a better price, weakening further the crude physical differentials*, and increasing the weakness sentiment, driving more selling of futures. So it is a snowball effect until everybody is short, and then…” -Pierre Andurand, one of the world’s most successful oil traders (the Haymaker is very much looking forward to the “and then…” part)

*The spread between the futures market and the real market for oil.

Evergreen Compatibility Survey

Back in late October, I wrote that up until then there hadn’t been the usual rally this month so often bestows upon investors. At the time, I noted that this was likely due to a combination of a string of weak earnings reports and the “gravitational pull from dramatically higher long-term Treasury yields”. Additionally, I wrote that because stocks and bonds were seriously oversold, a rally might be in the offing.

As usual, it was stronger than I expected. A driving force behind that has been an extraordinary price recovery by U.S. Treasurys (USTs). Again, I thought they were poised to bounce but not like a bungee jumper after the cord recoils. Despite this muscular rebound, you can see that prior key support levels have not been reclaimed.

Price of the 10-year Treasury Note Since 2010

(Lines indicate long-term support levels; these were both taken out during the bond bear market starting in late 2020, providing a timely warning of the carnage to follow – Click chart to expand)

Bloomberg

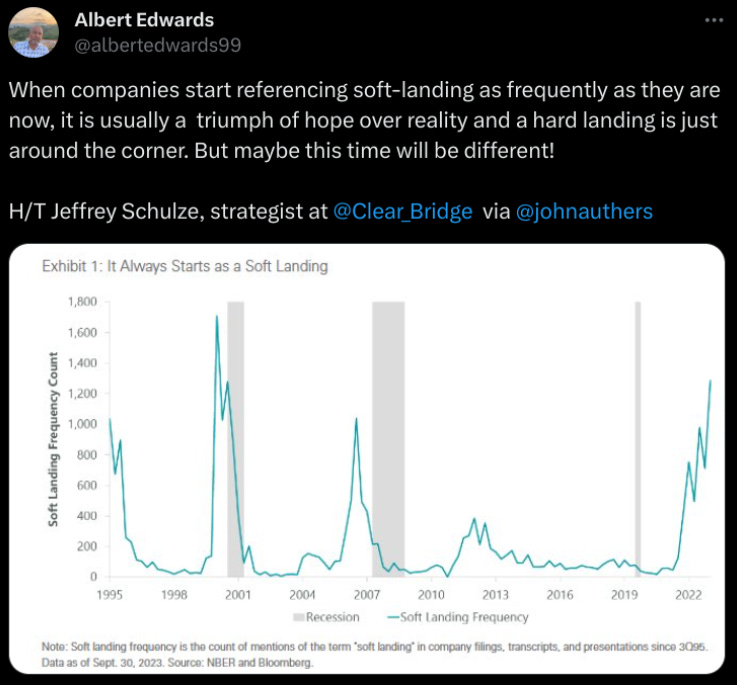

The catalyst for this resounding bond rally has been a series of weaker economic data. That includes Tuesday’s startling plunge in job openings. (Today’s employment release went the other way but due to the fact that every month’s jobs numbers this year has been revised downward, don’t place too much emphasis on it.) In other words, the hard landing I’ve been warning about (for a long time!) is beginning to worry the consensus conviction in a gentle economic touch-down. As you can see below, courtesy of Albert Edwards, the faith in the soft-landing narrative has been almost universal.

Edwards

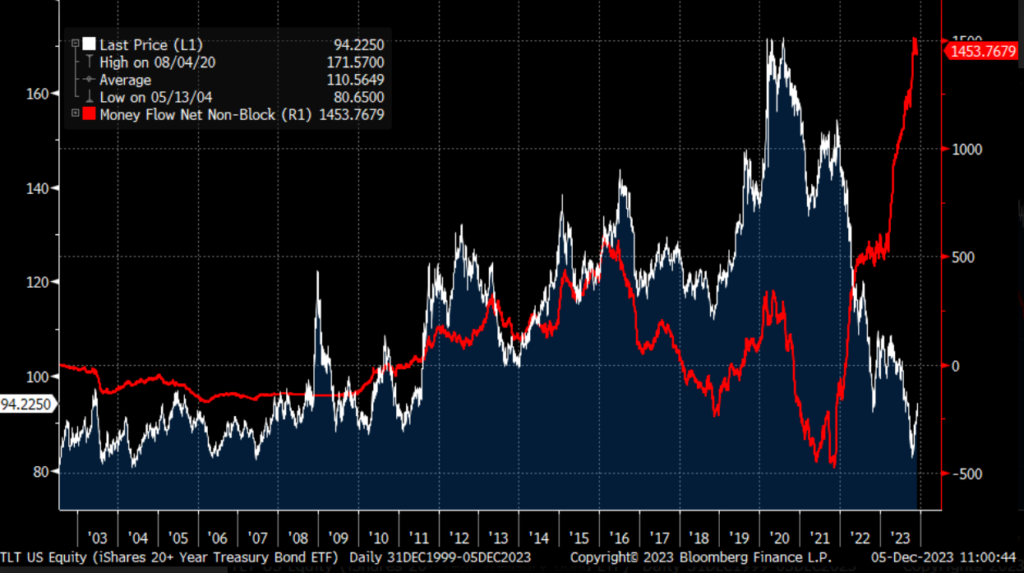

Even prior to the rally, investors were foaming at the mouth to buy into the bond sell-off. In recent months, the inflows into the long Treasury bond ETF, TLT, have truly gone postal, as you can see below.

(White line: price of the ETF | Red line: the flows into it)

Bloomberg

What they are ignoring is one of my most fervently held beliefs: namely, that the U.S. Treasury (UST) market is very likely to be overwhelmed by an explosion in the federal deficit once the next recession hits. My totally inexact guesstimate is that it might double from the current inexcusable $2 trillion level to around $4 trillion.

However, earlier this week I listened to a podcast hosted by my pal Adam Taggart. (You can find him on Substack under Thoughtful Money; in my view, he’s one of the best in the business and can even make yours truly sound lucid.) His recent guest was Michael Pento, who forcefully warned about the dangers to the long Treasury market from what he thinks could be an annual deficit of $6 trillion, should this be more of an economic crash landing — $4 trillion is scary enough; $6 trillion is almost inconceivable.

This prospect is far off the radar of the hordes of raging bond bulls, much like a hard landing was considered a remote possibility until very recently. Consequently, it has the potential to be extremely destabilizing should they begin to connect the dots that a recession is highly probable to be very long-bond unfriendly. That’s not likely to happen anytime soon and further deterioration in the economic data might easily extend this rally for a time. Regardless, it looks way overdone to me.

Fortunately, for those who have been dollar-cost-averaging into emerging market debt funds, they have exceeded the 10-year T-notes price increase, and nearly matched the moonshot by TLT, since the late October lows. It continues to be my expectation that on a multi-year basis these will leave long-maturity USTs in the dust. (Before year-end, I hope to highlight a Brazilian bond denominated in dollars that might interest Haymaker readers, at least those of the paying variety.)

For now, though, in case you think the stock market has moved too far, too fast — a thoroughly reasonable conclusion — there is a seasonal opportunity I’d like to point out to our beloved paying subscribers. …

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20231209