Transports, Small-Caps Weakening, while Treasury Rally Looks Nearly Complete

| SPY- SPDR S&P 500 ETF Trust Support: 430, 425, 420 Resistance: 437, 438-438.50, 440 |

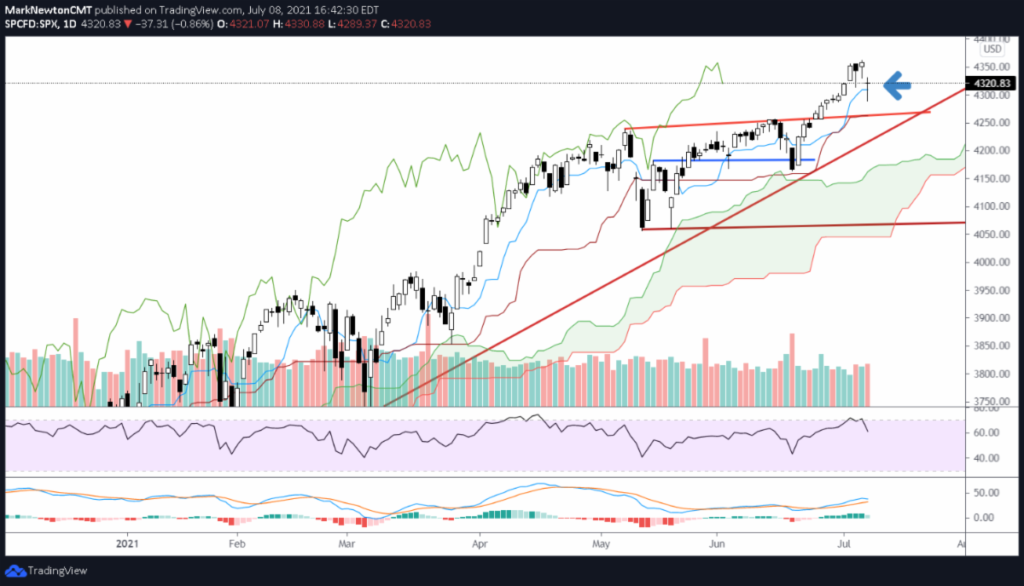

Replay Link- Technical Analysis Video Webinar- 7/8 https://youtu.be/lDuUAoo1Tmc Replay- 7/1 Technical Webinar- What does Growth say about 2H 2021? https://youtu.be/m16YIBQglso MY CNBC interview 6/16 on choosing AMZN vs GOOGL https://www.cnbc.com/video/2021/06/16/amazon-vs-alphabet-traders-take-sides-after-bold-analyst-call.htm SPY – (3-5 Days)- Bullish- As much as the deterioration in Transports, Small-caps, EM, Financials is of concern, SPY barely made new multi-day lows & still in good technical shape. Under 427 is needed to change near-term to bearish, as this could lead to 415-420. For now, its thought that move back over 432 should happen, causing a bounce into next week. FEZ (3-5 Days)- Bullish – Pullback has now reached important support near 46 that likely holds, and along with SPY, both can trend higher over the next week. FEZ has been far weaker than SPY, so expecting resistance near 48.31 on rallies. Technical Long/Short Focus list 7/09/21 |

| Top Technical Developments 1) SPY, NDX finally experienced a rare “down day”, though rallied back resiliently to fail to do much damage. It’s thought that Technology’s influence continues to help these indices hold up better than the broader market. 2) Technology is nearing overbought levels, while Financials, Transports have broken down, yet look close to support. It’s not unrealistic to expect yet another rotation from Growth back to Value into late July, where Tech falters while Value snaps back. 3) US Dollar broke out to new intra-day and closing highs for the month of July. This should pressure Commodities and Emerging markets a bit longer, but should create buying opportunities into mid-July. 4) Over half SPX SPDR ETFs have been lower over the rolling 1 month period, losing between 2-7%: Industrials, Materials, Energy, Financials, Utilities, Staples. Meanwhile, Cons Discretionary and Tech are up 6-7%. 5) TLT near resistance/ Treasury yields look to be near support after the big flush in recent days. Counter-trend exhaustion signals look to create selling opportunities for Treasuries Thursday-Friday and it’s right to exit TLT, TMF in the short run into end of week and consider shorting Treasuries for a bounce in yields. 6) Energy along with Small-caps are two areas to focus on after recent weakness. The divergence in Energy as a sector with greater than 6% losses in the last month, despite WTI Crude just having hit new highs for 2021 is interesting but ultimately should lead Energy to bounce and WTI back to 80. 7) Emerging markets have broken down, per EEM’s triangle violation with Dollar strength. This looks to continue into mid-to-late July but should ultimately create attractive buying opportunities for the metals. 8) Next major cycle hits between July 14-22. Back in June, my cycle projection caused peaks in NY Composite and Value Line, and many sectors peaked, yet, SPX and QQQ did not. I feel mid-July is the possible tipping point for Technology and a rotation back to Value might occur. 9) Transportation has broken the entire trend going back since last March lows. This will need to be repaired to have faith in Transports outperforming, and for now, this sector is a laggard. 10) Sentiment has come in (understandably) more subdued this past week, with AAII bulls being reduced to 40 from 48 and the Bulls bears spread is back under 20. Concerns on the growth outlook with yields plummeting, and/or FOMC’s “Beginning of the Endgame” for Tapering look to be concerns, along with Tax reform at this weekend’s G-20. |

Still very difficult to fight the uptrend, as SPX (SPY), NDX have shown little to no weakness but divergences and breadth/momentum problems remain. Even Thursday’s initial -1.5% decline failed to hold as prices ground back to show just -0.8% losses. While the violent sector rotation has been important, and a technical negative to see Equal-weighted Indices fail to push back to new highs (as the last meaningful time this happened was last February right into 2020’s meaningful peak), there simply has been very little evidence of weakness in SPX, nor NDX. Given Technology’s dominance in SPX, and NASDAQ, these have held up in much more robust fashion of late and haven’t shown the same degree of weakness as NY Composite, or Value Line Geometric, which are thought to be purer forms of “the market”. The key message here is that Technology’s influence continues to be the important anchor for this market, and until we see meaningful evidence of Tech rolling over, ALONG with the inability of Financials, Materials, Industrials, Discretionary, Energy, Healthcare to rally to pick up the slack, then this is simply a larger game of Musical Chairs. Breaks of June lows remains the first real worry for SPX, and breaks of May indicate this market rally is vulnerable to acceleration lower into the Fall.

Transports have to be watched carefully, as DJ Transportation Avg has just broken the entire uptrend from last March 2020 lows. This “leading” index is now down nearly 10% in less than two months, and always important to watch when Transports are not confirming SPX, or DJIA’s push back to new all-time highs. Nearterm, i do feel TRAN is nearing initial support of this first move down, but has to be given extra attention here and not overweighted in any big manner until this can stabilize and regain 15075. This closed back down on its lows Thursday after having violated the last few weeks of lows, which is a short-term negative.

Treasury Risk/reward poor after this sharp rally and rates look close to reversing course in the short run. TLT gave early warning about yields imploding after prices broke out of this lengthy downtrend from last Fall. TLT has now eclipsed the 38.2% Fibonacci retracement and just below both 50% levels as well as former June spike lows, which now should be strong resistance) Additionally, evidence of DeMark based exhaustion is now present and means that further pullback to 1% in US 10-year rates is unlikely for now. Overall, i like selling TLT, TMF here and going short Treasuries, buying TBT, TMV for a push back higher in yields into end of month.

Mark Newton

Managing Member/Founder

ML Newton Advisors LLC

You can reach me at: https://newtonadvisor.com/

Or email me at info@newtonadvisor.com for copies of recent notes, or to inquire about how my work might fit to one’s investment process.