Making Hay Monday – October 2nd, 2023

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Charts of the Week

One of the most shocking developments of this year has been the extreme weakness in the normally low-volatility utility sector. Including another 5% hit today, utilities are now down almost 27% on a price basis versus their peak last fall. Obviously, surging long-term Treasury rates have been a big factor in this shellacking. Unfortunately, I’m old enough to vividly remember 1987 when a similar bloodbath happened. Back then, the primary utility index (the Dow Jones Utility index) plunged 29% from peak to trough. In my view, the most recent utility sector rout is an ominous sign for the overall stock market, including the Magnificent Seven.

Utility stock index performance over the last two years

Utility stock index performance from the first quarter of 1986 to October of 1987

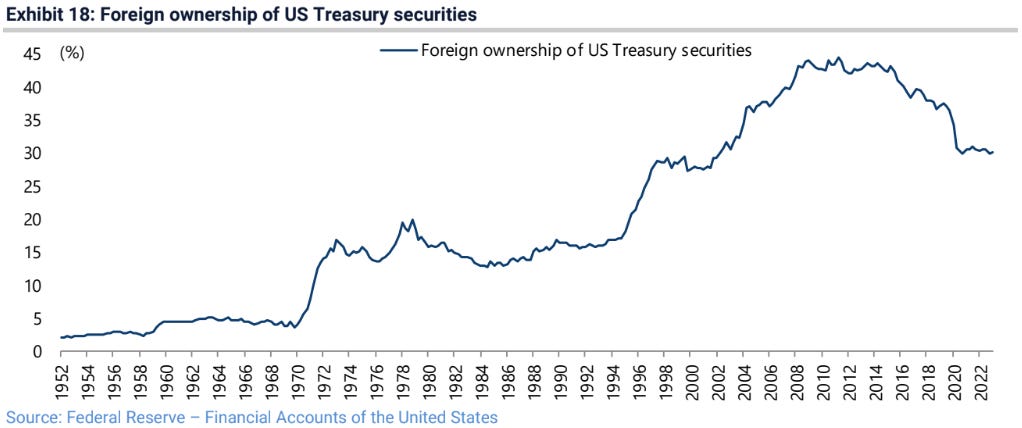

With the federal government needing to raise in the vicinity of $3 trillion in fresh financing between now and the end of next year, along with rolling over $10 trillion of maturing debt, the fact that overseas investors are, in aggregate, selling U.S. Treasurys, is problematic. Greatly adding to this challenge, both the Fed and U.S. banks are also sellers.

Have the bank runs run their course?

“When you have a bond market and a mortgage market that’s concentrated as much as it is today because of quantitative easing, you can’t raise rates that much or you make everybody insolvent. This is kind of basic Bond Market 101, but apparently the board in Washington did not see this, so now they do.” -Chris Whalen

“Strange how paranoia can link up with reality now and then.” -Philip K. Dick, A Scanner Darkly

The man who stood out for his early and prescient warnings about the threats to the banking system has gone silent. Chris Whalen was among the precious few banking experts who cautioned, as far back as last year, that surging interest rates would soon pose a big problem for the industry he so closely follows. When SVB (Silicon Valley Bank), First Republic, and Signature Bank failed in quick succession last spring — three of the largest bank failures in U.S. history — his views were resoundingly vindicated.

He opined at the time that there were many more yet to come. Along similar lines, The Wall Street Journal reported that, quoting Stanford University finance professor Amit Seru, there were 500 more institutions, about 11% of America’s total number of banks, in worse condition than SVB. Yet, over the last six months, it’s been all quiet on the banking front. Why have further disasters been averted?

Undoubtedly, the Fed’s latest emergency intervention, the Bank Term Funding Program (BTFP), played a critical stabilizing role. This gave banks the ability to put up their heavily underwater government bonds, beaten down in price by soaring yields, as collateral to the Fed in return for loans. Crucially, they were valued at cost, not market value. It was another gift from the Fed to the banking system, but a small price to pay for preventing a systemic meltdown.

Not yet a paid Haymaker subscriber? Complete the brief survey linked below and we’ll set you up with a 90-day trial at no cost.

This did cause the Fed to once again expand its balance sheet, reversing the quantitative tightening- (QT) driven shrinkage. But that was temporary, and since then the Fed has resumed aggressively contracting its government bond and mortgage holdings. Considering it has been able to resume QT and that there have been no more bank runs and/or failures, the Fed must feel pretty satisfied with its latest triage efforts.

Another supporting factor was the pronounced decline in bond yields from the peak just under a year ago to the trough this spring as the Terrible Trio collapsed and even mighty Charles Schwab was rumored to be in trouble. That nearly 100 basis points (1%) decline in 10-year T-notes reversed a lot of the mark-to-market losses on which the banks were sitting.

The combination of these two events, along with a generally rising market, at least in a handful of names, produced a rousing 40% rally in the regional bank ETF. Crisis averted, right? …

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20231003