Making Hay Monday – November 27th, 2023

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Charts of the Week

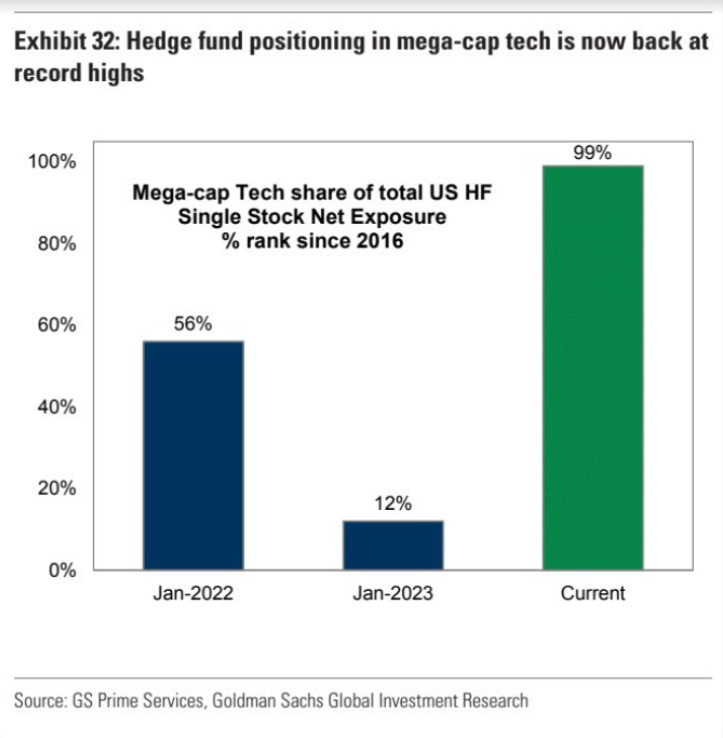

A recurring theme of this newsletter is that it’s hard to make money — and easy to lose it — when you follow the crowd into popular stocks and sectors. Based on the below image from The MacroTourist, Kevin Muir (one of my must-reads) mega-cap tech is as overcrowded as the Michigan football stadium was on Saturday. A key factor behind the exceptional performance of the Magnificent Seven, excluding 2022, has been the equally exceptional profits results of this elite cohort. To quote Kevin:

The earnings for these companies have been nothing short of mind-blowing, but as Peter Boockvar noted the other day…’People forget who are the MAG7 customers.’ If the economy continues to struggle, it is only a matter of time until it translates into weaker earnings for MAG7 as well.

Considering the current intense enthusiasm for what I often refer to as Heaven’s Seven, that is highly probable to lead to a nasty shakeout. (Note, for subscribers who’d like to read Kevin’s very relevant recent missive on this subject, we’ve included a link to that at the end of this Making Hay Monday. (Note: the piece is behind his paywall)

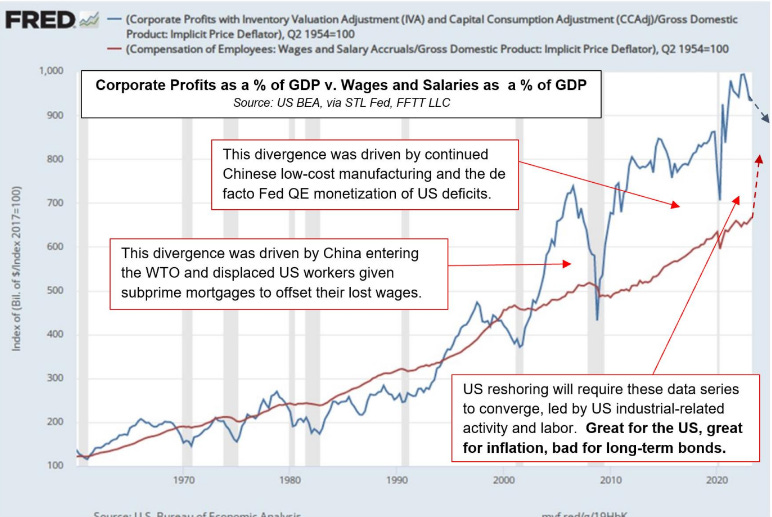

So far this century/millennium, corporate profits have grown at a much faster pace than wages and salaries. As you can see in the chart, below from the always-brilliant Luke Gromen, prior to 2000 there was a close correlation between the upward slopes of both of these critical GDP components. As Luke points out in his red box inserts, there is little doubt China’s inclusion in the World Trade Organization (WTO) was a major force behind this divergence. The “China Price” led to a considerable amount of America’s manufacturing base shifting over there, to the detriment of U.S workers (but the benefit of consumers who enjoyed low prices). However, the vertical upshift by mega-cap tech companies profits also has been one the primary drivers of this phenomenon.

Unfortunately for future S&P earnings, offshoring is now becoming reshoring with negative implications for profit margins and inflation. Also, should there be a recession, the MAG7’s net income is likely to suffer, though by varying degrees. (Microsoft may be better insulated that its magnificent peers.)

Evergreen Compatibility Survey

As Good as IT Gets?

“Everybody wants to show they owned all the winners—the Magnificent Seven—and that they didn’t own the losers.” -Dan Niles as quoted in this week’s Barron’s referring to year-end portfolio virtual signaling, also known as “window dressing”

“The Treasury market, oil and the Dollar are behaving as if the United States is heading into imminent recession, while stocks and Bitcoin are behaving as if risky assets are off to the races.” -Mike O’Rourke, Chief Market Strategist JonesTrading

Hopefully, nearly all Haymaker readers are aware of the extreme importance of multi-year breakouts and breakdowns. These are what some financial luminaries refer to as range expansions.

A highly significant case in point was Nvidia earlier this year. Unlike most highfliers from 2021’s mass mania in growth stocks, last May it managed to break above the $330 zenith it hit back then. Subsequently, it proceeded to rise another 50%, topping out at $505 just prior to reporting earnings this week.

Interestingly, though, despite releasing stunningly strong numbers, with revenues tripling and profits exploding by 1350% from a year ago, blowing away analysts’ highly optimistic estimates, the stock actually receded. It’s only been a 4% retracement, but it is now back near where it was trading in early September.

The driver of its glorious stock price performance — and even more stupendous earnings growth — has been, of course, the feverish excitement about AI. Because of Nvidia’s towering domination of AI chipmaking, no mega-cap company has been a bigger beneficiary of the intoxicating promise of what might be the biggest breakthrough ever in information technology, commonly known as IT. Considering how many paradigm shifting products the IT industry has bestowed upon the world, that’s a potentially hyperbolic statement. Yet, I think it is likely true, for better and, quite possibly, for worse. (The threat of solely AI-controlled — i.e. sans human direction — killer drones is merely one example of the plausible peril.)

Returning to range expansions, one of the challenges with capitalizing on upside breakouts is when to cash in some of the winnings that usually follow those occurrences. In the past, I’ve mentioned that a failure of the stock in question to respond favorably to good news is one tip-off that the bull run might be at least temporarily exhausted. When the news was as extraordinary bullish as Nvidia’s, I’d say that is particularly concerning.

Naturally, it’s entirely possible that it is merely consolidating after a $400 billion increase in its market value in a mere six months. Granting that as a decent likelihood, I still think it’s prudent for Nvidia holders to cash in some of their windfall gains. Please notice the word “some”. A fundamental reason this might be a wise move is that the semiconductor industry is notorious for experiencing double-, triple- and, even quadruple-ordering when an inventory deficit has developed. This happened in the wake of Covid when almost every sector, especially autos, was crippled to a degree by semiconductor chip shortages. Companies are so desperate to secure Nvidia chips right now that it’s hard for me to believe there isn’t a considerable amount of duplicate ordering happening. Perhaps in this case it will continue for more quarters, maybe even a year or more. But eventually there will be a deceleration, likely to a pronounced degree.

This Making Hay Monday, though, isn’t meant to solely focus on Nvidia. My theme for this week is a reprise of one I expressed back in late July; namely, that tech in general should be reduced in most investors’ portfolios. …

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20231128