Making Hay Monday – November 13th, 2023

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

Charts of the Week

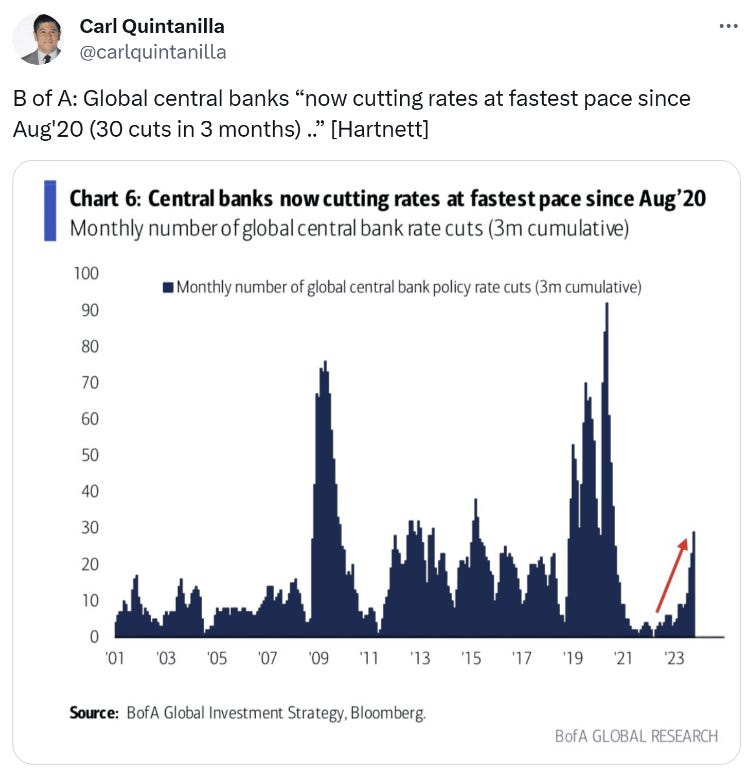

Emerging market central banks moved much earlier than their developed world counterparts when it came to raising interest rates as inflation soared. You may not be aware the same is happening on the easing front. As you can see below, courtesy of BofA’s razor-sharp Michael Hartnett, on a global basis central banks are slashing the cost of money at the most rapid clip since the summer of 2020. Other than New Zealand, the rest of these all appear to be in developing countries such as Brazil, Thailand and Vietnam.

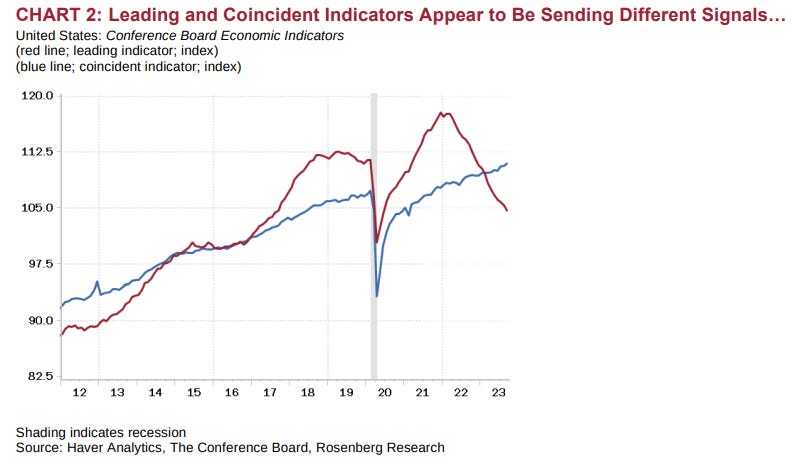

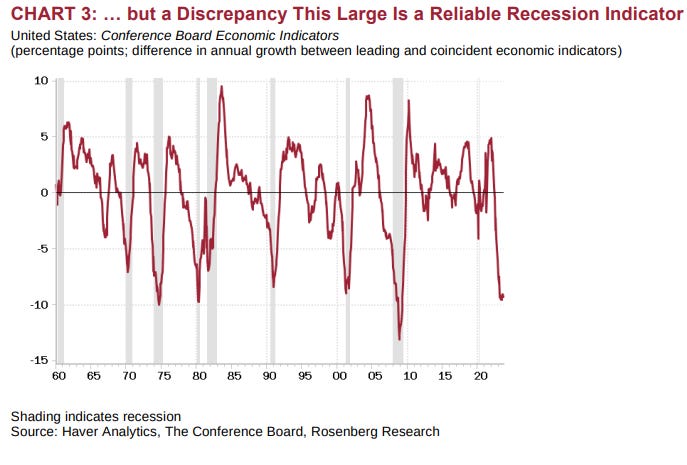

The Wall Street and economic tea leaf-reading consensus continues to be convinced that a soft-landing, if not a no-landing, scenario lies ahead. One of their supporting data points is the continuing rise by Coincident Economic Indicators. However, what they are ignoring is that when the divergence versus the Leading Indicators is as yawning as it is now, recessions have consistently been close at hand. Additionally, evidence is mounting that this year’s holiday shopping season is likely to be a lump of coal per this Wall Street Journal headline from over the weekend: This Holiday Season Is Looking Ho! Ho! Horrible

“It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is most adaptable to change.” -Controversially attributed to Charles Darwin

“When the facts change, so does my mind. What do you do, Sir?” -John Maynard Keynes

“The irrational exuberance, all the excitement about clean energy, is clearly getting squeezed out of a market that can no longer afford it,” -David Foley, Blackstone Senior Managing Director

Evergreen Compatibility Survey

Not So Electrifying

One of humanity’s greatest strengths is its ability to adapt to changing circumstances. That was an invaluable attribute in a world that once changed extremely gradually. Today, when paradigm shifts seem to happen every few years, it has become even more essential.

Perhaps that’s why capitalism, with its inherent tendency toward creative destruction — or, as Charles Darwin definitely didn’t say, the survival of the fittest — has repeatedly proven far more effective than communism and even socialism. Market forces are powerful and unforgiving, at least for those who fail to adapt to their shifting needs and preferences. As a result of this ruthless winnowing out process, society at large benefits to a great degree.

This reality is clearly playing out with regard to renewable energy currently. The most graphic example of this is with offshore wind. The number of projects being cancelled is becoming hard to track. The travails of this sub-set of the Great Green Energy Transition (GGET) can be vividly seen in the stock charts of two of the leading players in this field. (Vestas is a producer of wind turbines and related equipment while Oersted is the world’s largest developer and operator of offshore wind projects; the latter is particularly struggling presently.)

(Past performance is not indicative of future results)

Obviously, Oersted’s share price has fared significantly worse than Vestas’. The latter has “only” been cut in half while the former has collapsed by 75%. Vestas’ stock has also avoided breaking three-year support; clearly, Oersted shareholders haven’t been as fortunate; it decisively broke below 600 krone early this year. As is so often the case when key support is taken out, it has fallen another 50% since then.

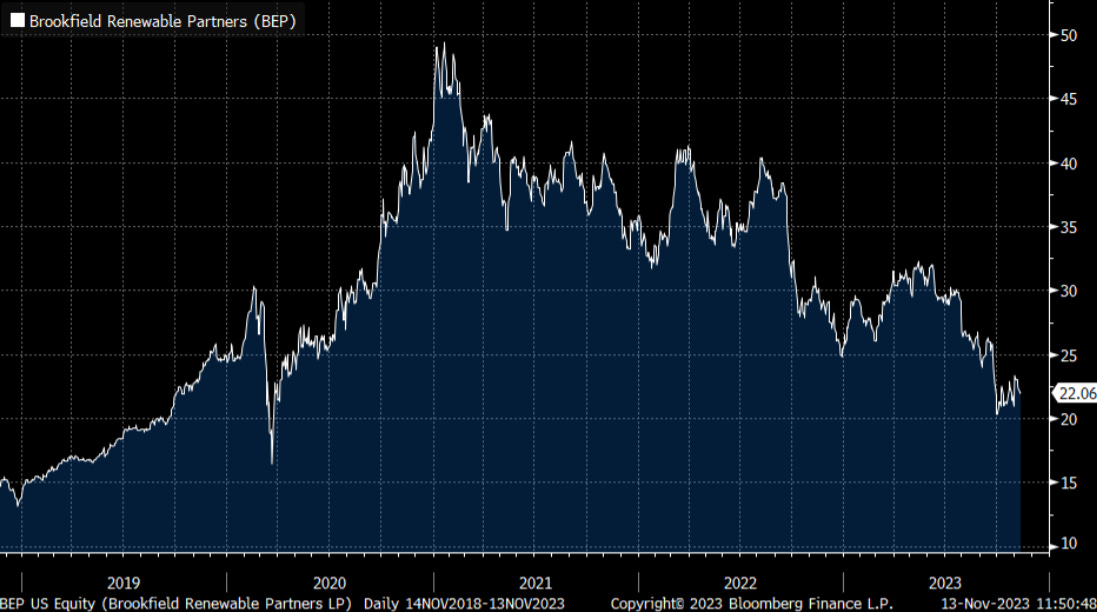

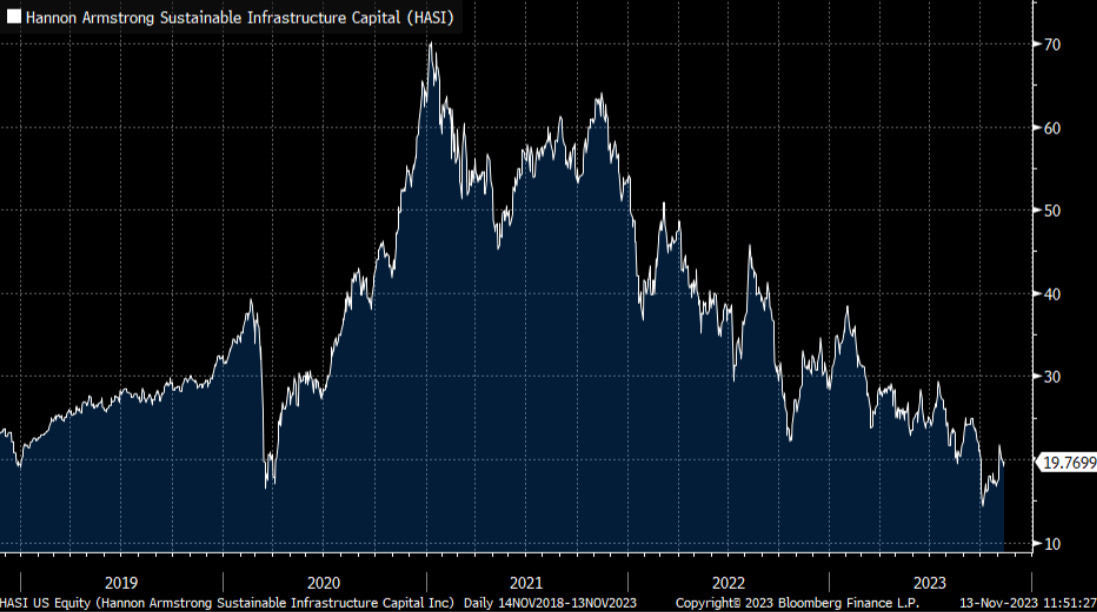

Yet, it’s much more than just trouble with offshore wind companies. Those that operate utility-like renewable energy facilities, such as solar farms and onshore wind, which is much less risky than off-shore, have been hammered. This is a point I’ve made before and the carnage has included one of my long-favored names that, in the past, was an extremely lucrative investment. The three others, with similar business models, have also been mercilessly punished.

(Past performance is not indicative of future results)

The suppliers of solar systems and critical components have not fared any better. It’s hard to believe that such devastation could have occurred at a time when trillions of dollars have been showered upon this industry. It’s becoming obvious that this is a sub-industry that needs to do some serious adapting to a much less hospitable environment.

(Past performance is not indicative of future results)

The above quartet of nauseating visuals is another example of multi-year support levels being broken followed by yet more value destruction. A pleasant exception is First Solar which is down a comparatively modest 43% from its early-2023 zenith; more encouragingly, it’s nowhere near breaking multi-year support. In fact, it remains above last year’s buy-signal breakout point. As market veterans know, prior resistance typically becomes a support level during corrections… and this has been a doozy of a correction. It does appear, though, that First Solar might be a capable adapter to the new realities.

The foregoing is disturbing enough for those who feel Net Zero is a feasible target — unsurprisingly for regular readers, I don’t — but what’s happening in EV-land is yet more worrisome. As I relayed on Friday, the proliferation of negative articles and televised news segments on EVs is remarkable these days. It’s enough to get my contrarian juices flowing, though I struggle with the EV makers’ valuations. In that regard, of course, Tesla is in a nosebleed class of its own. But at least it makes money, even if not enough to justify a market cap of almost $700 billion. That’s precarious on its own, but when combined with crashing profit margins and intensifying competition from Chinese EV producers, it’s downright dangerous, in my view. (TSLA better get that autonomous driving software debugged, ASAP.) …

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20231114