Making Hay Monday – February 20th, 2024

Making Hay Monday

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day’s financial fray.

“It has been said that history repeats itself. This is perhaps not quite correct; it merely rhymes.” -Theodor Reik (words to that effect are often mistakenly believed to have been spoken by Mark Twain — Our thanks to Quote Investigator)

Rhyme Time

Please humor me for a few moments while I highlight some eerie parallels. Perhaps I’ve missed them, but I haven’t seen anyone pointing out the number of similarities with current market behavior and what was seen almost exactly 24 years ago.

It was the late winter of 2000 when the tech-heavy NASDAQ was soaring to previously unimagined heights. This was after a run-up in the late 1990s that was even more feverish than what had held the prior record for American speculative excess: the end of the Roaring ‘20s.

Evergreen Compatibility Survey

Naturally, this isn’t like an AI-generated replica of what happened at the start of the 21st Century. There are, for sure, glaring differences, particularly when it comes to U.S. government finances. In those days, which now seem like several lifetimes ago, the then-Fed head Alan Greenspan was publicly agonizing that there would be no Treasury bond market by 2010. This was because the federal government was running large surpluses which Mr. Greenspan anticipated would continue indefinitely. In his estimation, it might only take a decade to retire all outstanding federal debt.

While he conveniently ignored the issue of trillions of unfunded entitlements, the fact of the matter is that U.S. Treasury bonds were the safest fixed-income instruments on the planet at that time. As we all sadly know, that situation has done a complete 180°.

Regarding the rhymes with February 2000, let’s consider what the Fed has been doing in recent years. As was the case back then, it has completed a long rate hiking campaign. Reflecting that, bond yields have risen significantly, as they also did at the end of the last century. Interestingly, they also fell sharply at the start of 2000, from 6¾% to around 5½% by the end of March of 2000. Undoubtedly, that helped provide the impetus for the final speculative blow-off top, arguably the most extreme in all of market history — at least until 2021. That bond rally was similar to what happened since last October when the 10-year T-note yield plunged from over 5% to around 3.8% in December.

Another rerun is that U.S. Treasury (UST) yields have risen considerably since that 3.8% trough. They are now back in the 4.3% range. The same thing happened in early 2000 when the interest rate on USTs zoomed from 5½% to 6½% in very short order. That may well have been another pin that punctured the massive bubble of those days, along with such outrageous overvaluation that a crash had become inevitable. The NASDAQ would fall nearly 80% by the time it hit bottom in 2002.

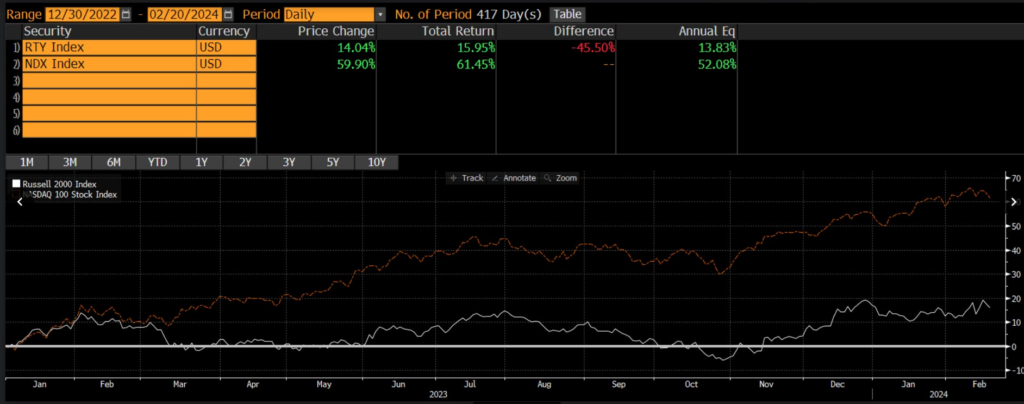

In addition to the fact that the late stage of the great tech mania was also led by a small number of stocks, there was another similarity related to this point. This was the comparative performance of the Russell 2000 (small cap) index versus the NASDAQ. As you can see below, the divergence between the two back then was enormous, as it is again today.

Russell 2000 vs. NASDAQ – Total returns from 12/31/1998 to 2/29/2000 – (Click chart to expand)

White Line: Russell 2000 | Orange Line: NASDAQ

Bloomberg

Total returns from 12/30/2022 Through Present – (Click chart to expand)

White Line: Russell 2000 | Orange Line: NASDAQ

Bloomberg

Subsequent to that, the reversal of fortune was equally dramatic. In fact, it would last for the next 14 years.

March 2000 NASDAQ Peak Through 3/15/14 – (Click chart to expand)

White Line: Russell 2000 | Orange Line: NASDAQ

Bloomberg

What if by some strange coincidence, we are on the verge of seeing a similar performance inversion? If we are, you might want to be reorienting your portfolio, at least to a certain degree. In other words, it may be prudent to be cashing in some monster gains on tech stocks and redeploying some of the proceeds into shares with much less ebullient valuations. An example you might want to consider will be discussed in the section immediately following for paid subscribers. (Also for those who help support the Haymaker mission, we’ll be sending out a short video this week on a legendary portfolio manager who is doing exactly that.)

As will be described behind the paywall, it’s not just tech stocks that are trading at extremely generous P/E ratios. Even certain elite retailers are trading at valuations reminiscent of the early-2000 era. Back then, that was also the case with stocks like GE, Gillette, and Coca-Cola priced at 40-50 times earnings — before they, too, had their return-to-reality experience. …

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240220