Macro Tides – “Watch the Dots”

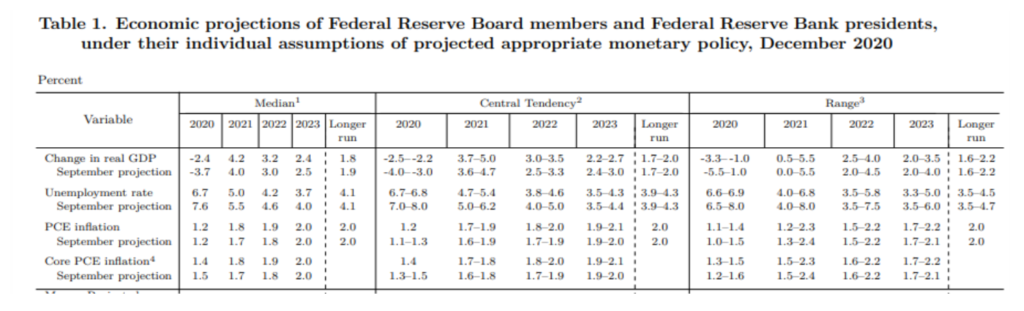

When the FOMC met on December 15 and December 16 last year there was a high level of uncertainty about fiscal policy and the speed of vaccinations. Congress didn’t pass the $900 billion Consolidated Appropriations Act 2021 until December 21 and the initial rollout of vaccinations wasn’t as smooth as hoped after the first dose was administered on December 14. The FOMC’s projections for GDP growth, Unemployment rate, and inflation reflect the widespread uncertainty present last December.

As the FOMC meets on March 16 and March 17 much of the uncertainty has been replaced by visibility and good news. Congress has passed a total of $2.8 trillion in fiscal stimulus which will give the U.S. economy a meaningful lift in 2021 and 2022. The speed of vaccinations has accelerated and by mid 2021 the majority of American adults will be vaccinated, so the reopening of the U.S. economy is no longer in doubt. Members of the FOMC will raise their projections for GDP in 2021 and 2022, lower their estimate of Unemployment, and potentially pull forward into 2022 the expectation that Core PCE inflation will hit 2.0% and possibly 2.1% in 2023. The Treasury market may not like these upbeat changes.

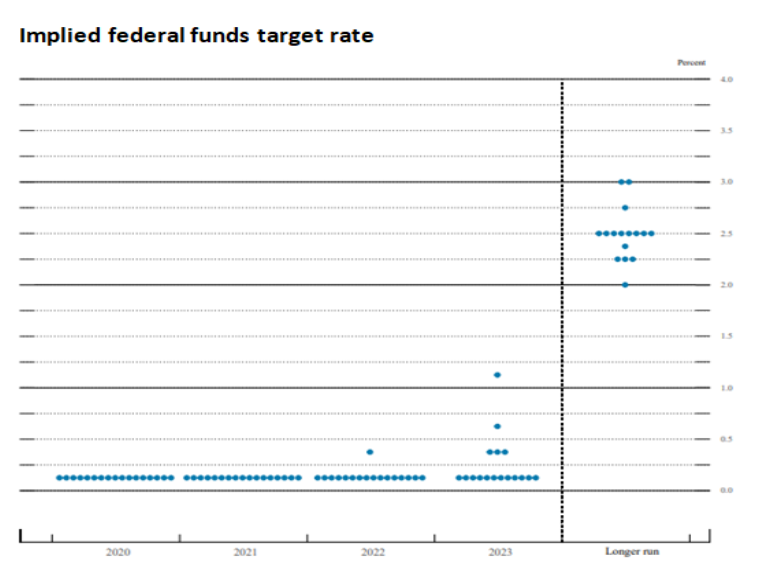

I reviewed the FOMC’s Dot Plot from their December 2020 meeting in the January Macro Tides. The Dot Plot illustrates when each of the 17 members of the FOMC expect the federal funds rate to be increased. Only one member supported an increase in 2022, while 3 members expect the funds rate to be 0.375% at the end of 2023, with one member projecting the funds rate at 0.625%, and one looking for the funds rate to be 1.125%. The other 11 FOMC members were projecting no increase in the fed funds rate until after 2023. With Congress passing the $1.9 trillion stimulus bill and vaccine progress accelerating, the FOMC’s Dot Plot is likely to change with more members projecting at least one increase before the end of 2022. If correct, Treasury yields may tick higher and lead to another decline in the Mega Cap stocks which have responded negatively to higher Treasury rates.

During his post FOMC meeting press conference Chair Powell is going to reiterate the FOMC’s commitment to keep rates down so unemployment can fall and tolerance of any pick-up in inflation toward its target of 2.0%. Chair Powell will restate the Fed’s expectation that the coming rise in inflation is likely to be temporary, so the FOMC will not react by hiking rates, even if the Core PCE is above 2.0% for a period of time.

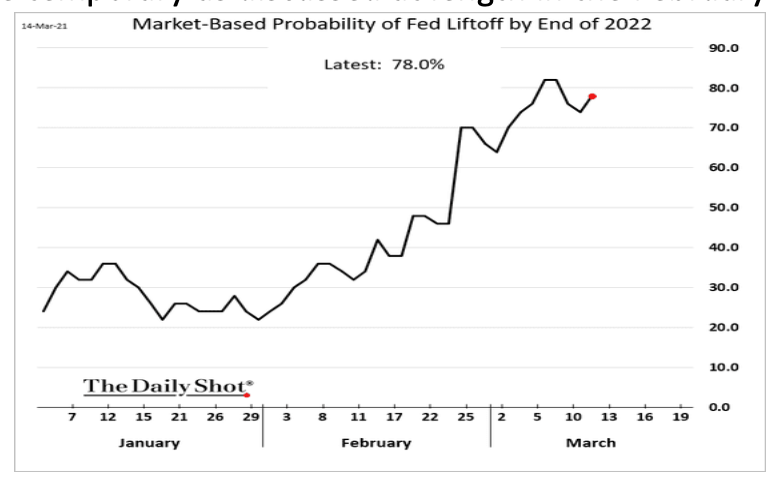

The coming bout of inflation is likely to prove temporary as discussed at length in the February Macro Tides. However, in the next few months inflation surprises are likely to be higher than expected. When the CPI for April is reported in May, the headline CPI inflation will be north of 3.0%, and could approach 3.5% when the data for May is reported in mid June. As the inflation data becomes less sanguine, the federal funds rate market will begin to price in more rate hikes and earlier in 2022 than projected by the FOMC’s Dot Plot.

With the prospect of higher Treasury yields in coming months, some market participants are eager to hear if Chair Powell hints about the FOMC implementing Yield Curve Control (YCC), which would be expected to minimize any increase in Treasury yields. I doubt Chair Powell will provide even a hint that the FOMC is considering YCC anytime soon. If correct, the Treasury market may be disappointed and sell off.

Jim Welsh

JWelsh@SmartPortfolios.com