Haymaker Friday Edition

Haymaker Friday Edition

“History never looks like history when you are living through it.” -John Gardner, as quoted in Neil Howe’s The Fourth Turning Is Here (Not to be confused with the Mr. “Gardiner” referenced below)

“Washington in general has a very relaxed attitude towards debt that I think they’re going to be sorry about.” -Ken Rogoff in a recent Bloomberg TV interview.

“… growth in the spring.” (see below) – Image: Shutterstock

The first question to be asked at the outset of what I intend to be a multi-part series on the phenomenon I’ve been calling “The Great Disconnect” is if there is any such thing? (Part I is open to all, as it’s a topic of deep significance to me.) Specifically, because this newsletter is almost exclusively about investing, is there truly a chasmic — perhaps even cosmic — divide between financial markets and what’s transpiring in the real world?

While most of Wall Street these days seems inclined to answer those questions with another one — as in, “Who cares?” — I believe that is both a dangerous and short-sighted attitude.

At some point, history is clear that fundamentals do win out. Or, as Warren Buffett’s mentor, Benjamin Graham, long ago observed, in the short-run the stock market is a voting machine, but in the long run it is a weighing machine. Eventually, the popularity contest succumbs to reality, for better or worse. When it comes to asset markets that are priced as if the skies will always be topaz blue, even as the dark clouds gather, it is almost always “or worse”.

On that score, there have been numerous instances, including recently, in which I have chided The Economist for its star-crossed cover stories. On March 18th, it ran the below issue.

The Economist

Admittedly, it might seem like I’m unfairly picking on the UK’s august magazine, particularly since it has admirably stood the test of time. As far as its extraordinary longevity, you may be surprised to learn that it has been around since 1843. That’s a long, long time ago — even before either Joe Biden or Donald Trump were born. Yet, it has repeatedly proven its ability to call the top or bottom of major trends with its covers. Unfortunately for its credibility, The Economist has typically been on the wrong side of the trend reversals.

When it comes to the U.S. economy, it’s fair to say that it has surprised those of us who have been expecting a recession with its ability to keep on keeping on. This has been despite a long list of economic forcings that usually lead to downturns. Those include one of the longest-lasting yield-curve inversions in history, a renewed banking crisis, an utter meltdown in important parts of the real estate market, and 23 months of falling Leading Economic indicators (until lately).

Despite all that, America’s economy has been pumped-up indeed. However, you don’t need a PhD in chemistry to discover the magical elixir that has created the muscular appearance shown above: The U.S. government has been self-injecting fiscal steroids at a rate than could have transformed Paul Reubens (Pee-wee Herman) into Arnold Schwarzenegger.

Of course, as with all artificial stimulations, there will be a day of reckoning. In the meantime, though, it is creating a radical divergence between A) the economy most Americans are experiencing, and B) the one The Economist is inistently celebrating.

The venerable economist David Rosenberg addressed this in his April 3rd Breakfast with Dave:

We have reached a state of budget-busting that the U.S. is now beginning to look more like a bastion of socialism than free-enterprise capitalism… Everyone marvels at how wonderfully the U.S. economy is doing… (Yet) nearly all the growth has come via the government sector, both directly and indirectly.

To illustrate his point, please realize that some 90% of the increase in nominal GDP (this includes inflation, which is rising again) is coming from deficit spending. In other words, if you back that out, the private sector is basically at stall speed.

David then compared America’s current 6% fiscal deficit (which, in dollar terms, is likely to exceed $2 trillion this year) to other countries. It’s a pretty sad story, particularly considering the U.S. remains the world’s leading superpower (for now). As he wryly noted, the U.S. is starting to resemble a Banana Republic. To wit:

Government deficit-to-GDP:

Ecuador -0.9%

Chad -1.2%

Chile -2.4%

Mexico -3.4%

Peru -3.6%

Columbia -4.1%

Bangladesh -5%

America’s 6% deficits, at a time when the economy is growing and the jobless rate is near record lows, is indefensible. But it’s also inarguable and it puts the U.S. in the same sorry league with Uganda, Kenya, and India. Even the infamous PIGS — Portugal, Italy, Greece, Spain — from Europe’s debt crisis Hall of Horrors of 12 years ago, put the U.S. to shame. Portugal is, remarkably, running a budget surplus. Spain’s red ink is just 1.2% the size of its economy. Last decade’s ultimate basket case, Greece, is at -1.7%. Even Europe’s current sick man, Italy, is at -3.1%, just half of America’s number.

It’s my belief that Americans realize something is rotten… and it’s not in Denmark (which also is running deficits roughly half of the USA’s, as a percentage of GDP). Most realize that the rot lies in Washington, D.C., and its spend-happy, vote-buying politicians from both parties (a note on political partisanship follows today’s main section).

In fairness to The Economist, the article that accompanied its buff-America cover story pointed out that our pandemic-fighting stimulus was double that of the rich-world average. It also stated that over the last year the actual deficit-to-GDP was closer to eight percent than six. (The number I’ve more frequently seen is around seven percent.)

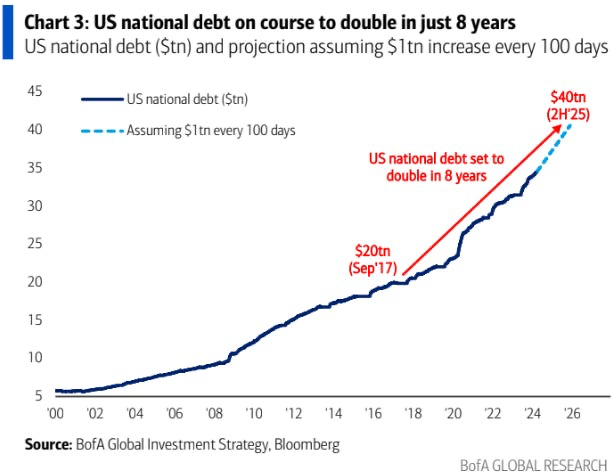

What’s actually much more disturbing is that per both David Stockman (the Reagan administration one-time budge savant) and BofA’s Michael Hartnett, America’s national debt is increasing $1 trillion every 100 days. Note that this tracks Treasury issuance, not officially reported deficits.

One could argue this is a more realistic statistic than the figures the U.S. government’s accountants produce since this what’s actually being raised. However, it is fair to note that the Treasury’s checking account, its General Account (TGA), has been replenished to the tune of $500 billion recently. So, perhaps the “real” issuance has been running at about $1.5 trillion over what will soon be the first 200 days of this federal fiscal year (which started 9/30/23). That still annualizes at well over $2.5 trillion, or about 8% of GDP, close to The Economist’s figure.

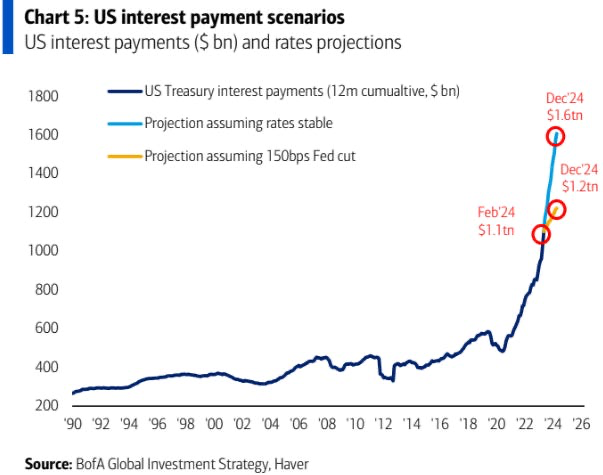

As Michael Hartnett pointed out in his March 28th weekly missive, The Flow Show, America’s national debt is on track to double in just eight years, as shown in his chart below. He also shared one on the hockey stick-like increase in U.S. interest payments. As you can see, by the end of this year, he has those running at $1.6 trillion. As recently as 2020, these outlays were in the vicinity of $600 billion.

Shockingly, the U.S. government’s interest expense will soon double defense spending.

Hartnett

Hartnett

All Americans with a modicum of common sense (naturally, that excludes members of the administration and Congress) realize this is both unsafe and insane, not to mention totally unsustainable.

Yet, they look at the stock market, which has been hitting new highs, and they wonder if this stunning example of The Great Disconnect is simply the way the world works these days.

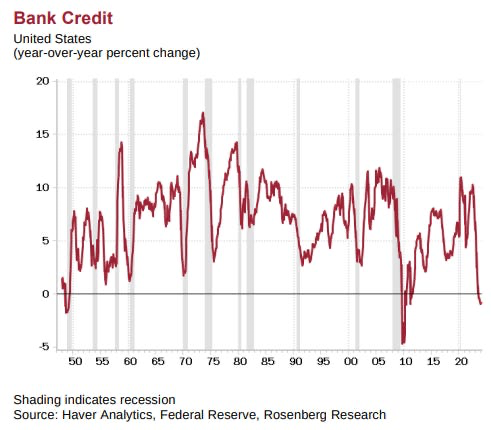

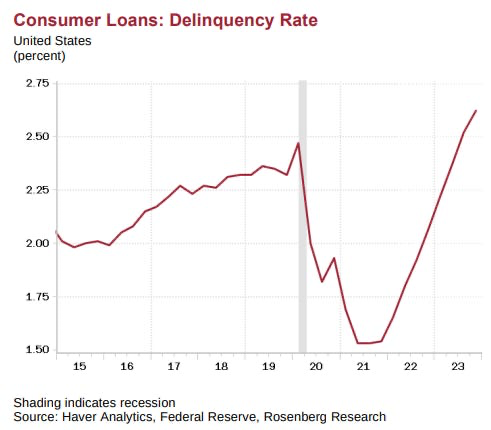

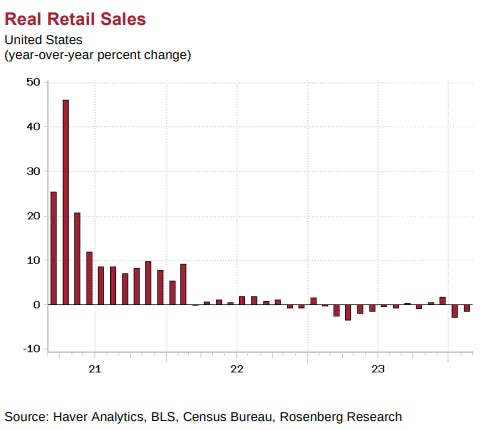

If they dig a bit deeper, like by reading David Rosenberg, they’ll pick up on some other disconnects. The trends in Bank Credit (down), Consumer Loan Delinquencies (up) and Real Retail Sales (akin to the EKG of a cadaver) are three cases in point. (Those who ascribe to my breakout/breakdown theories, including with economic data, will note the ominous signal from the first two charts.)

Rosenberg

Rosenberg

Rosenberg

It doesn’t stop there. As David wrote in a recent Breakfast With Dave:

I have to say that in my 40 years in the business, I have never seen so many divergences and discrepancies in the economic data.

Consider these dichotomies (Year-over-Year % changes):

Nonfarm payrolls: +1.8%; Household Survey employment: +0.4%

Part-time employment: +3.4%; Full-time employment: -0.2%

New home sales: +5.9%; Existing Home Sales: -3.3%

Single-family housing starts: +5.9%; Multi-family housing starts: -35.9%

Manufacturing construction (Biden subsidies!) +31.9%; Manufacturing production: -0.7%

Real consumer spending: +2.4%; Real retail sales: -1.6%

It’s fair to say, I think, that divergences, discrepancies, and dichotomies are synonyms for disconnects and I’m right there with him. This David — as in, the Haymaker — has been in the investment business for 45 years and I’ve never witnessed such a disparity between conditions that usually have a large degree of synchronicity.

My plan for this series on “The Great Disconnect” is to create a string of missives, comparable to short chapters in a book, that will typically run every other week, though that cadence may get thrown off at times. The ultimate objective is to make this series into a coda or addendum to my book Bubble 3.0. As many of you are aware, we digitally published it in early 2022, right before that speculative mania — arguably, the most hyper-inflated of all-time — imploded.

Of course, since the fall of 2022, Bubble 3.0 has done an encore performance. It’s reasonable to wonder if this is Bubble 4.0 or if it’s just a continuation — an echo, if you will — of Bubble 3.0. Regardless, it’s my contention that the helium that has refilled it has been the trillions of U.S. government red ink over the last year and a half. That monstrous mountain of synthetic liquidity has allowed the stock market, and certain important parts of the U.S. economy (but certainly not all), to disconnect from normal gravitational forces. For those sectors that have been in the sluice-path of the enormous torrent of government largesse, it’s all systems go. For those that aren’t, like the bulk of small businesses — America’s ultimate job engine — it may not be full-stop, but many are slowing, if not running in reverse.

Undoubtedly, some, if not most, Haymaker readers believe I have an obsession with what I’ve been calling my 4-F scenario: the Federal Fiscal Funding Fiasco. Frankly, I’m guilty as charged. In my view, it’s the main reason for our current illusion of economic and financial market vitality. As I’ve previously written and said, it’s a case of pseudo-prosperity. My overarching advice to all of you is to enjoy it while it lasts. As Herb Stein (Ben’s dad) said decades ago, “If something can’t go on forever, it will stop.”

But when?

Obviously, I don’t know, but I’d strongly suggest you track the long-end of the bond market for clues as to when the jig will be up for the deficit-spending-driven boom times. (As regular Haymaker readers are aware, I believe there are market segments that are well-positioned to benefit from a spreading realization that the U.S. government is nearly certain to use inflation to cope with the 4-F scenario. You may have noticed that those, like energy producers and gold miners, have come alive lately.)

There’s a lot more to cover on this subject, with new information emerging daily. In future Haymakers on “The Great Disconnect” I’ll be drawing on a book I recommend all of you read: Neil Howe’s The Fourth Turning Is Here.

For now, I’ll wind down this edition with a brief quote from Howe’s magnum opus: “Opinion surveys suggest that the most prominent feature of (America’s) mood is almost unrelieved pessimism about the nation’s future.”

How that observation, which I think most of us realize is not inaccurate, squares with the U.S. stock market representing 70% of global market capitalization is, to me, the essence of The Great Disconnect.

The good news is, as “Chauncey (Chance, actually) Gardiner” famously said in Being There: “Yes. There will be growth in the spring.” Spring will come again to America but we need to be realistic — and prepared — about the prolonged winter season in which we currently find ourselves.

“Chauncey” and the President (perhaps Jack Warden would have been a No Labels supporter) – Image: IMDb

As the old saying goes, forewarned is forearmed.

P.S. On No Labels’ recent announcement…

As most Haymaker readers are aware, I have been a strong supporter of No Labels, the bipartisan movement attempting to restore balance and rationality to American politics. The main focus of its recent efforts has been to field a “Unity Ticket” comprised of one Democrat and one Republican to run for America’s highest office. But, as perhaps you’ve learned, it is abandoning its campaign.

Those who felt No Labels’ mission would fail often cited the inability to get on enough state ballots. That, surprisingly, was not the problem. Rather, it was the reluctance of electable candidates to run, particularly at the top of the ticket. The reasons were varied, but the bottom line is no one with a compelling national profile was willing to incur the wrath of the political establishment and the attacks on themselves and their families. Frankly, much of the blowback, including from the media, was appalling. Moreover, in my view, it was of a most undemocratic nature.

For me, this is a heart-breaking outcome for America. Roughly two-thirds of our citizens have told pollsters they don’t want to see a Biden/Trump rematch. But that’s exactly what we’re facing though third, fourth, and even, fifth, party candidates may play the role of “spoiler”. Frankly, I’m not sure which way that will tip the electoral scales come November. But, now, No Labels won’t be blamed for handing the presidency to either Trump or Biden.

In fact, true to its word, No Labels has elected to stand down rather than merely seek to be a disruptor with almost no chance to win such as with Ralph Nader in 2000. However, it will continue to be active in the presidential election process by holding both candidates accountable to accuracy and unifying policies. It’s safe to say No Labels will have its hands full in that regard.

Please accept my deep thanks to those of you who offered your support to this great cause. The fight is not over, nor will it be as long as American politics are dominated by forces that don’t reflect the will of the Common Sense majority.

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240406