Haymaker Friday Edition

Haymaker Friday Edition

Courtesy of my great mate, Grant Williams!

“In ten years, Tesla will be the largest and most profitable company in the world,” -Billionaire money manager Ron Baron, November 4th, 2022.

“Buying a car today is an investment into the future. I think the most profound thing is that if you buy a Tesla today, I believe you are buying an appreciating asset – not a depreciating asset.” -Elon Musk, April 2019

“I am uncomfortable growing Tesla to be a leader in AI & robotics without having ~25% voting control.” -Elon Musk, January 15th, 2024

Is It Dusk For Musk?

Today’s Guest Haymaker edition is a special one that we’ve been eager to share since last month. My dear friend and longtime industry peer, Grant Williams, has turned out an especially comprehensive look at the myriad challenges besetting Elon Musk and his convoluted collection of business endeavors (some over-hyped, some semi-hyped).

One of the great strengths of any piece Grant publishes is the sheer scale at which he presents his ideas in his missives… or, more precisely, his “Things That Make You Go Hmmm”. For those of you who know your film history, Grant is to the finance journalism world what Cecil B. DeMille and David Lean were to mid-20th century cinema — hint: neither of those men were known for shooting small-scope pictures.

It’s also something of an Achilles’ heel for our newsletter, as we tend to publish more in the medium wordcount range. Our solution in this case is to do what we’ve done before: run a selection of especially compelling excerpts to capture Grant’s major points and keep your read-time at ~10-15 minutes.

Below you’ll find a solid sampling of Grant’s February newsletter titled, very fittingly, Claims Adjustment. Most of you know the Haymaker team has had plenty of criticisms to lob at Elon Musk over the years, with new fodder coming to light on a regular basis. We also understand and respect that many of our readers may have an affinity for Mr. Musk based in large part on his sociocultural pushbacks and apparent willingness to ruffle feathers in the top political ranks of our republic. He certainly does do that, and we appreciate his non-conformist streak since the Haymaker is often accused of the same proclivity.

For our part, we tend to focus (as does Grant in his newsletter) on the excesses and unforced errors of which Mr. Musk is guilty in the business, rather than the political realm. That might not be good enough for anyone who finds him beyond reproach because of his penchant for pissing off powerful government officials. However, our aim in sharing this work is primarily to shine a light on some excellent analyses of Mr. Musk’s balance sheet struggles and legal perils.

Coincidentally, Wells Fargo analyst Colin Langan attracted intense media coverage on Wednesday due to his downgrade of TSLA stock to an underweight (Wall Street code for a sell rating). In the process, he lowered his price target to $125 versus its current quote of $165. A pithy soundbite from Mr. Langan’s report called TSLA “a growth company with no growth”. He also lowered his earnings estimate for this year to $2. You may do some quick math and realize that means it is trading at almost 83 times his projection. Perhaps even worse, he expects profits to decline in 2025. To his point, that’s not what growth stocks are supposed to do; said differently, lofty P/Es and declining profits go together like EVs and power outages.

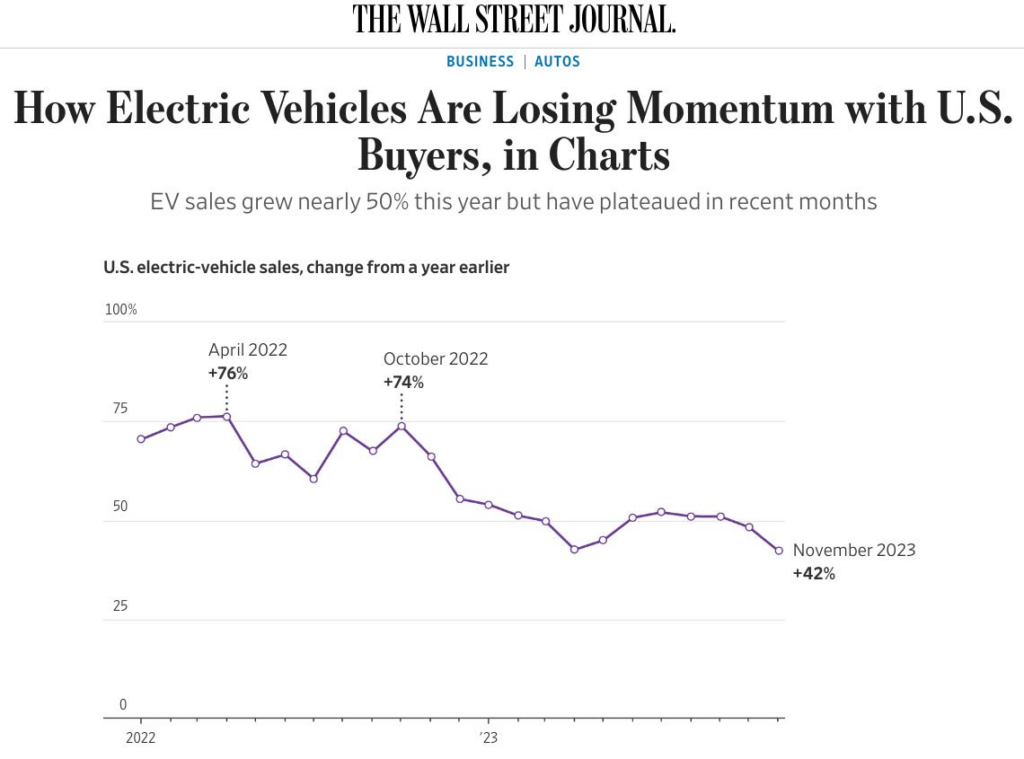

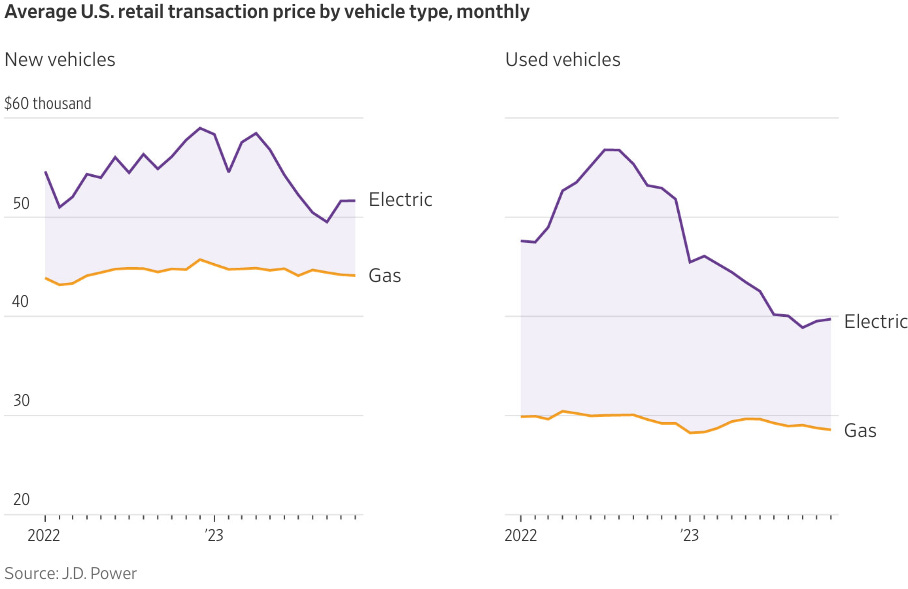

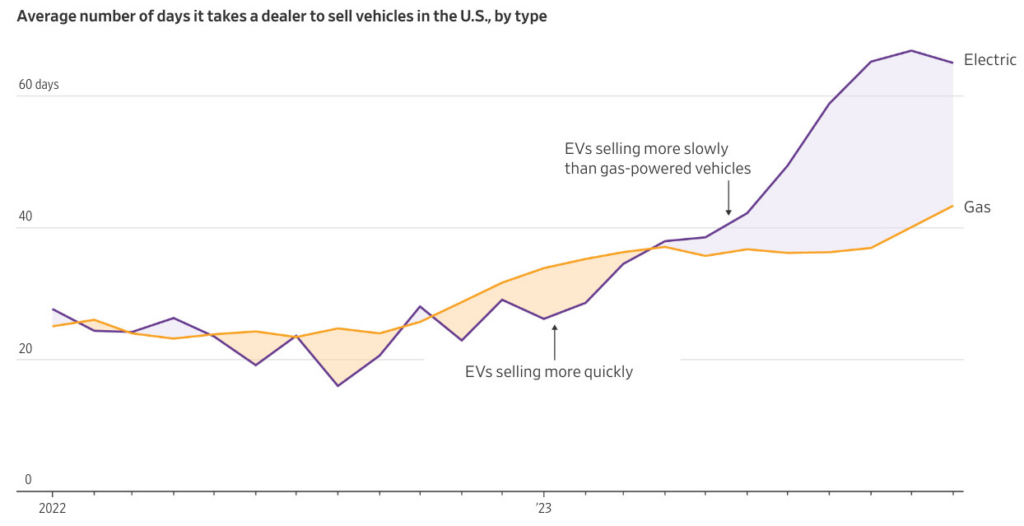

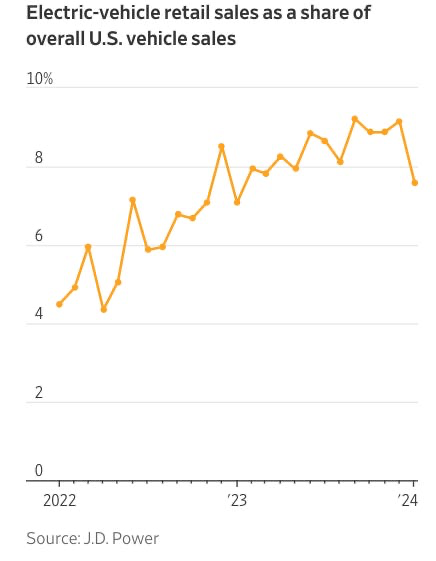

Reinforcing Mr. Langan’s concerns, EVs in general are encountering a previously unimaginable reality: consumers are falling out of love with them. As you can see, despite repeated price cuts, which hurt re-sale values, EV sales growth is decelerating. Unsold inventories are far higher than their internal combustion (ICE) rivals. Moreover, the price reductions have failed to reverse market-share losses.

WSJ

WSJ

WSJ

WSJ

In China, TSLA’s most important market, blistering growth has not only slowed, it has gone into reverse. Last month’s sales were one-third below their December levels. This appears to be more than just a normalization from year-end strength because February sales were off about 25% from January. Its China woes are being magnified by brutal competition from Chinese EV producers. Price cuts over there have become widespread and show no signs of ending.

Back here in the States, TSLA is also slashing prices. That may get worse before it gets better, as well. Per the Financial Times, Chinese EV manufacturers may be able to sell new vehicles in America at $26,000, even inclusive of a 25% tariff. TSLA’s average car price last year was about $45,000.

But the risks to TSLA go well beyond the foregoing factoids. Mr. Musk’s manifestly erratic behavior, which may be a result of his reported drug use, is alienating much of his core customer base. It also has repeatedly placed him in hot water with the SEC. As you will read soon, he is dangerously flirting with securities fraud, something he may already have committed numerous times. He may want to review the legal history of Martha Stewart — not to mention, Trevor Milton’s — as to the advisability of thumbing one’s nose at the SEC. This is particularly the case when he has gone out of his way to alienate various elements of the U.S. government. His demand for a massive compensation increase, in terms of additional shares of TSLA, when he already owns $100 billion worth, is rankling even some of his diehard fans.

Okay, I don’t want to steal too much of my friend’s thunder. Before getting to some of his key excerpts, a formatting note: Grant quotes larges bodies of text in his own work, text which he bold-fonts and italicizes to set it apart from his own words; a sort of belt-and-suspenders approach. We would normally block-quote such extensive passages, but as that would amount to a belt-suspenders-and-extra-suspenders approach, we have refrained from doing so here. The formatting appears as it does in the source document.

Now, treat yourself to some insightful excerpts from the work of a brilliant friend.

The Haymaker Team

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240315