Haymaker Friday Edition

Haymaker Friday Edition

ATTN OIL BULLS: HOLD FAST

“The fourth quarter was… the highest quarterly demand figure ever…. We are in a challenged environment for non-OPEC supply.” -Cornerstone Analytics’ Mike Rothman from his weekly podcast, released this morning, on the state of the oil market.

Charts of the Week

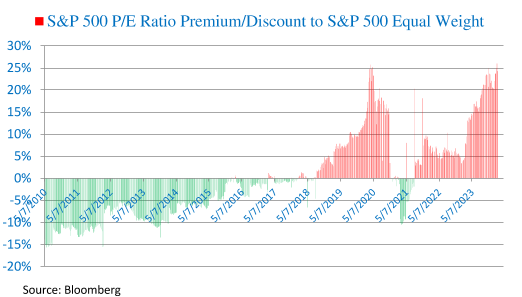

The ongoing dramatic outperformance by most of the Magnificent Seven has created a similar yawning divergence between the capitalization-weighted earnings of the S&P 500 and the equally-weighted S&P. Because such a large percentage of the S&P is presently comprised of mega-cap stocks, mostly tech, these highly valued companies have significantly increased the P/E ratio for the cap-weighted S&P compared to the P/E for the average of all 500 companies. This gap is likely unsustainable, comparable to the situation 24 years ago as the great tech bubble of that era was poised to pop.

O’Rourke, The Closing Print

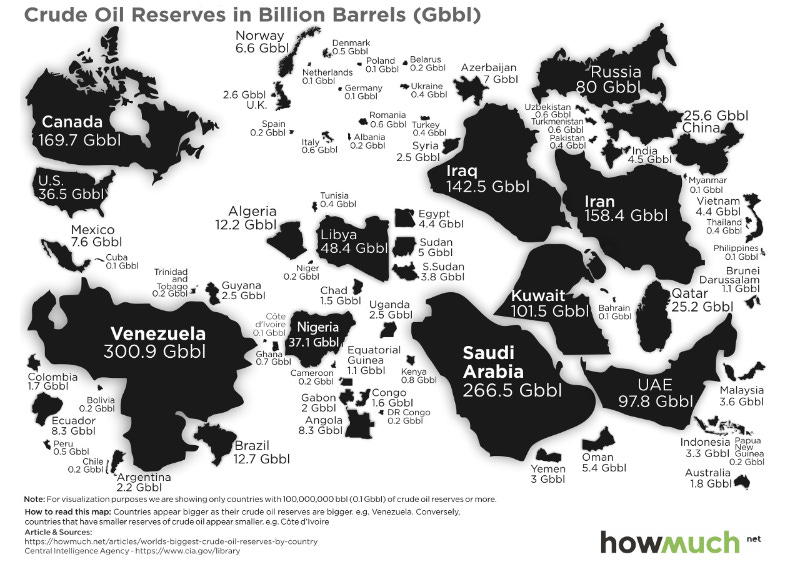

Befitting this week’s oil theme, I thought the below visual (admittedly, not a chart) to be fascinating. It’s an older image from 2019 I haven’t seen before, comparing oil reserves among major producing nations. What’s extraordinary about this is how modest U.S. oil reserves are compared to countries like Venezuela and Saudi Arabia. Despite this resource limitation, the U.S. is now the world’s largest oil producer. (As noted in prior Haymakers, Venezuela’s production has collapsed to below one million barrels per day, or bpd.) Thanks to the “shale revolution”, as a result of the combination of hydraulic fracturing (fracking) and horizontal (vs vertical) drilling, U.S. crude oil production has risen from just 5 million bpd to 13 million bpd. Natural Gas Liquid (NGL) output has swelled from roughly 2 million bpd to around 6 million bpd; i.e., it has tripled. (As discussed in the main body of this note, NGLs have numerous important uses, but a barrel of NGLs is not equivalent to a barrel of oil, particularly from a price standpoint.) America has been punching above its energy weight thanks to its prolific shale oil (and gas) basins, but nearly all of those are now in decline mode. As far as crude production goes, only the Permian is still growing… barely. It may well peak this year, with major future supply implications. As a reminder, virtually all of the world’s net oil output growth since 2007 has come from the U.S., a truly amazing reversal of fortune.

Evergreen Compatibility Survey

No Time For Energy Chickens

Shutterstock

Let me be the first to admit that the man behind the Doomberg avatar, which includes his now famous green chicken, is smarter than I am. In fact, I believe he possesses one of the keenest minds in the financial media world. For one thing, he has an exceptional background in chemistry. He is also a gifted writer, as well as a skilled verbal articulator of his beliefs. As a result, his podcasts are as good as his newsletters. Consequently, if you’re not a subscriber to his service, you may want to consider rectifying that omission. (In case you think his voice sounds strange, realize he uses a voice synthesizer for anonymity reasons.)

If you suspect these well-deserved accolades are a lead up to some points of contention, you are on the mark. Because Doomberg is both a friend and mentor of mine, taking issue with one of his strongest-held convictions is both daunting and intimidating for me. However, he has challenged one of my most firmly held beliefs — namely, that we remain in the midst of the third serious energy crisis of the last 50 years.

Before I make my case, I want to clearly state that I respect the deep thinking Doomberg has put into this issue, one I feel is of high importance to both investors and consumers, which includes almost everyone (after all, who doesn’t consume energy?). Unquestionably, the recent series of missives and podcasts he’s done on his new thesis about the myth of peak cheap oil has created tremendous blowback. Candidly, that’s more than a bit ironic considering that, if he’s right, it’s good news for the economy and energy users. Moreover, what’s been most distressing to me is the harshness of the criticism he’s received. This includes one energy pundit who has accused him of “going off the rails”.

A much more respectful and, accordingly, persuasive dissenting set of views was expressed by Adam Rozencwajg, the “R” in the highly respected energy research firm, G&R. Another friend, and another Adam, also a financial media star, Adam Taggart, recently did the investing public a great favor by recording their sometimes opposing, often agreeing, views last month.

Befitting their classy personalities, both were extremely respectful of each other. Yet, clearly, Adam R. has come to a very different set of conclusions on several key points. It shouldn’t come as even a mild, static electricity-like shock that I’m in sync with Adam R.’s outlook. This is an important enough subject that I plan to follow in Doomberg’s footsteps by publishing a series of articles on the Peak (or not) Cheap Oil debate. (Ironically, it was he who helped me select my own avatar, the Haymaker. Further, if Doomberg is willing, I’d love to give him the chance to respond in writing or via recorded debate to my various areas of disagreement.)

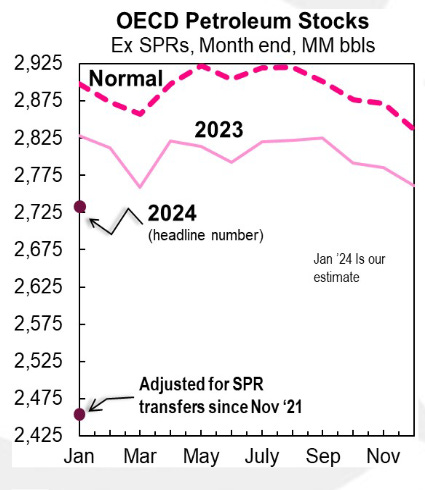

From a high-level standpoint, one of my first opinion divergences has to do with Doomberg’s belief that we are in an era of energy abundance, not one of shortages. Rather than taking my word for it, let’s check out this chart from Cornerstone Analytics, a firm that is a pure oil market specialist. (Like me, Doomberg is more of a generalist; thus, he’s at a bit of a disadvantage versus energy-centric entities like G&R and Cornerstone.)

Cornerstone Analytics

The key aspect of this is that it adjusts for the nearly 300 million barrels that have been released by the Biden administration since the invasion of Ukraine. Most observers fail to do this and, in fact, Doomberg did not bring this up in his podcasts or in his writings. To me, that’s a glaring omission. …

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240217