Haymaker Friday Edition

Haymaker Friday Edition

A broad, insight-packed presentation of high-finance, economic, and industry/stock charts from the Haymaker and his top-notch external resources.

“The advocates of public control cannot do without inflation. They need it in order to finance their policy of reckless spending and of lavishly subsidizing and bribing voters.” -Ludwig von Mises, 1912 (quote courtesy of Danielle DiMartino Booth)

Evergreen Compatibility Survey

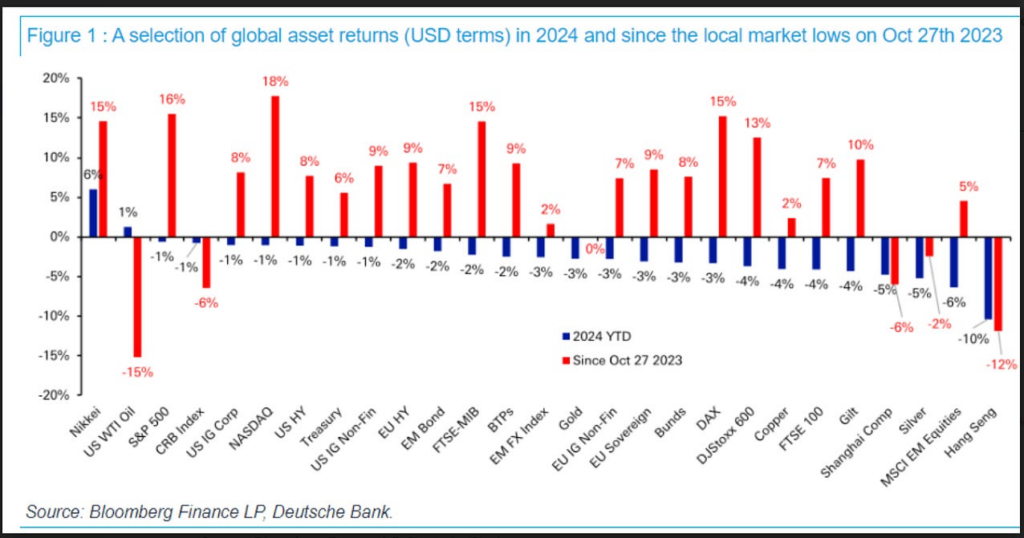

- 1. Market lore has it that January sets the tone for the full year. If this month continues to be soft, that doesn’t bode well for much besides Japanese stocks and the beaten-down oil market. However, two weeks is a long time in the stock market and a lot can change between now and month’s end. Lending credence to this theory, since 1950 up, Januarys have led to positive full year returns 85% of the time. Skeptics point out that the market rises in 7 out of 10 years, rendering the January Indicator a bit less impressive.

Reid/Deutsche Bank

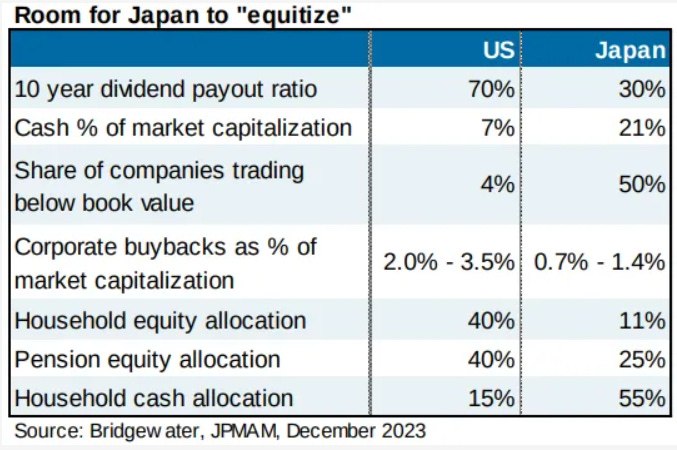

- 2. Even though the Japanese stock market has been outperforming the S&P since the start of 2022, at least in yen terms (its weakness versus the dollar has masked that for U.S. investors), there are solid reasons to believe the rally will continue. Per the table below, it’s clear that the 30-year bear market in the Nikkei created an exceptionally undervalued condition. Japanese household allocations to equities are particularly noteworthy, particularly because they have massive cash holdings.

Cembalest

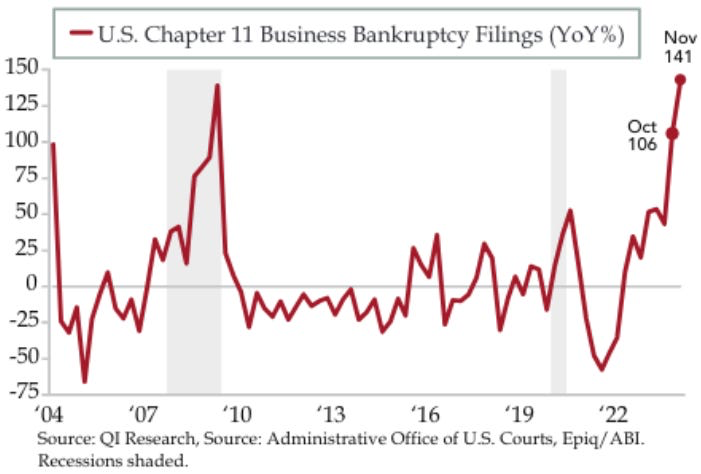

Bloomberg

- 3. Initial claims for unemployment have been trending down in recent weeks. That’s a definite positive for the economy. However, the trend in business bankruptcy filings calls into question the accuracy of the initial claims data. It could be a function of “labor hoarding” after the severe challenges of hiring and retaining employees in the wake of the pandemic. This may be why hours worked have been coming down and continuing claims for unemployment insurance are still rising. Moreover, despite nearly universal soft-landing expectations, U.S. bankruptcy filings hit 642 last year, per S&P. This is the most elevated since 2010 when the economy was haltingly emerging from the Great Recession.

Booth/Quill…

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240120