Haymaker Friday Edition

Haymaker Friday Edition

Top Ten Potential Surprises of 2024

Charts of the Week

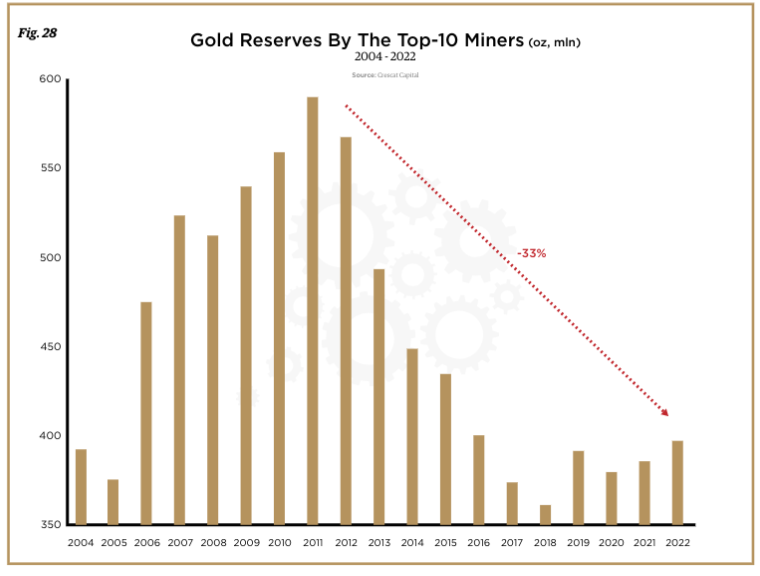

Unlike U.S oil and gas producers that have, as a result of the shale miracle, been able to dramatically increase their reserves and output, the situation for the leading gold miners is very different. The many years of challenged profitability and related capital spending starvation has created a situation where reserves in the ground are now off by 1/3 since 2011.

Williams, TTMYGH

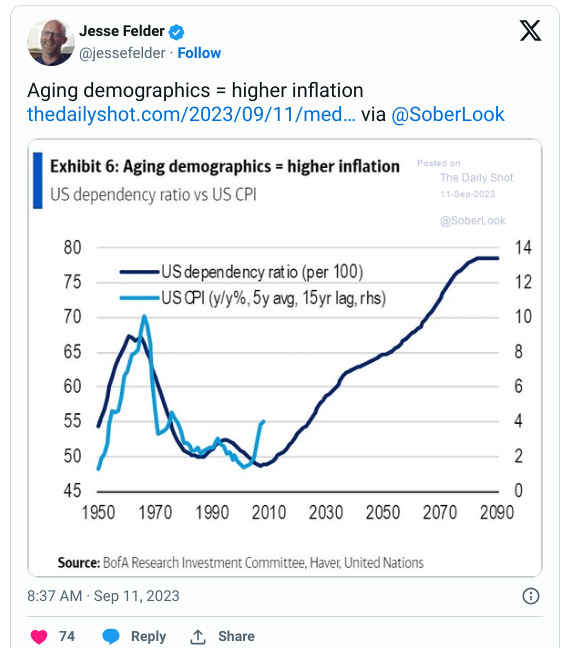

Among the many reasons to suspect that the recent inflation cool-down is transitory is due to demographics. As 19th century French philosopher Auguste Comte long ago observed, demographics are destiny. Based on that aspect alone, it’s best to be suspicious that the CPI will hover around the Fed’s desired target of 2%. As my friend Jesse Felder X’d out (Tweeted sounds so much better; thanks, Elon!), there is a tight correlation between the dependency ratio and consumer prices. Because that ratio compares workers to the size of the overall population, that makes sense. Fewer productive workers and more who are merely consuming should exert upward pressure on prices.

Felder

Evergreen Compatibility Survey

“In a time of domestic crisis, men of goodwill and generosity should be able to unite regardless of party or politics.” -John F. Kennedy

“The future ain’t what it used to be.” -Yogi Berra

“Even Napoleon had his Watergate.” -Also Yogi Berra

Top Ten Potential Surprises of 2024

It’s homage time, in this case to the legendary Byron Wien who passed away at 90 this past October. Byron was famous for his Ten Surprises for a given year. Because these were, by definition, non-consensus expectations, the odds were against them being actualized. Based on that, he did make some excellent “calls of the unexpected” over the years.

For example, in his last list of surprises, for 2023, he postulated that the S&P would bottom in mid-year. He was bit off because the S&P bottomed in March but it was still a good prediction. He also anticipated a “financial accident”; last spring’s banking crisis checked that box. Further, he pretty much nailed it with his expectation that the Fed would stay hawkish, more so than other central banks.

Of course, when it comes to divining the future — especially, sticking to outside-the-box calls — there are going to be a few whiffs. One of his worst was that he thought Elon Musk would turn Twitter/X around during 2023. Another was that oil would fall as low as $50, though that wasn’t a terrible miss. Crude briefly traded in the low 60s before screaming to $95 by late September. (After that, it was another precipitous tumble to the upper 60s, leading to the latest oversold rally.)

Another less than stellar anticipation is that China’s growth would re-accelerate, leading to a broad commodity rally. In reality, it was pretty much the opposite outcome. He also thought that unrelenting carnage on both sides in Ukraine would lead to a truce. Hopefully, that one isn’t wrong, just a tad early.

Accordingly, in the spirit of Byron Wien I am initiating an attempt at my own surprises. As you can see, I’m providing more color on these lower-probability events than he did… but, then again, I certainly don’t have his track record or gravitas. Admittedly, my concluding shocker could reasonably be called a triumph of hope over experience. However, for the future of America, and the world, let’s hope it’s not.

David “The Haymaker” Hay…

Subscribe to Haymaker to read the rest.

Become a paying subscriber of Haymaker to get access to this post and other subscriber-only content.

A subscription gets you:

| Subscriber-only posts and full archive | |

| Post comments and join the community |

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

20240106