Growth Over Cyclicals? Not So Fast.

This week has no shortage of potential catalysts. We have over 30% of the S&P 500 members reporting earnings this week, including four of the FAANG stocks. The Fed meeting on Wednesday, updated GDP numbers, the uncertain coronavirus situation and even Robinhood’s IPO all have the potential to move markets this week.

I’ve often told investors you should have three goals: identify trends, follow those trends, and anticipate when those trends are exhausted. In periods of uncertainty, stick with the trends. Clearly define your risk and your reward, and regardless of the overall market direction you should be able to safely navigate the markets.

How does all of this relate to sector rotation?

Quite simply, sector rotation represents the cyclical nature of the financial markets, as sectors and themes and styles come in and out of favor. Late 2020 and early 2021 were all about the emergence of the cyclicals. Financials, energy, materials and industrial stocks all pushed higher as the FAANG stocks struggled to keep up on a relative basis.

Then something changed in April to May of this year. The upside run in cyclical sectors began to show signs of fatigue, and growth sectors like technology and communication services emerged to retake the leadership role. So while the S&P 500 has consistently made new all-time highs every month in 2021, the stocks that pushed the market to new highs have changed.

So where are we now?

Four of the FAANG stocks, AAPL, MSFT, GOOGL and FB, all reported earnings this week with limited upside follow-through. Granted, most of these names were bid up quite strongly leading into this week, but they’ve seen limited upside follow-through since their earnings releases.

Breadth measures and now even momentum indicators have flashed bearish divergences, suggesting an elevated risk of a correction in the coming weeks. There have been some signs of life in financial and energy stocks, but not enough to propel stocks like JPM out of recent congestion ranges.

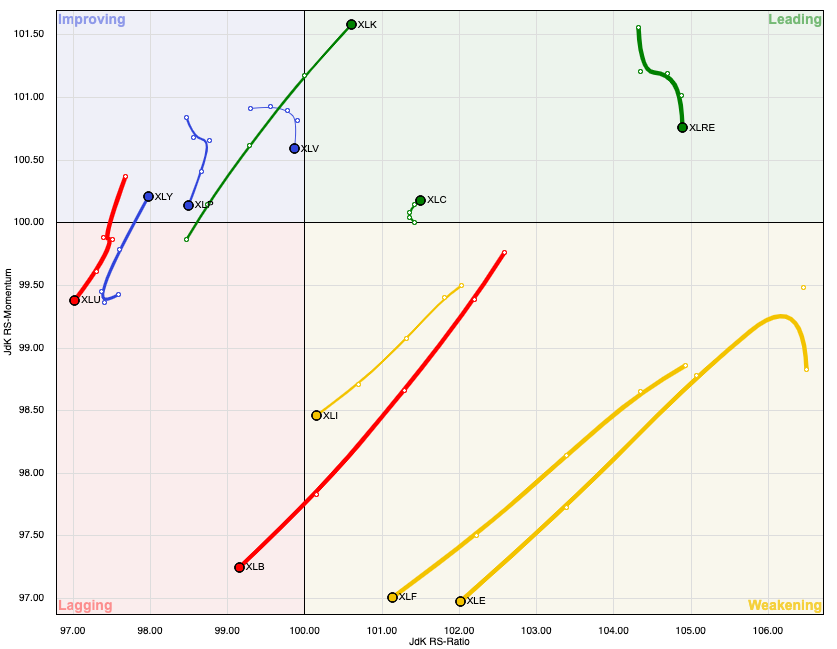

At the end of the day, it’s all about leaning into what’s working and leaning away from what’s not working. I often use the Relative Rotation Graphs (RRG) to visualize how the eleven S&P 500 sectors are rotating through periods of strength and weakness.

In a recent video, I discussed how to identify opportunities for outperformance and highlighted three particular sectors: Technology, Industrials, and Real Estate.

- * How can we define the rotation away from cyclical sectors over the last 6-8 weeks?

- * Why are growth-oriented sectors well-positioned given recent relative strength?

- * Which sector led the markets in the bull phase of 2014, and is also strong today?

For deeper dives into market awareness, investor psychology and routines, check out my YouTube channel!

RR#6,

Dave

PS- Ready to upgrade your investment process? Check out my free course on behavioral investing!

David Keller, CMT

Chief Market Strategist

https://www.StockCharts.com

David Keller, CMT is Chief Market Strategist at StockCharts.com, where he helps investors minimize behavioral biases through technical analysis. He is also President and Chief Strategist at Sierra Alpha Research LLC, a boutique investment research firm focused on managing risk through market awareness. He is a Past President of the Chartered Market Technician (CMT) Association and currently serves on the CMT Curriculum and Test Committee. David was formerly a Managing Director of Research at Fidelity Investments in Boston as well as a technical analysis specialist for Bloomberg in New York. You can follow his thinking at MarketMisbehavior.com, where he explores the relationship between behavioral psychology and the financial markets.

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.