What to Expect from the Fed this Week

What to Expect from the Fed this Week

This is the time when the two competing narratives over the Fed’s path of rates get to test each other. STIR markets have been pricing in two rate cuts this year. However, the Fed’s communication has been that there needs to be more work done on inflation and the Fed has been reluctant to start talking about rate cuts. The December summary of economic projections saw no rate cuts projected at all this year. So, there we have the conflict. The Fed sees no rate cuts this year and STIR markets see two. So, which way will the Fed edge in its communication? Will it push back against STIR markets projections and stress no rate cuts? Alternatively, will it move away from its December projections and start talking about pausing rates/cutting on growth concerns?

What to watch for

A clear hawkish sign that the Fed is concerned about inflation would be if the messaging starts to move towards a terminal rate above 5.5%. This would be a hawkish development and should trigger more USD upside. The simplest expression of this would be EURUSD downside. Please note there is no dot plot at this meeting.

A clear dovish message from the Fed would be the worries about slowing growth/hints of a rate pause or a rate cut coming. Any of these factors, or preferably a combination of them, should be dovish for the USD and should support XAUUSD and XAGUSD higher. It should also support US stocks higher if the Fed takes a more dovish stance. The S&P500 is up-testing a key weekly trendline and this level can be used as a good reference point.

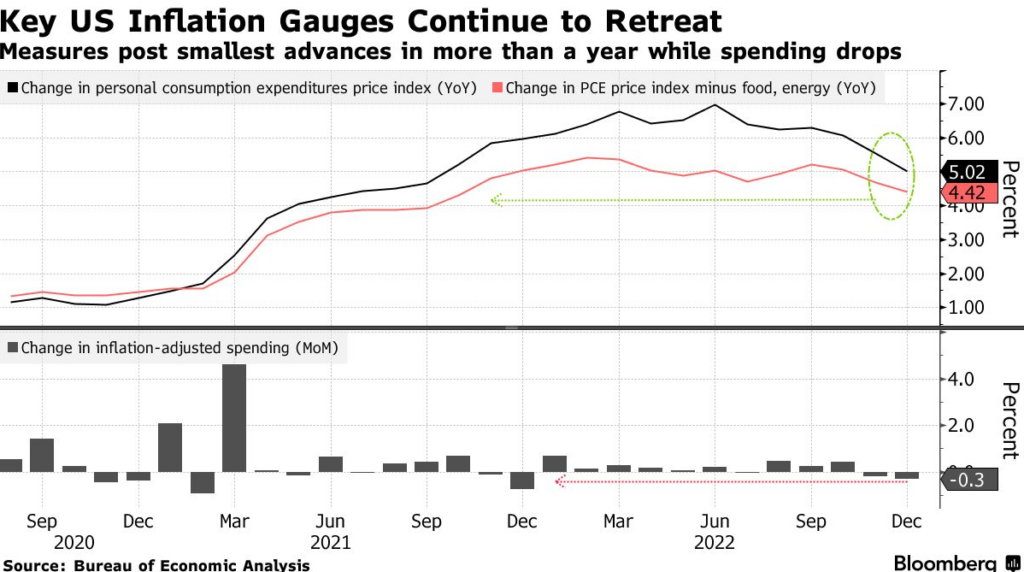

In favour of this view is the fact that expectations have been growing for a more dovish Fed as inflation readings fall. The Fed’s preferred measure of inflation, the personal consumption expenditures core price index rose at the slowest pace since late 2021 to 4.4% y/y. The headline price rose to 5%, lower than the 5.1% projected and the m/m reading was a rise of 0.1%.

Although still well above the Fed’s preferred 2% target it does show that the worst of the inflation prints are in the rear mirror, at least for now. Also, watch out for US labour data due out on Friday. Any signs of a serious slowdown in the labour market will play into the need for a dovish Fed. Keep that in mind as a tail risk post the Fed meeting on Wednesday.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

20230131