What the ECB’s last holding meeting means?

This was a holding meeting with a slightly more optimistic tilt. ECB President Lagarde said the decision could be seen as a ‘steady hand’ decision. The statement was virtually the same as the prior one, so it is a fair description.

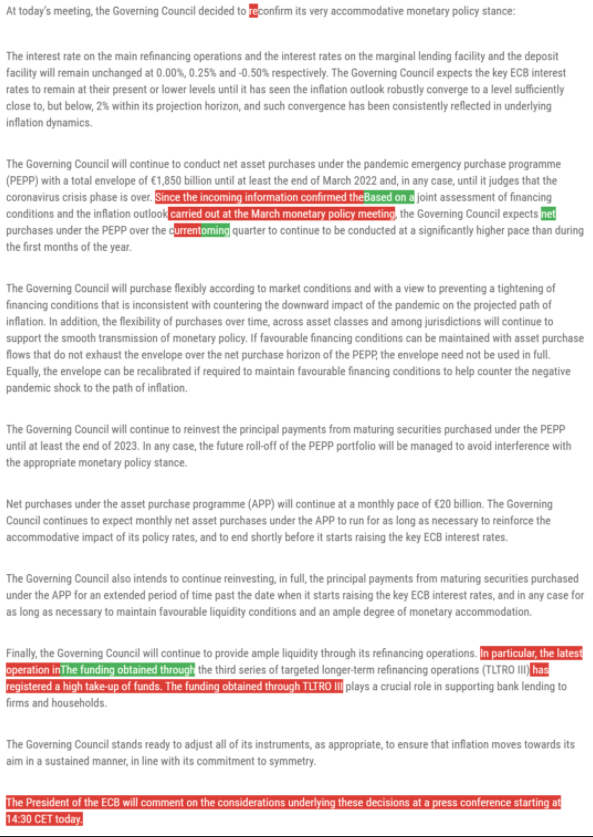

The main points first

- * The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility were unchanged at 0.00%, 0.25% and -0.50%.

- * The Governing Council will continue to conduct net asset purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,850 billion until at least the end of March 2022.

- * If favourable financing conditions can be maintained with asset purchase flows that do not exhaust the envelope over the net purchase horizon of the PEPP, the envelope need not be used in full. Equally, the envelope can be recalibrated if required.

- * Net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion.

So, that was pretty much what was expected going into the meeting as the recent ECB rhetoric had shown a more dovish tilt. Remember it was just a few weeks ago when this June meeting was being touted as the one to begin tapering. However, there were some more bullish points in the detail.

The optimistic notes

1. Christine Lagarde said that growth risks are now seen as ‘broadly balanced’ while the ECB had previously said that they were ‘tilted to the downside’.

2. GDP projections are revised higher and the ECB expect activity to accelerate in H2 2021.

- * 2021 to 4.6% vs 4.0% previously

- * 2022 to 4.7% vs 4.1% previously

- * 2023 at 2.1% vs 2.1% previously

3. Inflation projections were revised higher:

- * 2021 to 1.9% vs 1.5% previously

- * 2022 to 1.5% vs 1.2% previously

- * 2023 to 1.4% vs 1.4% previously

4. From an ECB sources report after Lagarde’s press conference, three policymakers wanted to cut PEPP purchases at the last meeting.

The takeaway

This was a steady hand with an eye to the future and does tilt the ECB to bond tapering at their next meeting. The EURUSD pair was barely moved out of the meeting and the German bunds kept finding buyers (pushing yields lower), but that was the case across the bond market last Thursday. So, very much a holding meeting and there is not much tradable immediately from it aside from knowing what the ECB’s thinking is so that a shift can be spotted.

Giles Coghlan