U.S. Cannabis in the Crosshairs

U.S. Cannabis in the Crosshairs

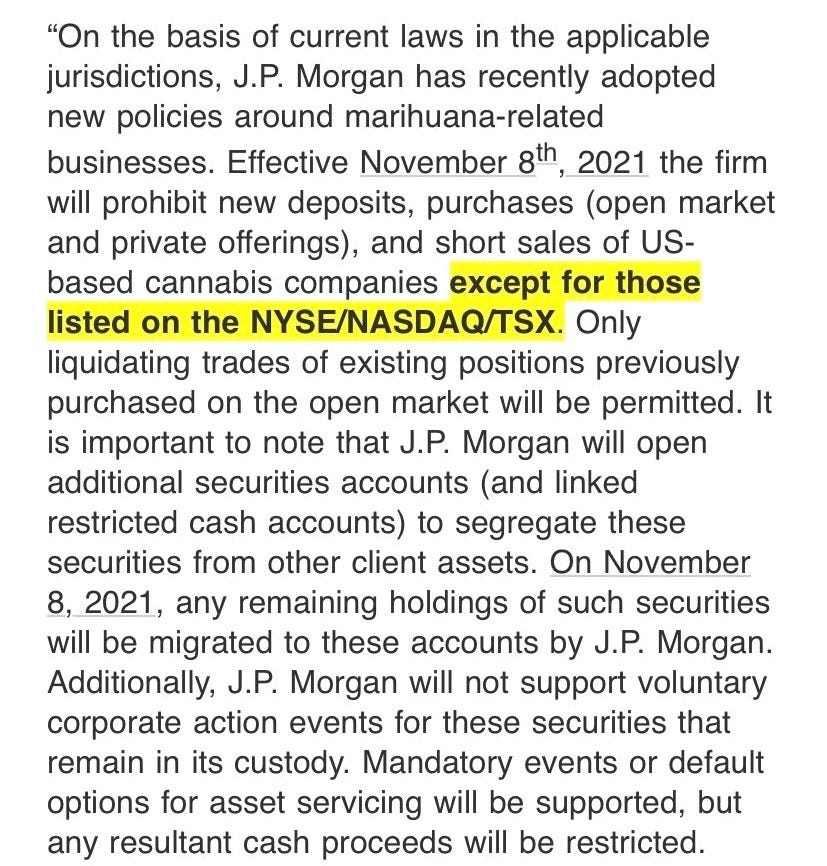

There’s a lot of noise in U.S cannabis of late, including the recent speculation that JP Morgan will join a growing list of banks that no longer custody US cannabis stocks.

I haven’t verified if the below text is accurate but did confirm that their policy will become more restrictive November 8th.

[none of this would surprise me as it might help to explain the recent price action / massive volume / prints]

Industry veterans will remember a similar situation two years ago when Pershing pulled the plug on US cannabis custody and clearing.

At the time, US canna was on the ropes after a brutal two year bear market, the cost of capital was borderline usury and there were existential risks for the industry.

This JPM stuff, if true, isn’t that, for several reasons:

- Pershing cleared canna for most of the funds that were involved in the space, whereas JP Morgan, while massive, is / was a bit player in U.S canna.

- There are other custody / clearing solutions in place for those looking, although it’s entirely possible that some funds would punt their US canna exposure and take what may be the only tax-losses in the entire financial universe.

- The fundamentals are night and day. U.S cannabis leaders are cashed up and generating FCF despite all the onerous regulations, and the credit curve has contracted > 400 bps over the last year.

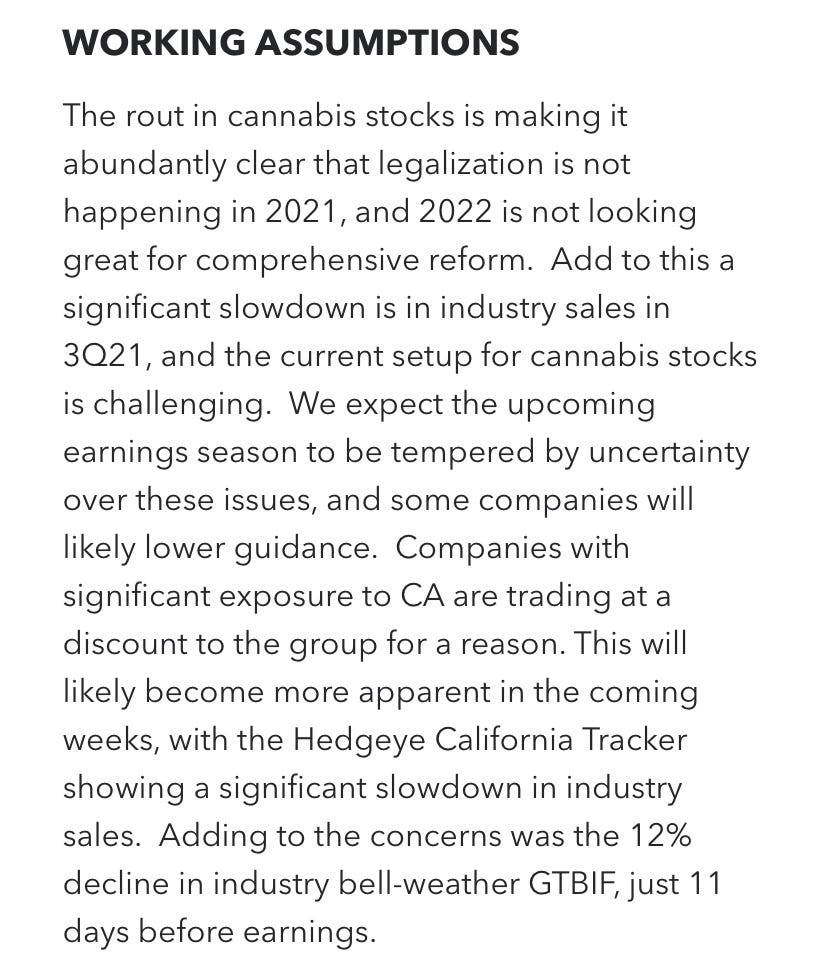

And while there may be cause for pause, per this note from Hedgeye Cannabis…

…markets look forward, not back. Nine months ago, there wasn’t a cloud in the sky or a reason to sell U.S cannabis. The market saw through, and after the massiveyear-over-year rally in the space—700-1250% gains—we’ve since given back half, or more.

It’s hard to game invisible catalysts (JPM) and even tougher to time the stock market but we wanted to share the other side as we ready for canna earnings the next few wks.

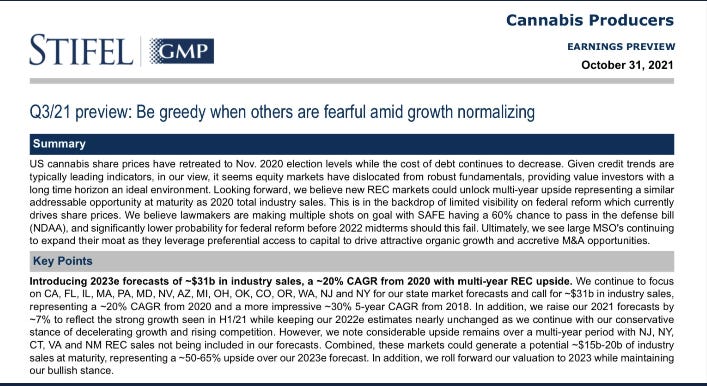

First, this note from The Greek Freak Andrew Partheniou at Stifel, where he talks on the stellar industry fundamentals, the long multiyear tail and his take that SAFE has a 60% shot of passing this year via the NDAA

…and there’s this from Matt “Shooter” McGinley from Needham…

The Here and Now

It’s been a wild few years for cannabis stocks: the massive 1.0 (Canadian cultivation) bubble and bust that erased 92% of the value of global cannabis bw 1/18-3/20; the rise of cannabis 2.0 (US led CPG; cannabis as an ingredient) that sparked massive gains for cannabis stocks from 3/20-2/21; and the five-finger Sally we’ve seen endured.

I’ll reiterate something I said about a year ago, when many U.S cannabis stock prices were last at these levels: the best case under McConnell will be the worst case under Schumer, and that’s SAFE Banking.

And despite the noise / seething anger / venom that now surrounds the space, I still believe that the script is the script is the script and view these levels akin to a second bite at the apple, one that should be embraced rather than dismissed.

But hey, NEWSFLASH: we’re super-bullish on U.S cannabis / have built businesses that are predicated on the success of this economic-driver / jobs-engine; and given where one stands is a function of where one sits, none of this should be a surprise.

So when we share that we’re buying U.S cannabis because it’s trading at ridiculously cheap multiples entirely predicated on continued state-level adoption—and that we view anything at the Federal level as an upside call option to our thesis—we share that in good faith bc it’s true.

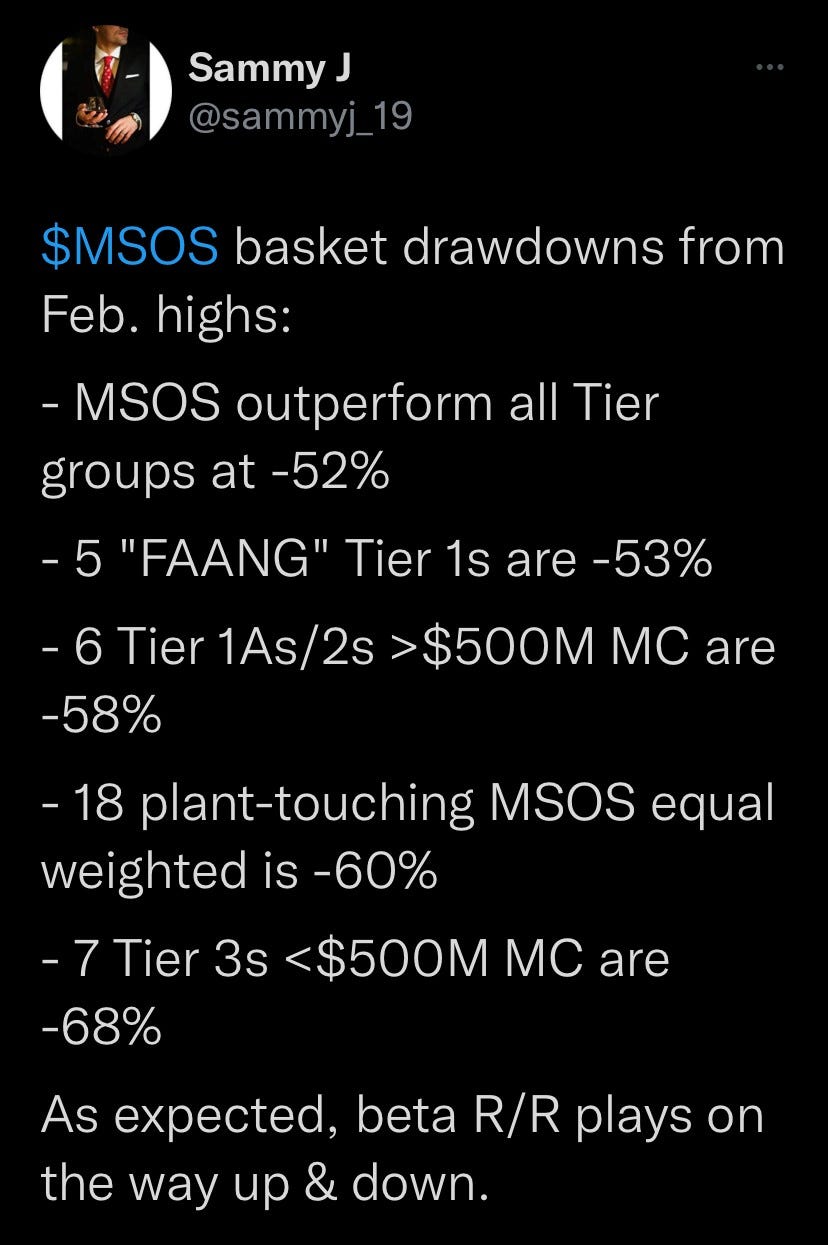

h/t @cashflow_free; click to enlarge

Doesn’t mean we’ll be right, of course, but I like our odds…

…and I also like seeing smart money entering U.S canna into this downdraft…

…because birds of a feather often flock together.

Good luck, and may peace be with you.

/positions in stocks mentioned.

position / advisor US Cannabis ETF $MSOS

20211101