Transitory inflation? “Think again”, say ING.

Last week there was an article on ING making a case for inflation being more broad-based than the latest CPI figures indicated. This is an interesting case since UC CPI seems to have peaked. The latest readings were 0.5% m/m increase in July, in line with expectations, but the core (ex-food and energy) index was a slight miss at 0.3% m/m versus the 0.4% consensus. The core annual rate of headline inflation is at 4.3% versus 4.5% for last month’s reading. So, inflation is fading, right? ING say inflation is actually broadening. Here is their case:

1. The reason for the softer readings was that airline fares, used car prices, and clothing all fell in price.

However, recreation showed a sharp move higher (0.6% m/m), medical care posted its fastest increase since February (0.3%) and housing costs increased (0.4% m/m).

2. Inflation may have peaked, but disinflation will be slow.

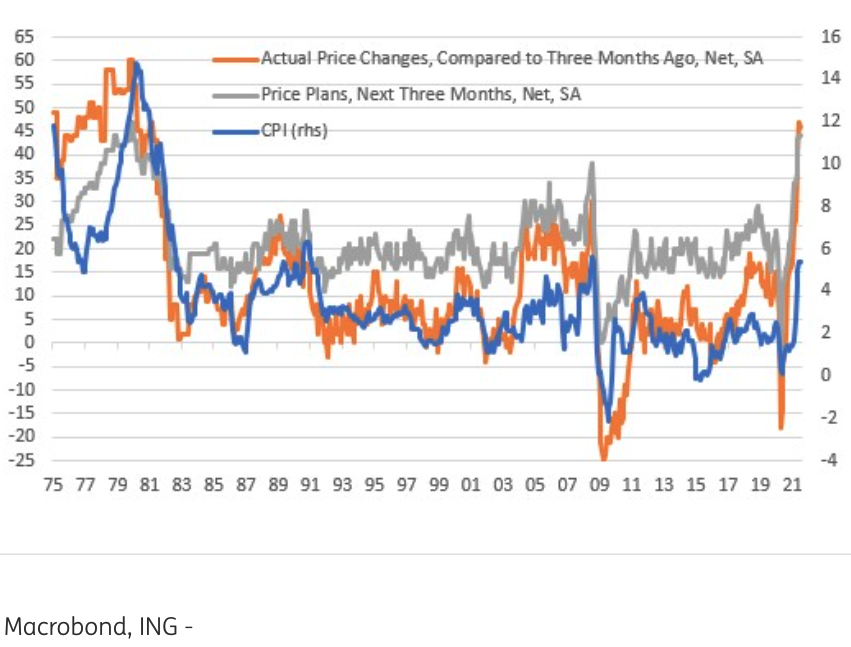

Their thinking here is that the stimulus fuelled economy is booming and demand is outpacing the supply capacity of the economy due to bottlenecks and about shortages. As a consequence, costs are increasing throughout the economy and companies have confidence in using pricing power now. In fact, the National Federation of Independent Businesses (NFIB) companies raising prices are at a 40 year high as the chart below tells us.

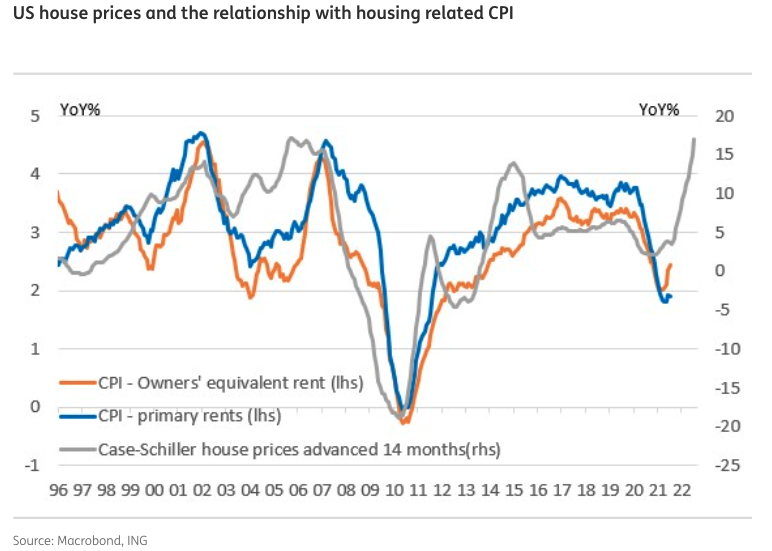

3. Housing costs are rising.

ING say ‘Primary rents and owners’ equivalent rent account for a third of the CPI basket with movements in these components tending to lag 12-18 months below house price changes’. They see this being the story to watch for the second half of the year and look for housing costs alone to add 1% to annual inflation.

4. They question the Fed’s statement that longer-term inflation remains anchored at 2%.

This is because they are projecting the strong growth story to remain in the US and workers to be in short supply, keeping headline inflation above 4% through Q1 for 2022. A light irony here too is that inflation expectations even from the NY’s own Fed have risen. They project 3y ahead inflation to be above 3.5%. So, it looks like we may see a shift from the Fed at some point on just how well-anchored inflation expectations are.

The bottom line

Well, this means that there is a stronger case for Fed tapering being announced at the Jackson Hole Symposium. This look under the hood at inflation by ING is compelling. The spike higher is not just due to used cars (who would have thought?) and does seem broader than perhaps it may seem by just looking at the headline. So, prospects of a Fed taper announcement at the Jackson Hole Symposium keep a USDJPY buy on dips bias. However, the recent hit to consumer confidence on Friday means that narrative may be questioned going forward. So, watch out for any Fed speakers to make the narrative clear.

Giles Coghlan