The Hard Decision Facing Central Banks

The Hard Decision Facing Central Banks

Next week the Federal Reserve, Bank of England, and Swiss National Bank all meet. This time last week the SVB crisis was just dropping onto markets and since that time the decision for central banks has just got a lot harder. The fallout from the Credit Suisse crisis on Wednesday just underscored the difficulty for central banks. Do they hold back on hiking interest rates due to strains in the economy? Or do they keep hiking so inflation doesn’t get out of control?

Invariably in markets, someone always thinks a central bank has ‘got it wrong’. In an ideal world, with hindsight, all decisions can be made with 20/20 vision. It’s easy looking backwards to know what decision you should have made. However, in reality, it is usually more down to luck than skill when the timing is perfect in these decisions. That does not take away from the difficulty of their decision though and here are some of the factors influencing them.

The lag effect

Are the SVB crisis and Credit Suisse the first signs of economic activity being crushed? The answer is, ‘yes’. So, the next question is how many more banks will be affected. If the Fed hikes rates by 50bps next week will there be more banks under strain. Will investors start moving deposits from ‘riskier’ banks? The risk of contagion is real and when it happens, it happens very quickly.

The inflation fight

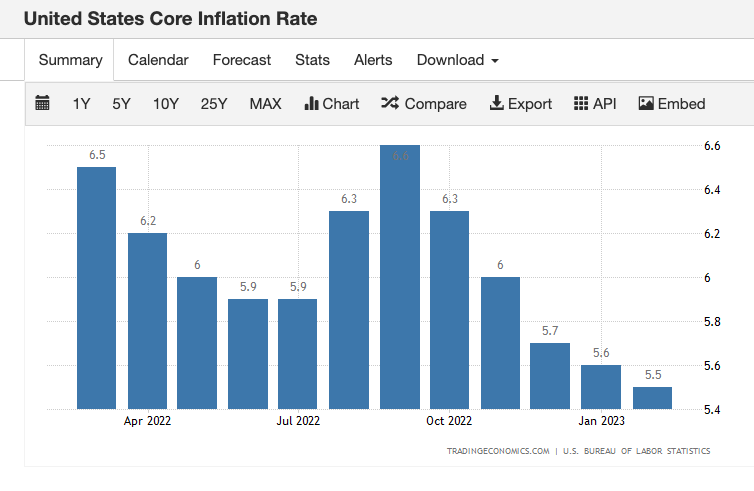

It’s not over. So, with the Fed backing up the SVB and the SNB supporting Credit Suisse will this type of ‘propping up’ keep global inflation pressures rising? If it doesn’t hike rates, will the core inflation rates around the world just keep rising? Core rates have been generally quite stubborn around the world. The US core was 5.5% for February.

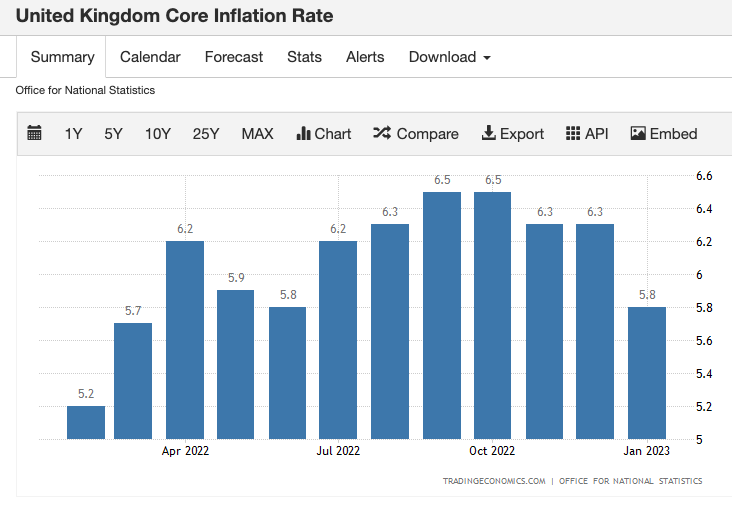

The UK’s core inflation was 5.8% for January.

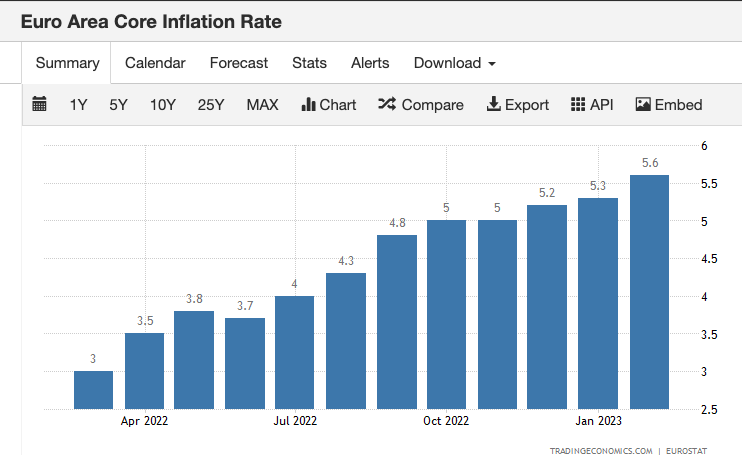

The Eurozone’s core inflation was 5.6% for February and is still trending higher.

So, the risk is that core inflation becomes entrenched if the central banks take their foot off the gas too quickly in terms of raising rates. However, what is ‘too fast’? The drop in the labour market numbers post-covid has kept wages firmer, so price pressures are still ‘in the system’.

The importance of next week

The pressures on central banks underscore the importance of next week and also the next moves for markets. After huge amounts of rate re-pricing over the last 7 days, one thing is for sure – expect volatility next week over the Fed’s meeting. Watch stocks and precious metals closely as some near-term trends could be set depending on how aggressive or otherwise central banks decide to be.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

20230317