SNB Takes On a New Role as Inflation Buster

SNB Takes On a New Role as Inflation Buster

This was a shock decision. For years the SNB has been battling against deflation and trying to keep the CHF from strengthening. Do you remember the attempt of the SNB to keep the EURCHF pegged at 1.2000 and its eventual capitulation in 2015? Well, the SNB is now in the position of actually wanting to strengthen the Franc in a bid to tackle inflation. This is how the decision last Thursday went and what it means more widely.

50 bps hike

No economists going into the SNB meeting expected the SNB to move on rates. This was because no one thought the SNB would hike rates before the ECB did. However, the central bank announced on June 16 that, ‘the SNB is tightening its monetary policy and is raising the SNB policy rate and the interest rate on sight deposits at the SNB by half a percentage point to −0.25% to counter increased inflationary pressure’. This hike is all about one thing, fighting inflation.

Inflation buster: fearing spreading inflation

The SNB attributed the inflation to the conflict in Ukraine driving up prices for commodities which compounded already persisting supply bottlenecks. So, why did it hike rates as both of these factors are out of the SNB’s control? The answer is to combat spreading inflation. The second line of the SNB’s statement stated, ‘the tighter monetary policy is aimed at preventing inflation from spreading more broadly to goods and services in Switzerland’. Linked to this is the idea that the Swiss, like the RBA and the BoE, and the Fed, do not want to see a ‘wage-price’ spiral.

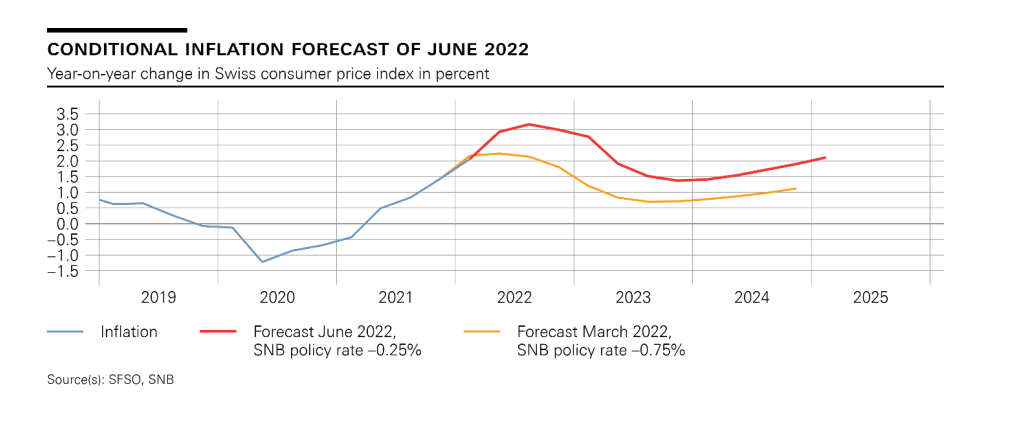

The SNB revised its inflation forecast higher, but still sees it dropping around the middle of next year.

The takeaway

The move by the SNB before the ECB is a significant shift. We no longer have the reference to the CHF being ‘highly valued’ and the need for FX intervention to address it. According to the excellent team over at ING, with a piece authored by Charlotte de Montpellier, Chris Turner, and Antoine Bouvet: ‘We take this to mean that the SNB will now sell EUR/CHF to ensure that the trade-weighted CHF appreciates by roughly 4% per annum. Why do we say 4%? This is because the SNB told us in late April it wants to keep the real CHF stable and a 4% nominal appreciation in the trade-weighted CHF is required to offset the low inflation in Switzerland relative to trading partners.’

Inflation tackler

All of this means the SNB is tackling inflation on the front foot and they don’t want inflation to go into wages. With inflation at 2.9% in May the SNB is trying to slow that down as quickly as possible. This does open up a USDCHF sell bias for now. If the US starts to show falling inflation then USDCHF could move sharply lower. So, one to watch with key levels marked.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

20220621