September Central Bank Overview

September Central Bank Overview

Major central bank rundown

It has been a very busy week with the SNB, BoE, BoJ and the Fed all meeting this week. So this weekend is a great time for a catch-up on the largest central bank moves. The central banks are listed below with their current state of play. The link for each central bank is included in the title of the bank and the next scheduled meeting is in the title too. The link to the latest statement is at the bottom of each section, so there is no excuse for not being up to date.

Reserve Bank of Australia, Governor Phillip Lowe, 0.10%, Meets 05 October

Sticking to the recovery script

Despite the surge in the delta variant Governor Lowe said on September 10 that the economic recovery had been delayed, but not derailed. However, he did add that it was difficult to understand markets pricing in hikes in 2022 and 2023 and said that interest rates were unlikely to rise before 2024.

The delay in the economic recovery was reflected in the last meeting

On September 10 the RBA surprisingly kept to their plan to taper (reduce) purchases to $4 billion a week. However, the time that tapering was to continue was extended out to mid-Feb 2022. So, the effect of this is that there will be more tapering for longer. The RBA repeated that their experience is that, once the virus is contained, the economy bounces back quickly. The question, of course, is whether it can be contained or not as cases are still rising. The RBA conceded that they expect the bounce back to be slower than earlier in the year, so the expectations seem reasonably set from the RBA.

AUD: Watch for mean reversion

The AUD has seen shorts building and they are now looking very stretched. The obvious trade to look for here is some mean reversion. It is very easy to not expect mean reversion when you are trading, especially when there are multiple reasons for AUD weakness, but it happens more often than you may realise. Therefore, in particular look for any bullish signals for the AUD to send it higher quickly. The main trigger would be either a sharp decline in COVID-19 cases and or some recovery from China. The latest slow down from China’s economy and sharp falls in the Iron ore markets have been weighing heavily on the AUD.

The takeaway

Central bank divergence between the RBA and the RBNZ. Although this divergence looks set for some mean reversion now, a deeper pullback should still find sellers as long as the broad outlooks stay unchanged.

You can read the full statement here.

European Central Bank, President Christine Lagarde, -0.50%, Meets October 28

Holding meeting, despite policy change

The meeting on September 09 kept interest rates unchanged. The size of the bond purchases (PEPP) was unchanged at €1.85 trillion and APP purchases are continuing at the speed of €20 billion a month. However, the pace of the PEPP bond purchases has changed. The Governing Council decided that the pace of asset purchases under the PEPP programme could be slightly reduced. The PEPP purchases are now to be conducted at a ‘moderately lower pace’ versus the previous decision of a ‘significantly higher pace’.

Does this mean the ECB is tapering?

No. In the press conference, it was clarified that the tweak to the PEPP purchases is not considered ‘tapering’ by the ECB. However, to a certain extent, this is semantics as the ECB are recognising that less support is needed. The ECB are wanting to simply avoid overkill with too many APP purchases and not signal a material shift in policy outlook. Further PEPP discussion will take place in December. There was little new here at the meeting and the ECB is remaining on a ‘wait and see’ stance. Moving forward the focus remains on incoming data and the December meeting.

What comes after the PEPP programme expires in 2022?

If you cast your mind back to the July 23 meeting there were expectations that, after the ECB’s strategic review, the ECB would be revealing a more dovish hand. This was hinted at in the run-up to that last meeting by Christine Lagarde who said that the PEPP could ‘change’ into something else. Well, at this latest meeting they did not discuss what would come next after the PEPP programme ends. So, this is at least on hold for now, but Lagarde has recently reminded markets that the eurozone is ‘not out of the woods yet’.

The takeaway

Optimistic, but with a holding stance. Lagarde summarised that the eurozone economy rebounded by 2.2% in Q3 and is on track for strong growth in Q3. Consumer spending is increasing, but there are still 2 million fewer people employed than before the pandemic. So, there is nothing tradeable here for now. Just accept the euro has a weak bearish outlook. However, incoming data remains key as does the voice of the ECB board members. In particular, look out for any hawkish comments from Lagarde, de Guindos, and Lane to boost the euro for a quick sentiment-based trade intraday. Aside from that, you would favour EURUSD downside after the Fed’s latest shift this week.

You can read the full statement here.

Christine Lagarde’s press conference link here.

Bank of Canada, Governor Tiff Macklem, 0.25%, Meets October 27

At the last meeting, the BoC held rates at 0.25%. Asset purchases remained at $2 bln and they see lifting rates around the second half of 2022. There were far more concerns sounding from the BoC at their last meeting than there had been at the start of the year. The bank stressed the problem of supply chain disruptions, slack in low-wage workers, and the uncertainty of supply chain bottlenecks. However, the BoC still see the economy strengthening in the second half of 2021 with consumption, business investing, and government spending all contributing positively to growth.

Inflation

Like the Fed, the BoC see it as transitory. The BoC gave a caveat to this by once again saying that ‘the factors pushing up inflation are transitory, but their persistence and magnitude are uncertain and will be monitored closely’. So, higher inflation is not going to be totally ignored.

COVID-19

The BoC ‘continue to expect the economy to strengthen in the second half of 2021, although the fourth wave of COVID-19 infections and ongoing supply bottlenecks could weigh on the recovery’.

The takeaway

Nothing much to note here aside from the fact that CAD should remain supported against weaker currencies. Any deeper dips lower on Evergrande fears/collapse should offer good value in the near term on CADJPY.

You can read the full statement here.

Remember stronger oil supports the CAD as around 17% of all Canadian exports are oil-related. Canada’s top export is Crude Petroleum at over $66 billion and around 15.5% of Canada’s total exports.

Federal Reserve, Chair: Jerome Powell, 0.125%. Meets 03 November

Sufficient progress on inflation and employment ‘all but met’

At the latest Fed meeting, interest rates were unchanged and the path of QE stayed at $120 bln per month. The statement revealed that ‘if progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted’. This sets up a November taper.

Powell went further in the presser

The Fed delivered a surprise in the press conference as Jerome Powell said that, if the economy remains on track, then the tapering of asset purchases could be concluded by the middle of next year. This was towards the hawkish end of expectations and Jerome Powell said there was broad support on the committee for the timing and the pace of the taper.

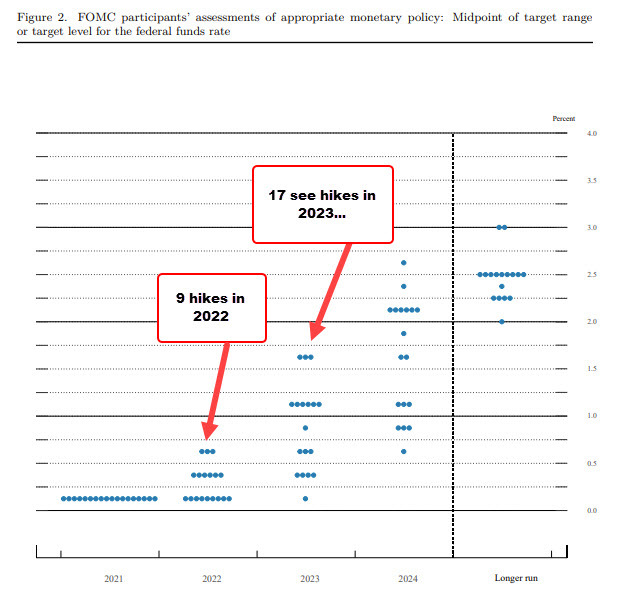

The dot plot

Here is a helpful post on this straight after the meeting.

The dot plot for the September 2021 FOMC meeting shows:

- 0 Fed officials see hikes in 2021 vs zero in the June meeting,

- 9 Fed officials see hikes and 2022 vs 7 in the June meeting,

- 17 Fed officials see hikes in at 2023 vs 13 in the June meeting.

The bottom line

The Fed has now set up a November taper and plans to have tapering completed by the middle of 2022. The next jobs report is going to be very important on October 08. A good jobs print and expect the USD to surge in anticipation of a November taper. However, one note of caution is that the USD has been pretty flat after this latest meeting when otherwise it would have been reasonable to expect more USD strength. So, just bear that in mind. However, a strong jobs print should be ok for at least an intraday pop higher in the USD if not more. Keep an eye on US 10 year yields if you look to go long USDJPY. You want to see US10 year yields moving higher to confirm the USDJPY upside bias.

Bank of England, Governor Andrew Bailey, 0.10%, Meets November 04

There was no change to interest rates and the split was 7-2 in favour of not altering the current target of £875 billion in bond purchases. Saunders and Ramsden were the dissenters as would be pretty much expected from their more hawkish stances. During the August BoE meeting, the bank was optimistic without prompting an initial hawkish response from markets. In this latest September meeting, the Bank of England was able to prompt a hawkish response. Take a look at the drop lower in Sonia futures as markets price in higher interest rates coming.

Inflation is now a worry for the BoE.

They did not say as much, but the inference is clear. First of all the 3.1% print in August was marked out as the highest since November 2011. The BoE also noted that ‘CPI inflation is expected to rise further in the near term, to slightly above 4% in 2021 Q4, owing largely to developments in energy and goods prices’. The phrase that caught my attention was this one – ‘The MPC’s remit is clear that the inflation target applies at all times’. All times. So, now. This inflation worry translated to the Bank saying that ‘some modest tightening of monetary policy over the forecast period was likely to be necessary to be consistent with meeting the inflation target sustainably in the medium term. Some developments during the intervening period appear to have strengthened that case’.

The end of the furlough scheme is still a concern for the BoE. The BoE is focusing on ‘the extent, impact, and duration of any change in unemployment; as well as the degree and persistence of any difficulties in matching available jobs with workers’. So this means that jobs data will be in key focus going forward for the GBP.

Bottom line

The medium-term outlook for the GBP remains bullish. Pairing the GBP against the CHF and the JPY make sense, just watch that the risk tone does not result in significant strength for the safe-haven currencies.

The other entry option is from the market with a hidden bullish divergence on the weekly chart.

The argument against GBPJPY longs is that the Evergrande crisis can return to spook markets at any time and is not an insignificant risk. The other option would be to pair the GBP with the EUR as long as the ECB have a neutral/ weak bias.

You can read the full statement here.

Swiss National Bank, Chair: Thomas Jordan, -0.75%, Meets December 16

This is interesting as the SNB is showing signs of growing impatience with the strong CHF. The SNB interest rates remain the world’s lowest at-0.75%. This is due to the highly valued franc (CHF) which has seen significant gains over the last few years due to safe-haven demand.

The SNB want a lower CHF

At their latest meeting, they repeated their willingness to intervene in the FX market in order to counter upward pressure on the Swiss franc. However, at this last meeting, the SNB were explicit about the highly valued franc. Previously, they had said that they were willing to intervene ‘as necessary while taking the overall currency situation into consideration’. The shift underscores that the SNB hates a strong CHF and their patience is fractionally thinner. It’s probably been the Evergrande crisis spooking investors into the CHF that has peaked their attention. As an aside see here for an interview on the Evergrande crisis if you would like a refresher/primer. As an export-driven economy, they hate a strong CHF and are doing their best to make it as unattractive as possible. The market generally ignores this and keeps buying CHF on risk aversion which has been here in one form or another since around 2008/2009.

On their September 23 meeting, the SNB left rates unchanged. The inflation forecasts were revised higher again to 0.5% for 2021 from 0.4%.The new forecast stands at 0.4% for 2021, and 0.7% for 2022, but then back to 0.6% or 2023.

In terms of growth, the SNB was not as upbeat as the previous meeting. In the March meeting, they projected growth of 2.5% -3%. In the June meeting, they noted that the economic indicators had improved significantly of late. Growth for 2021 in June was seen at 3.5% mainly due to the lower than expected decline in GDP in Q1. The SNB now expects GDP growth of around only 3% for 2021. In June, the SNB had still been assuming higher growth. The downward revision, according to the SNB, is primarily attributable to the development of consumer-related industries such as the trade industry and hospitality which performed less dynamically than expected.

The bottom line and the EURCHF opportunity

The SNB will continue to intervene in the FX markets. The Swiss are always mindful of the EURCHF exchange rate because a strong CHF hurts the Swiss export economy. This is why there has been a shift in language about countering ‘upward pressure on the Swiss Franc’. The SNB want a weaker CHF. The rest of the world wants CHF as a place of safety in a crisis, so we have this constant tug of war going on.

For more details on the sight deposits check out SNBCHF.com. This site called the removal of the floor back in 2015, so well worth checking out.

The SNB are still content to be the lowest of the central bank pack and dissuade would-be investors by charging them for holding CHF. EURCHF for a 6-12 month hold is still worth considering, if not even more so now with the SNB’s patience wearing thin with a strong CHF.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, Meets Oct 27

The Bank of Japan still remains a very bearish bank and there is no sign of it exiting from its easy monetary policy. The latest meeting saw no surprises and everything was as expected. Interest rates remain at -0.10%. The Yield Curve Control (YCC) was maintained to target 10-year JGB yields at around 0.0%. The vote on YCC was made by 8-1 votes. The only dissenter was once again Mr Katoaka.

The general outlook is that although the level of Japan’s economic activity is ‘expected to be lower than that prior to the pandemic for the time being, the economy is likely to recover, with the impact of COVID-19 waning gradually, mainly due to progress with vaccinations, and supported by an increase in external demand, accommodative financial conditions, and the government’s economic measures’.

For years Japan has struggled to see any inflation, so with inflation rising around the world, it was interesting to see that the BoJ expect consumer inflation to remain around 0% for the time being.

The fed’s shift this week means USDJPY upside should be favoured.

In the last central bank report, I said that longer-term the Fed will move before the BoJ. The USDJPY pair has now broken higher after the Fed’s more hawkish shift this week. Check out the symmetrical pattern below. Also, check out the explanation of how the US 10 year yields tracks the USDJPY above under the Fed’s section.

If you need a hand trading this technical pattern, here is how to do it as outlined here. A return to test the pattern would be a great possible entry. Much focus will be on October 08 jobs, so stay tuned!

You can read the full statement here.

Reserve Bank of New Zealand, Governor Adrian Orr, 0.25%, Meets October 06

The latest RBNZ decision was a tricky one. Most of the projections for the decision were made obsolete by the news that the first case of COVID-19 had been discovered in Auckland. This sent New Zealand into a level 4 alert and three-day nationwide lockdown and Auckland into a seven-day lockdown. New Zealand has an elimination strategy to get rid of COVID which means any signs of cases rising will mean further lockdowns.

The RBNZ had to balance conflicting pressures. Firstly, the new COVID situation. Secondly, a very hot housing, employment, and inflation situation. At the meeting prior to this one the outlook for inflation was unclear. However, clarity emerged with the latest inflation reading coming in at 3.3% y/y which was the highest reading in 19 quarters. Also, remember that unemployment is very low at 4.0% vs the expected 4.5% level. So, the economy is running hot.

The RBNZ had to decide which pressure they would react to; Covid or a hot economy? They reacted to both. They responded to COVID pressures by not hiking rates and kept them unchanged at 0.25%. The RBNZ also reminded markets that they could decide to re-start the LSAP QE program (this stopped on July 23 this year) if necessary. The RBNZ said that the inflation and employment outlook would be reviewed on an ongoing basis with a view to raising interest rates over time. Both employment and housing are seen as ‘above maximum sustainable levels.

The bit that matters

Despite the hold on rates, this was seen as a minor hiccup on a strong projection higher. The projections for the cash rate were all revised higher from the previous meeting showing the underlying confidence that the RBNZ has. They project interest rates at 0.59% by December (previously it was 0.25%, 1.38% for September 2022 (previously 0.49%), & 1.62% in December 2022 (previously 0.67%).

The key point to note is that RBNZ is actually optimistic about the future and see the OCR rising. One rate hike this year and 100bps next. Not bad at all. Governor Orr really saw the recent COVID case as a bump in the road. Orr said at the meeting that lockdown is a concern but is less concerned than he would have been last year. The cherry on the top was when the Assistant Governor said that the bank would have hiked by 50 bps, but they avoiding doing it as it would make communication difficult as COVID cases were back again.

The takeaway

This should mean the NZD keeps an upside bias. A surprise rate hold and the first COVID-19 case in months could not send the NZD sharply lower. This means that the NZD remains a buy-on dip against weaker currencies. The RBNZ is expecting 100bps rise next year, so that should keep the dip buyers motivated. Something like the NZDJPY pair makes sense as long as the risk tone stays positive. Another alternative would be the EURNZD as a short depending on the ECB’s next move. The key issue here is how well the New Zealand Government can contain the virus.

20210928