Probing LCLoR

Probing LCLoR

Bank reserves are on track to approach a common estimate of the Lowest Comfortable Level of Reserves (“LCLoR”) within a few months. At the moment, reserves sit around $3.2t and a common Fed estimate places LCLoR at around $2.2t (8% of GDP). In addition to quantitative tightening, two events may soon reduce bank reserves to around $2.2t. First, the RRP is likely to steadily increase as MMF assets continue to rise and FHLB debt issuance declines. Second, the Treasury General Account’s eventual replenishment will likely be financed largely from reserves. The decline in reserves may only be temporary, as persistent bill issuance would eventually redirect liquidity out of the RRP and back into the banking system. This post reviews the mechanics behind the upcoming drain in suggests the Fed has only one good tool at its disposal.

Rising RRP

RRP participation is likely to steadily increase over the next few months and mechanically drain bank reserves. The rising participation would be due to increasing money market fund assets amidst declining alternative investment opportunities. In hiking cycles there is typically a lag of several months between the first hike and when yield sensitive investors begin to allocate into MMFs. MMF assets had been flat until early in the year, but now show steady weekly inflows that historical data suggests will continue. The investment opportunities for money funds will likely remain limited in the coming months, so these inflows would be directed into the RRP.

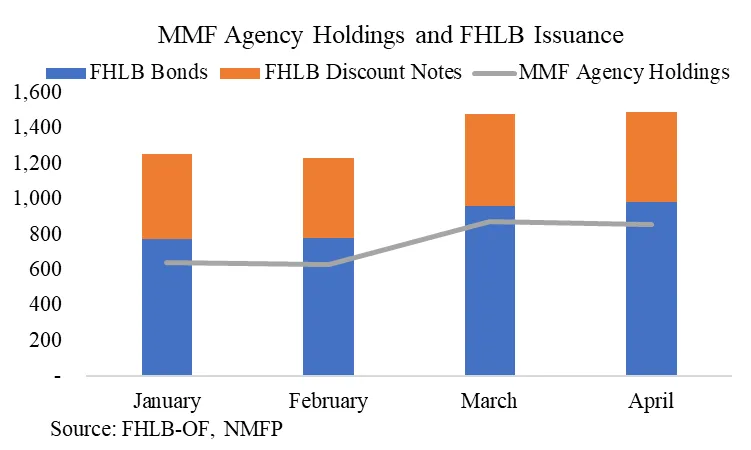

Money funds had been investing their marginal inflows into Federal Home Loan Bank debt, which grew rapidly during the March banking panic. FHLBs are government sponsored enterprises that largely borrow from MMFs to provide cheap loans to banks. MMF holdings of Agency debt rose by $200b in the March in line with the surge in FHLB issuance. The near record high volumes of federal funds, a measure excess FHLB liquidity, suggests declining demand for FHLB loans and thus declining FHLB debt issuance. MMFs may have no choice but to reinvest maturing FHLB debt into the RRP.

Replenishing the Treasury General Account

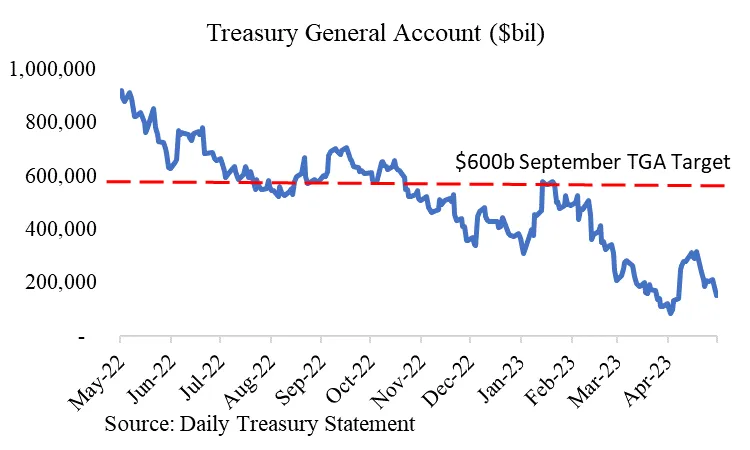

The Treasury’s expected replenishment of the TGA account from the current $150b to around $600b is likely to significantly drain bank reserves. The replenishment could be financed out of bank reserves or the RRP, but recent history shows that MMFs are no longer marginal investors in Treasuries. The marginal investors in Treasuries appear to be households, who would finance their purchases out of funds in the banking sector. Should that persist, then the TGA replenishment will amount to a rapid drain of a few hundred billion in bank reserves.

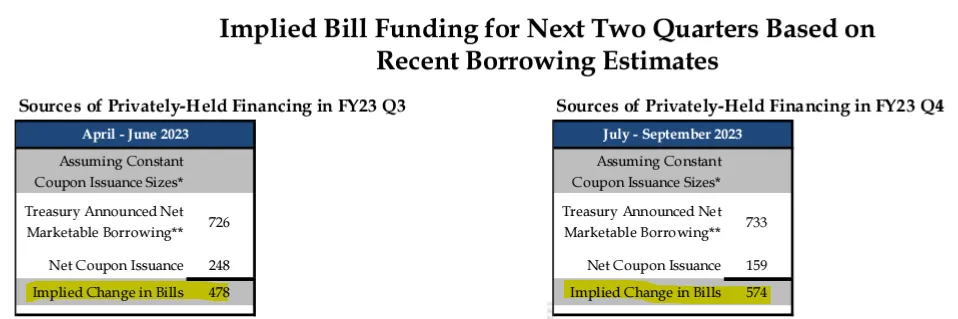

In the medium-term bank reserves would eventually be replenished through persistently high bill issuance. The Treasury is indicating a sizable $1t in bills issuance over the next 6 months. The rapid increase in bill supply should eventually be enough to raise bill yields and entice some MMFs with withdraw money out of the RRP and invest in bills. Those funds would flow out of the RRP, into the TGA, and eventually enter the banking system as the Federal government makes payments. The process may be slow, but bill issuance will only continue to increase in the months beyond as the fiscal deficit is expected to be persistently large.

One Big Tool

The exact timing of the move towards LCloR would largely depend on the resolution of the debt ceiling, which sets in motion the replenishment of the TGA. The vagaries of politics will dictate the timing, but a common estimate is a resolution around July. Regardless, bank reserves are set to steadily decline due to a growing RRP and on-going QT. The $2.2t estimate of LCloR could be too conservative, but the Fed may be afraid to find out.

An unwelcome move towards LCLoR would leave the Fed without many options other than a repeat of the 2019 Reserve Management Purchases. Pushing cash out of the RRP and into banks by toggling the RRP offering rate or adjusting counterparty limits is very unlikely because it interferes with the Fed’s ability to control rates. But purchasing bills to add reserves would be effective and tailored. The Fed would not perceive this to be a change in the stance of policy because it is duration neutral, but other market participants may view it differently.

20230516