Powell: Inflation Hotter & More Persistent – Taper Surprise?

Macro Tides Weekly Technical Review – Inflation Hotter & More Persistent

Chair Powell has acknowledged that supply chain disruptions are getting worse and not better and the increase in energy costs is adding a new dimension. “Supply-side constraints have actually gotten worse in some cases…and now we’re getting upward pressure on energy. The risks are clearly now to longer and more-persistent bottlenecks, and thus to higher inflation.”

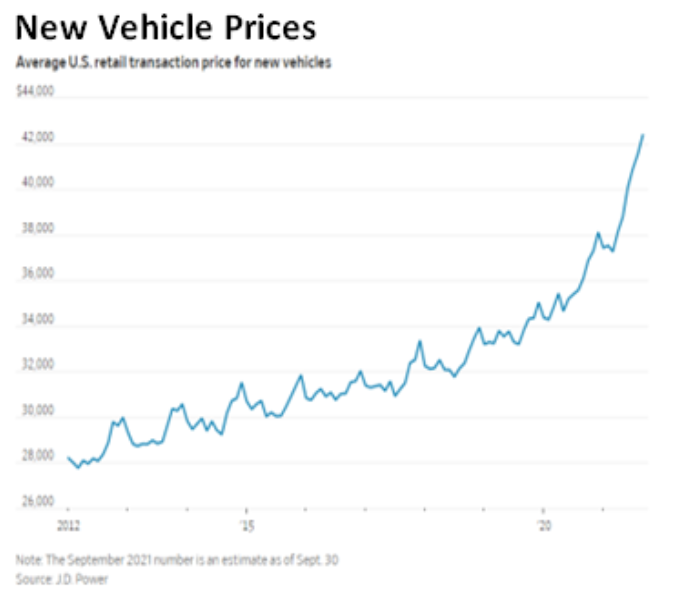

At the December 2020 meeting the FOMC estimated that PCE inflation would be 1.8% in 2021 and 1.9% in 2022. Core PCE was projected to be 1.8% in 2021 and 1.9% in 2022. In September the projections for 2021 and 2022 jumped to 4.2% in 2021 and 2.2% next year, with Core PCE being 3.7% this year and 2.3% in 2022. The FOMC and Chair Powell have lost credibility after having missed so badly relative to the projections made in December 2020 and every meeting since. The FOMC’s and Chair Powell’s credibility will take a further hit as inflation climbs in coming months.

Chair Powell has repeatedly said touted the Fed’s tools and that “No one should doubt that we will use these tools to guide inflation back down to 2% over time.” Does anyone really believe that the FOMC will ever vote to aggressively address inflation? I’m skeptical and the way the FOMC has handled the run up to the taper announcement has added to my doubting Thomas view. Using 5 months to tee it up tapering so the financial markets don’t throw a tantrum has also undercut the FOMC’s credibility. It reinforces the impression the FOMC will never do anything that may result in an OMG correction in stocks.

Markets are ready for the taper announcement at the November 3 FOMC meeting and have adjusted to the prospect that the FOMC will taper by $15 billion a month rather than the $10 billion expected a few weeks ago. The tapering process would finish in 8 months rather than 10 months if the monthly purchases are reduced by $15 billion a month.

There is another option that would likely increase the FOMC’s credibility and the perception of their commitment in addressing inflation. The FOMC would be served well by shrinking their monthly purchases by $20 billion. The whole taper process would end in six months so the FOMC could evaluate the timing of a rate increase 2 months earlier. That additional flexibility could prove helpful since numerous FOMC members have said they won’t taper and raise rates at the same time. Increasing the amount of the taper wouldn’t hurt economic activity much, so the economic downside would be negligible. In contrast, financial markets would reassess the FOMC’s resolve and think the FOMC might not allow inflation to get out of hand after all. The FOMC is concerned that inflation expectations might become ‘unhinged’ and there are indications that it’s already happening. The 3- year measure of inflation expectations is already the highest in more than a decade. By increasing the amount of the taper the FOMC could hold expectations in check even as inflation rises in coming months.

Should the FOMC taper purchases by $20 billion how will the financial markets react?

Will Treasury yields rise because the Fed purchases fewer bonds?

Will the stock market rally since a strong taper message will lower the chance of the FOMC having to raise rates more aggressively in 2022?

Will higher yields and less liquidity hurt the precious metals but help the Dollar?

The key to anticipating how markets will react is thinking beyond the conventional consensus. Most investors would like to think tapering is fully priced into the financial markets. Maybe, but sometimes the reality isn’t as tasteful as the theoretical which is always sometime in the future. Financial markets have been trading based on FOMC supplied liquidity. Less liquidity may not be outright bearish but it is surely less bullish, even if the FOMC tapers by $15 billion per month.

The prospect that the FOMC might taper by $20 billion a month is on no one’s radar.

Every week I review the changing fundamental landscape and review the Technical outlook for all of the major markets.

Last week the 10-year Treasury yield exceeded its October 8 high by 0.074%, but the 30-year Treasury yield held below its October 8 high. Do inter market divergences signal anything?

Blake Morrow and I have a conversation about the financial markets almost every Friday which is available at Traders Summit.

If you would like the most recent Weekly Technical Review or last month’s issue of Macro Tides just send me an email.

20211026