November Central Bank Overview

November Central Bank Overview

Major central bank rundown

It’s time for your central bank catch up. So, if you have been put off the loop, or just want a quick refresher then you can find it here. The link to the latest statement is at the bottom of each section, so just click there to read the bank’s central statement. Remember, there is no substitute for actually reading a central bank statement yourself and it will almost certainly be of great benefit to your trading.

Reserve Bank of Australia, Governor Phillip Lowe, 0.10%, Meets 07 December

Uncertainty reigns

In the October 05 meeting, the RBA indicated that they had hit rock bottom, that peak ‘bleakness’ had been reached. The impact from falling Iron ore prices, China’s slowdown in growth, the Evergrande crisis, as well as the delta variant locking down parts of the country all, left their mark on the Australian economy. In November’s meeting, the RBA’s decision tried to balance a few things as they did concede that interest rates could now rise in 2023. Remember that the RBA had previously stated that interest rates would not rise until 2024.

- * Firstly, as expected, they kept rates unchanged at 0.10 bps.

- * Asset purchases remain being purchased at the same rate of $4 bln per week.

- * They finished their yield target of 0.10 bps for the April 2024 Australian Government bond.

- This was all pretty much expected. The 2024 yield target was a slight ambiguity going into the last meeting. If you remember they stopped intervening in the bond market a few days beforehand. So, the speculation was that they had given up defending the curve, which they had of course. Sensibly, the RBA did not want to be fighting the sharp rise in front end yields. Was it a hawkish action? Yes, but their dovish rhetoric kept the AUD subdued.

Where now from here for the RBA?

Well, that all depends on two things according to the RBA: Inflation & wages.

Inflation

The RBA consider that inflation, or rather underlying inflation, is at an ok level. Underlying inflation is at 2.1% headline inflation is at 3% being driven higher by petrol, homes, and supply chain issues. The inflation forecasts are for underlying inflation to 2.25% over 2021/2022 & underlying inflation to 2.50% in 2023. In this regard ‘The Board is prepared to be patient, with the central forecast being for underlying inflation to be no higher than 2½ per cent at the end of 2023 and for only a gradual increase in wages growth’. Remember too that the RBA is also prepared to look through inflation of 3% or more if wages growth is not being seen at the same time.

Wages

The cash rate will not rise until – ‘actual inflation is sustainably within the 2 to 3 per cent target range. This will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently’. The latest wage data this week did not give any reason to think that the RBA would shift to hiking rates more quickly.

The key point

The AUD will be sensitive to four things now. Ideally, to get a clear direction on a trade it would be good to have as many of these factors as possible all pointing in the right direction.

- * Wages

- * Inflation

- * Global growth

- * Commodities – Iron Ore, Coal, Gold and copper prices

Finally, consider positioning from the COT report to see what leveraged funds and asset managers are doing. AUD looks very vulnerable to good news. Therefore, expect the AUD to rally hard on any better than expected wages news. Also, keep a close eye on Iron ore prices. A recovery here will be a lift for the AUD as around 1/4 of Australia’s exports are Iron ore.

Read the full RBA statement here

European Central Bank, President Christine Lagarde, -0.50%, Meets December 02

Holding meeting, despite policy change

The meeting on September 09 kept interest rates unchanged. The size of the bond purchases (PEPP) was unchanged at €1.85 trillion and APP purchases are continuing at the speed of €20 billion a month. However, the pace of the PEPP bond purchases has changed. The Governing Council decided that the pace of asset purchases under the PEPP programme could be slightly reduced. The PEPP purchases are now to be conducted at a ‘moderately lower pace’ versus the previous decision of a ‘significantly higher pace’.

Does this mean the ECB is tapering?

No. In the press conference, it was clarified that the tweak to the PEPP purchases is not considered ‘tapering’ by the ECB. However, to a certain extent, this is semantics as the ECB is recognising that less support is needed. The ECB is wanting to simply avoid overkill with too much APP purchases and not signal a material shift in policy outlook. Further PEPP discussion will take place in December. There was little new here at the meeting and the ECB is remaining on a ‘wait and see’ stance. Moving forward the focus remains on incoming data and the December meeting.

What comes after the PEPP programme expires in 2022?

If you cast your mind back to the July 23 meeting there were expectations that, after the ECB’s strategic review, the ECB would be revealing a more dovish hand. This was hinted at in the run-up to that last meeting by Christine Lagarde who said that the PEPP could ‘change’ into something else. Well, at this latest meeting they did not discuss what would come next after the PEPP pro-gramme ends. So, this is at least on hold for now, but Lagarde has recently reminded markets that the eurozone is ‘not out of the woods yet’.

The takeaway

Optimistic, but with a holding stance. Lagarde summarised that the eurozone economy rebounded by 2.2% in Q3 and is on track for strong growth in Q3. Consumer spending is increasing, but there are still 2 million fewer people employed than before the pandemic. So, there is nothing tradeable here for now. Just accept that the euro has a weak bearish outlook and the current negative sentiment around rising covid-19 cases is making it hard for the ECB to shift from an accommodative stance and supply chain bottlenecks continue to dog markets. Look for a surprise Calrida appointment to boost the EURUSD. Clarida will be more accommodative than Powell, so a surprise Clarida appointment should be a nice fast run-up higher in the EURUSD.

Read the full ECB statement here

Christine Lagarde’s press conference link here

Bank of Canada, Governor Tiff Macklem, 0.25%, Meets December 08

This meeting saw a hawkish shift from the BoC. At the last meeting the BoC held rates at 0.25%. Asset purchases remained at $2 bln and they see lifting rates around the second half of 2022. The hawkish tilt was that QE has now been ended by the BoC and rate hikes are now expected some-time in the middle quarters of 2022. Prior to the meeting the expectations were for the BoC to reduce QE from CAD$2 billion per week to CAD1$ billion per week and interest rate hikes were not ex-pected until the second half of 2022.

Inflation concerns

As with central banks the BoC expressed its concern for rising inflation. The BoC is now ‘closely watching inflation expectations and labour costs to ensure that the temporary forces pushing up prices do not become embedded in ongoing inflation’. The causes for the inflation by the BoC is seen as increased demand for goods, but shortage in labour and production & distribution alongside surging energy prices. The latest inflation data was not a massive cause for concern this week as it was on expectations unlike the UK and US prints. So, no drama from Canadian inflation to force the BoC’s hands yet.

The output gap

The BoC were correct in their assessment at the last meeting that they still saw the economy strengthening in the second half of 2021 with consumption, business investing , and government spending all contributing positively to growth. The narrowing in the negative output gap validated this outlook. The output gap is the difference between GDP and the potential GDP. It gives you a snap-shot of how the economy is performing compared to its possible performance. The current gap is less than it was in Q2 (-3 to -2%) and is now at -2.25 and -1.25%. The gap is expected to close around the middle quarters of 2022.

Summary

It was good news for the CAD out of the meeting and this should result in some CAD strength over the medium term. Like last time, and now especially with the BoJ such a low yielding currency, CAD strength over the JPY on deeper pullbacks makes sense. However, mark this point – a lot of good news was priced in for the CAD going into the last meeting.

So, it would be prudent to wait for a decent pullback in CAD before considering longs. Don’t forget that the Canadian dollar is one of the so called petro currencies alongside the Russian ruble (RUB) and the Norwegian krona (NOK). Stronger oil supports the CAD as around 17% of all Canadian exports are oil related. Canada’s top export is Crude Petroleum at over $66 billion and around 15.5% of Canada’s total exports. If it is good news for oil then it is good news for the CAD. The recent oil weakness on talk of emergency reserves flooding the market, albeit temporarily, is a near term drag on the CAD. However, here is one obvious candidate on the CADJPY chart for a medium term long.

Read the full BoC statement here

Federal Reserve, Chair: Jerome Powell, 0.125%. Meets 15 December

Flexible, but patient

At the last federal reserve meeting, the signalled taper of $15 billion per month occurred. The Committee decided to begin reducing the monthly pace of its net asset purchases by $10 billion for Treasury securities and $5 billion for agency mortgage-backed securities. All as expected and the taper was well flagged in advance. You can view the Yahoo Finance interview covering the release here.

The main question going into the meeting was how would the Fed manage inflation concerns around the pace of the taper. Would the Fed adjust the tapering speed? Could interest rates be increased even while tapering was still running? So, this meeting was always going to be about tone rather than the actual monetary policy decision.

On inflation

The Fed basically recognised it as an issue and moved away from the pure ‘transitory’ narrative. This was done by changing the statement to read that inflation was now ‘expected’ to be transitory & that the word ‘transitory’ did not appear in the press conference. The Fed took a step back from transitory in the statement as it means ‘different things to different people’. This means that some see transitory as 1 year and others as 6 months. Transitory is dependent on your timescale which does vary from person to person.

On jobs

This is a key sticking point. Jerome Powell does not think that the Fed is behind the curve, but stat-ed that needs to see more progress on jobs. He considers jobs back to ‘pre-Delta’ path as ‘good progress’. Jerome Powell dodged the question ‘is a 2022 hike appropriate? However, he did recognise that maximum employment could be reached by the middle of next year. So, that is potentially more hawkish and keeps jobs data front and centre.

The takeaway

The reaction to Jerome Powell’s speech was telling in the aftermath of the decision even though the decision itself was not obviously bullish or bearish. Yields started to fall around the world and, after the BoE pushed back on rate hikes as well as a dovish RBA in the same week the yields of bonds around the world started to fall. Markets began to re-price aggressive expectations of early rate hikes to combat inflation. One of the key beneficiaries of this drop in yields ought to be gold. If real yields fall (which they should with falling yields, but inflationary pressures) then gold could be a big beneficiary. Since then the market is trying to make up its mind on whether central banks will be forced to act or not.

The strength of gold around the year-end means that gold could be about to embark on a really strong run higher if yields drop and the USD drops along with inflation staying high. See here the talk about trading gold into year-end.

Bank of England, Governor Andrew Bailey, 0.10%, Meets 16 December

Heading into the last November Bank of England meeting investors were fully pricing in a 15bps hike to 0.25% with a further four 25bps being priced in for 2022. However, in a surprise to rate mar-kets, the Monetary Policy Committee voted by a majority of 7-2 to maintain the Bank Rate at 0.10%. The Committee also voted by a majority of 6-3 for the Bank of England to continue with its existing programme of UK government bond purchases maintaining the target at £875 billion and so the total target stock of asset purchases is at £895 billion. Saunders & Ramsden were the dissenters who were in favour of rate hikes. The rest of the MPC wanted to wait on jobs data before hiking rates and the market will be more cautious from here on in about pricing in Bank of England rate hike signals.

The GBPJPY upside outlook from the last central bank meeting report player out nicely. However, the upside moves have paused as SONIA futures show a quick repricing of interest rate expectations. Take a look at the SONIA futures to see the swift re-pricing the market made after the meeting.

1% rate rise by 2022

The Bank of England now has a market-implied path for the Bank Rate that rises to around 1% by the end of 2022. The BoE state that the UK economy is recovering and that interest rates will need to rise in tore to return inflation to the BoE’s 2% target.

Inflation is expected to fall back to around 2% in two years time

In the near term, inflation is set to rise to just under 4% for October of this year. This is mainly due to the impact on utility bills on the past strength in wholesale gas prices. CPI inflation is then expected to rise to 4½% in November and remain around that level through the winter, accounted for by further increases in core goods and food price inflation. Wholesale gas prices have also risen sharply since August. CPI inflation is then expected to peak at around 5% in April 2022, materially higher than expected in the August Report. However, the BoE do expect these pressures to fade: “the upward pressure on CPI inflation is expected to dissipate over time, as supply disruption eases, global demand rebalances, and energy prices stop rising’ and CPI inflation is projected to fall back materially from the second half of next year (2022)’. The inflation print was up across the board this week as the UK faces pressure to hike rates to control inflation. Yes, the outlook is what’s expected by the BoE. However, the pressure is on for the BoE to act. It’s the usual game of cat and mouse.

The labour market

At the meeting prior to this one the end of the furlough scheme was a key focus. The BoE were once again stressing uncertainties surrounding the outlook for the labour market, and the extent to which domestic cost and price pressures persist into the medium term. UK labour data out this week has shown a positive surprise with 247K jobs added vs only 185K expected. The unemployment rate was good at 4.3% vs 4.4% expected and UK average earnings were higher. This should give the Bank of England reassurance that a December rate hike would be appropriate.

Bottom line

Despite the sudden shock in rates futures markets the Bank of England is still expecting to raise interest rates to 1% in 2022. This keeps a weak bullish bias for the GBP. Wage and inflation data tick the BoE’s boxes, so a December rate hike is now being expected, Brexit risk remains a tail risk as the UK may trigger article 16 and that could suddenly weigh on the GBP.

Read the BoE full statement here

Swiss National Bank, Chair: Thomas Jordan, -0.75%, Meets December 16

This is interesting as the SNB is showing signs of growing impatience with the strong CHF. The SNB interest rates remain the world’s lowest at-0.75%. This is due to the highly valued franc (CHF) which has seen significant gains over the last few years due to safe-haven demand.

The SNB want a lower CHF

At their latest meeting, they repeated their willingness to intervene in the FX market in order to counter upward pressure on the Swiss franc. However, at this last meeting, the SNB were explicit about the highly valued franc. Previously they had said that they were willing to intervene ‘as necessary while taking the overall currency situation into consideration’. The shift underscores that the SNB hates a strong CHF and their patience is fractionally thinner. It’s probably been the Evergrande crisis spooking investors into the CHF that has peaked their attention. As an export-driven economy, they hate a strong CHF and are doing their best to make it as unattractive as possible. The market generally ignores this and keeps buying CHF on risk aversion which has been here in one form or another since around 2008/2009. Also, note that their trade surplus is high, boosting the CHF.

The bottom line and the EURCHF ‘opportunity’

The SNB will continue to intervene in the FX markets. The Swiss are always mindful of the EURCHF exchange rate because a strong CHF hurts the Swiss export economy. This is why there has been a shift in language about countering ‘upward pressure on the Swiss franc’. The SNB want a weaker CHF. The rest of the world wants CHF as a place of safety in a crisis, so we have this constant tug of war going on.

Read the full SNB statement here

For more details on the sight deposits check out SNBCHF.com. This site called the removal of the floor back in 2015, so well worth checking out.

The SNB are still content to be the lowest of the central bank pack and dissuade would-be investors by charging them for holding CHF. EURCHF for a 6-12 month hold is still worth considering, if not even more so now with the SNB’s patience wearing thin with a strong CHF. The problem with this trade idea is the timing. Get a turnaround out of Europe and one to jump on. You may try using the key tech, low leverage, and wide stops if you want to play this via FX. For a better option consider a EURCHF option ratio call. You can read more in the comments here.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, Meets December 17

The Bank of Japan still remains a very bearish bank and there is no sign of it exiting from its easy monetary policy. Once again the latest meeting saw no surprises and everything was as expected. Interest rates remain at -0.10%. The Yield Curve Control (YCC) was maintained to target 10-year JGB yields at around 0.0%. The vote on YCC was made by 8-1 votes. The only dissenter was once again Mr Katoaka. The BoJ expect current rates to stay at present, or at lower levels.

Was JPY weakness a worry to the BoJ? No

Going into the meeting the obvious concern had been the JPY weakness. Around the end of October, the monthly weakness of the JPY was quite notable.

However, the BoJ had no concerns and the weakness was seen as a normal move by Governor Kuroda. He said the move was within the range of current fundamentals and had only weakened a small amount. The weak JPY makes imports expensive, but the exports become cheaper. No complaints there then from the BoJ.

For years Japan has struggled to see any inflation, so with inflation rising around the world it was interesting to see that the BoJ now do expect consumer inflation to rise,. However, not by much and the latest inflation metrics for this year were lower than expected. Core CPI was down to 0.0% vs 0.6% expected and GDP growth was down as well to 3.4% vs 3.8% previous. However, the 2022 forecast for inflation is 0.9% and 1.0% for 2023. This is reflecting that Japan wholesale inflation hit a 13-year high (which puts a squeeze on industry profits) as the BoJ expect costlier input prices to be passed on to consumers.

The bottom line

The USDJPY symmetrical triangle breakout from the last central bank report turned out nicely helped by the JGB yield curve control as the US10 years broke higher post the September Fed meeting. The outlook is now different, but with no inflation worries for the BoJ and no fears over the weak JPY the JPY can remain a funding currency and is a great currency to pair with currencies set to raise rates. Is the carry trade back? It certainly could be, so don’t miss out on the JPY weakness as it is likely to remain an ongoing theme.

Read the full BoJ statement here

Reserve Bank of New Zealand, Governor Adrian Orr, 0.25%, Meets November 24

This October 06 meeting saw the anticipated rate hike by 25 bps to 0.50%. If you remember the previous meeting saw a resurgence of COVID-19 just before the rate decision and this led to the RBNZ holding rates. However, the situation for New Zealand is that their smaller economy leaves them more vulnerable to a surging housing market. On top of this theist inflation reading prior to the decision was at 3.3% y/y. This is the highest reading in 19 quarters.

It was this rising inflation that has caught the RBNZ’s attention. The RBNZ were explicit about rising inflation pressures, ‘cost pressures are becoming more persistent’. This recognition of rising inflation is significant. For many weeks central banks have been happy to consider inflation as transitory. It was at this meeting that it seems the inflation problem really starts to bite. The problem central banks will have is how to fix supply chain problems that cause inflation without hindering growth? It is like trying to square a circle.

At the previous meeting, the RBNZ had to decide which pressure they would react to; Covid or a hot economy. They reacted to both by not hiking rates and kept them unchanged at 0.25%. However, at the same time they saw see the OCR rising by one rate hike this year and 100bps next.

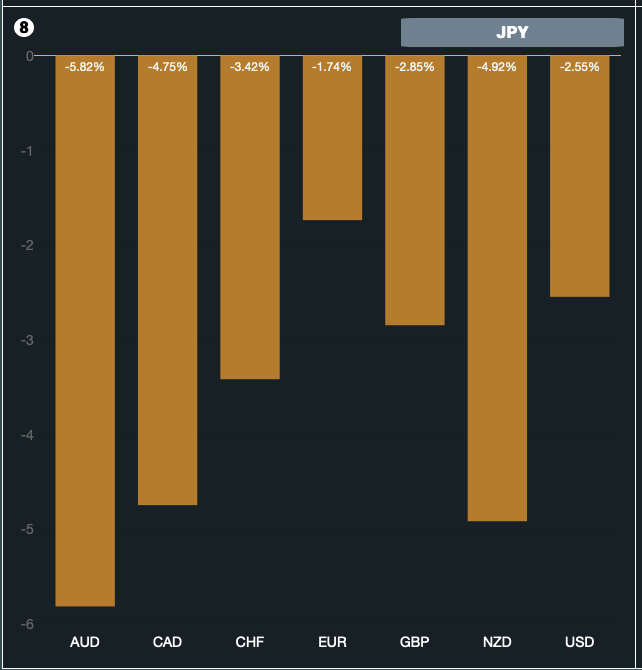

So, at this latest meeting, we saw the one rate hike that was expected. all this was a classic ‘buy the rumour, sell the fact response’. The hike was expected, so price rallied sharply higher on the announcement, before selling off. See the chart below.

The takeaway

The RBNZ meets this week and the OiS futures are pricing in a 100% chance of a 25bps rate hike. Some analysts also see a chance of a 50bps rate hike. This should keep the NZD bid into next week. If we see yields dropping lower than an NZDUSD long at the start of the week makes sense for a move higher in a ‘buy the rumour’ fashion. Just watch out for the selling of the fact. However, remember that RBNZ Deputy Governor Hawkesby said in October the RBNZ would be hiking rates by 25bps, not 50bps, at meetings due to the heightened uncertainty. Has this now changed with New Zealand withdrawing lockdown restrictions by the end of this month?

The RBNZ wants to keep options open and react as the economy reacts: The Committee noted that further removal of monetary policy stimulus is expected over time, with future moves contingent on the medium-term outlook for inflation and employment. Well, we know inflation is likely to keep rising and the RBNZ expect CPI to rise above 4% in the short term. Surely, inflation will be taking centre stage for the RBNZ moving forward and most traction for NZD direction is most likely to come from this quarter.

Read the full RBNZ statement here

20211122