I’m leaning short on the equity markets. I think the upside/downside [risk here] just doesn’t make sense to me when I have so many central banks telling me what they are going to do, This is a tough level [for the S&P 500] to talk about robust returns. [Central banks] are going to keep rates high for a while… Don’t ignore what these guys are saying. ~ David Tepper via Barrons

In this week’s Dirty Dozen Sixteen [CHART PACK], we pull way back and look at the really big picture. We dive into how a number of various cycles are syncing up (geopolitical, debt, conflict & cooperation, real vs. financial assets, etc…). And we lay out why the next decade(s) won’t be like the last.

**Note: Enrollment to the Macro Ops Collectivestarts today and will be open until the end of the week.

We’re entering an entirely new macro regime. One that will be vastly different than anything we’ve experienced over the past 50 years. It will no doubt be a target-rich environment for those macro traders and investors prepared and equipped to navigate it.

If you’d like to join us so we can tackle this new regime together, make sure to enroll in the Macro Ops Collective. We’ll be shutting down access Sunday, January 1st at midnight.

You can learn more about that Collective and what it can do for your investinghere.

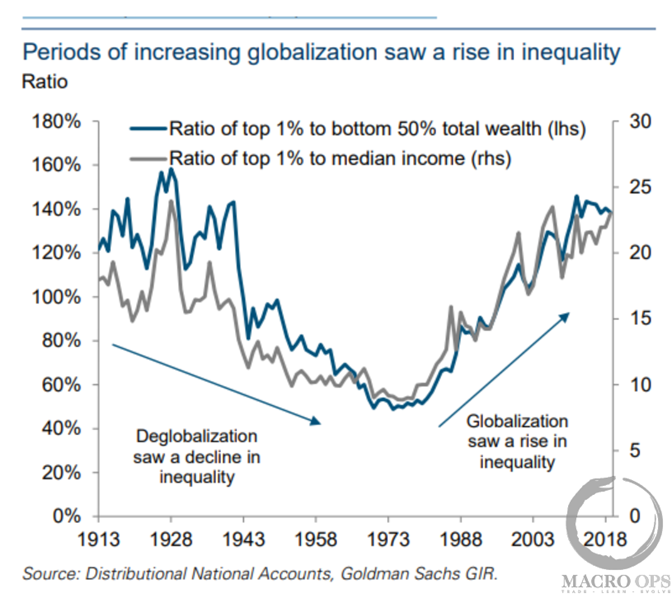

1. The most recent cycle of globalization that kicked off in the 70s was a significant driver of income inequality, as US labor was forced to compete with millions of low wage workers from Eastern Europe and China. This dramatically shifted power from labor to capital.

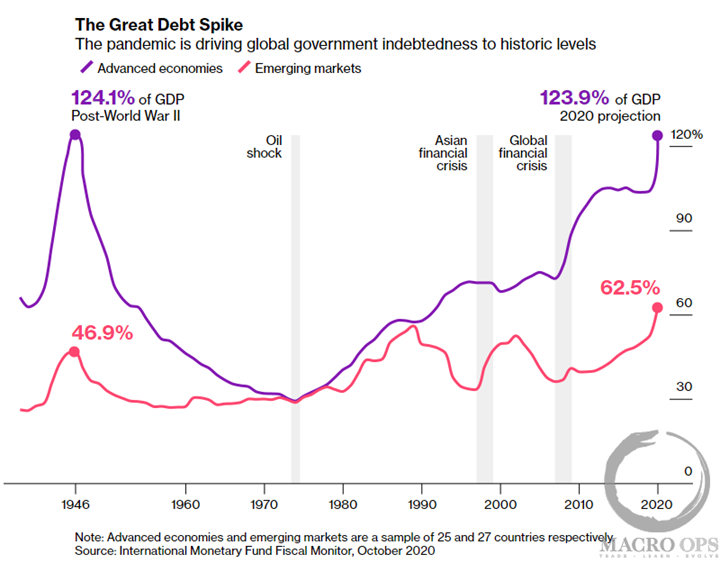

2. Labor lost its bargaining power. Real wages declined, and inflation trended lower on a secular basis, allowing interest rates to also move lower over multiple decades. Lower interest rates meant lower debt servicing costs. This meant more capacity for expanding credit, driving a Long-term Debt Cycle, not just in the US but in many other parts of the world.

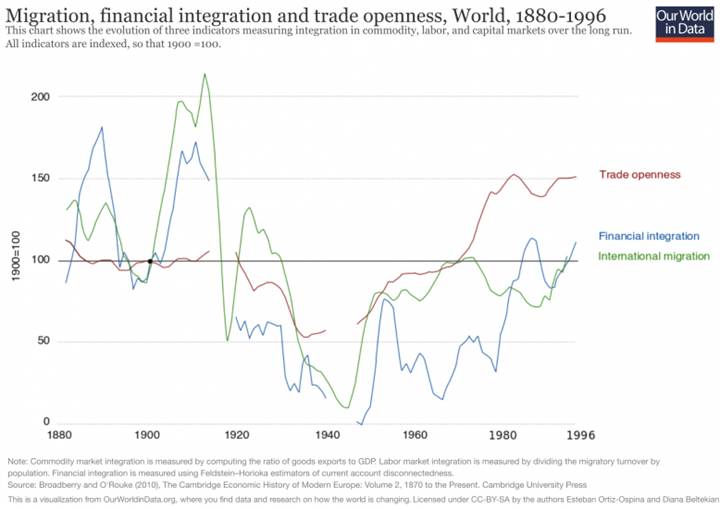

3. With the ability to lower interest rates each and every time the market and economy hit a rough patch, volatility was suppressed. Not just in asset prices and the economy, but in global affairs. Global integration and trade openness rose to levels last seen just prior to WWI, which was the peak of the previous globalization cycle.

4. But you can only lower interest rates so far. And you can only allow inequality to expand to a certain point. Eventually, you find that the volatility you thought you suppressed, was really just transferred to a later date. And the cycle begins to move in reverse…

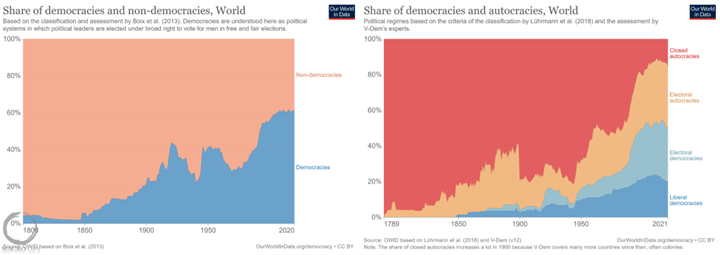

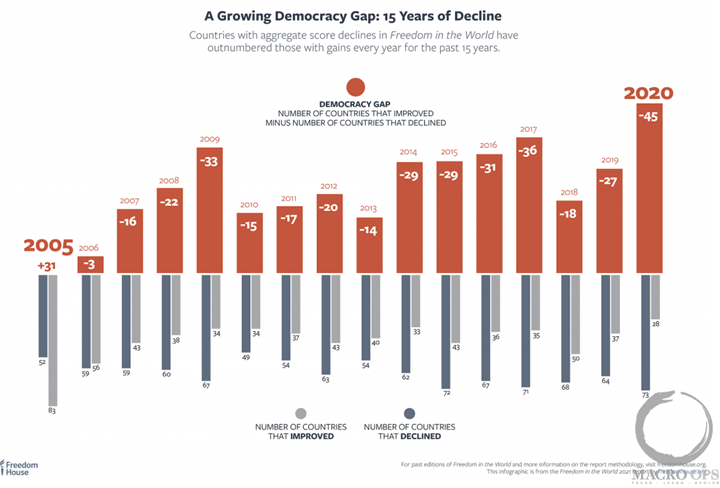

5. Many other global trends key off this cycle.Take the powerful long-term trend of democracy as an expanding form of governance. The trend is clearly up and to the right, as democratic systems are vastly more robust than their fragile autocratic counterparts.

But, as we can see, this trend doesn’t move in a straight line. It’s turning over now and the last time we saw a prolonged period of stagnation was during the previous period of deglobalization / major deleveraging cycle.

6. All of these cycles (debt, global integration, democracy, cooperation) peaked around the GFC and have been reversing ever since. They are accelerating now and there are a number of reasons why, which we’ll explore in an upcoming piece.

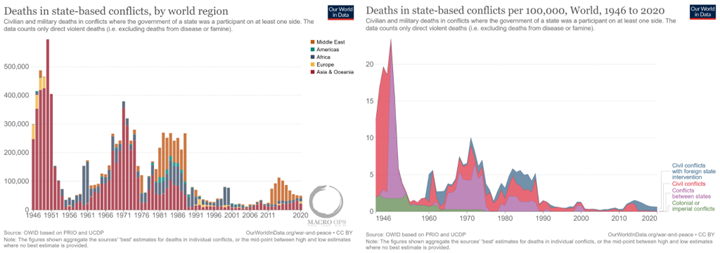

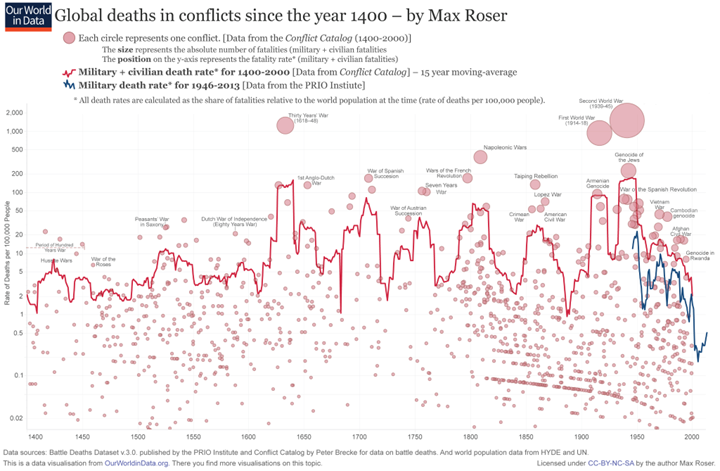

7. Volatility was suppressed across the board, including in the number and scale of violent conflicts.

8. These volatility cycles repeat time and time again throughout our history. And we’re just now coming off of an anomalous period of prolonged peace.

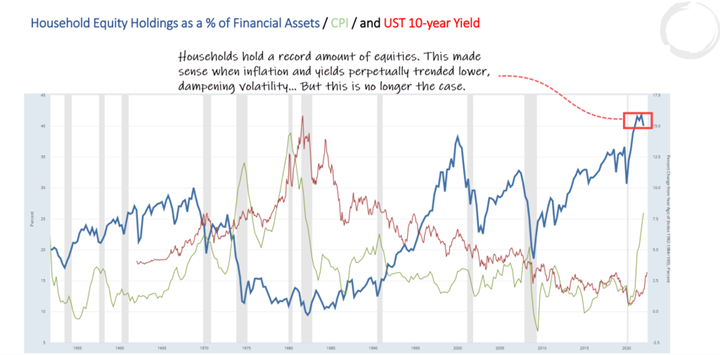

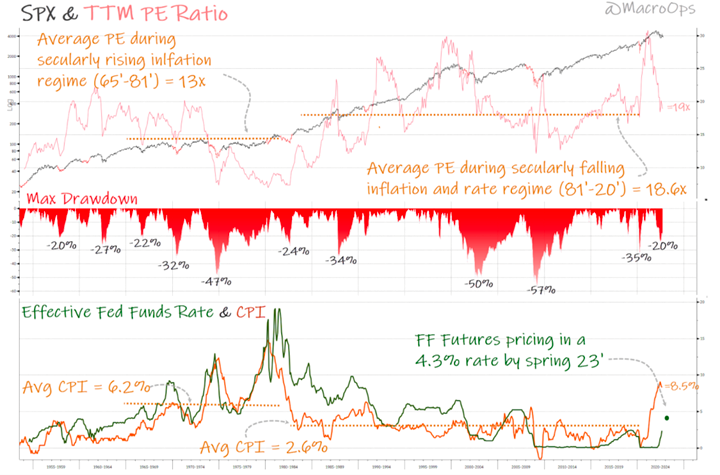

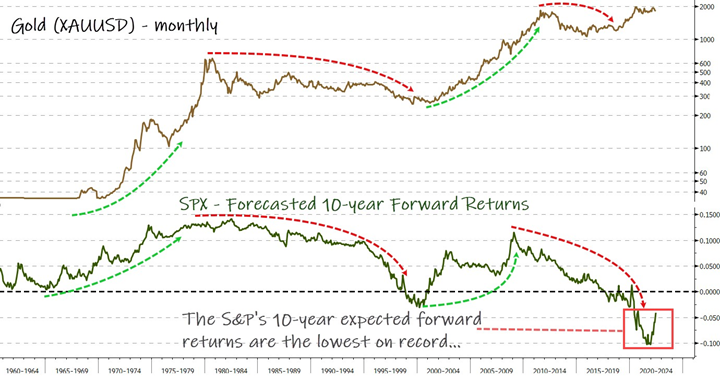

9. Increasing global volatility, higher inflation, and rising interest rates are now running up against a near-record high allocation in stocks.

10. I shared this chart back in September (link here). But where you think multiples will settle largely depends on where you think inflation will bottom. In an upcoming report, I’ll be making the case that we’re entering a new secular inflation regime, which will mean lower average multiples for risk assets.

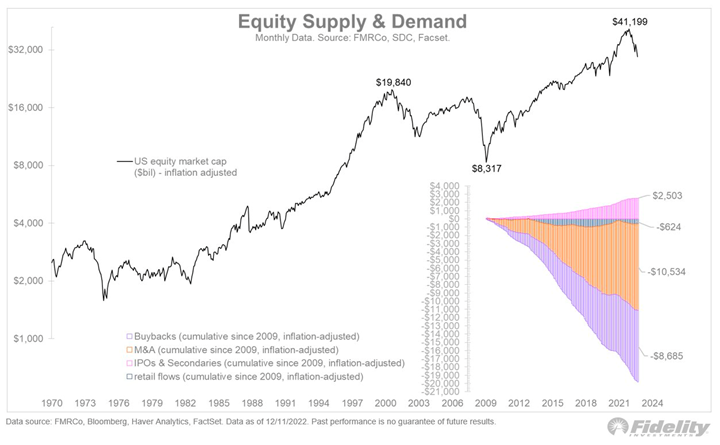

11. Net equity issuance is one of the Most Important Fundamentalswhen looking at long-term stock market returns, as I discussed here. Buybacks have been an incredible tailwind for the US stock market over the last decade (chart via @TimmerFidelity).

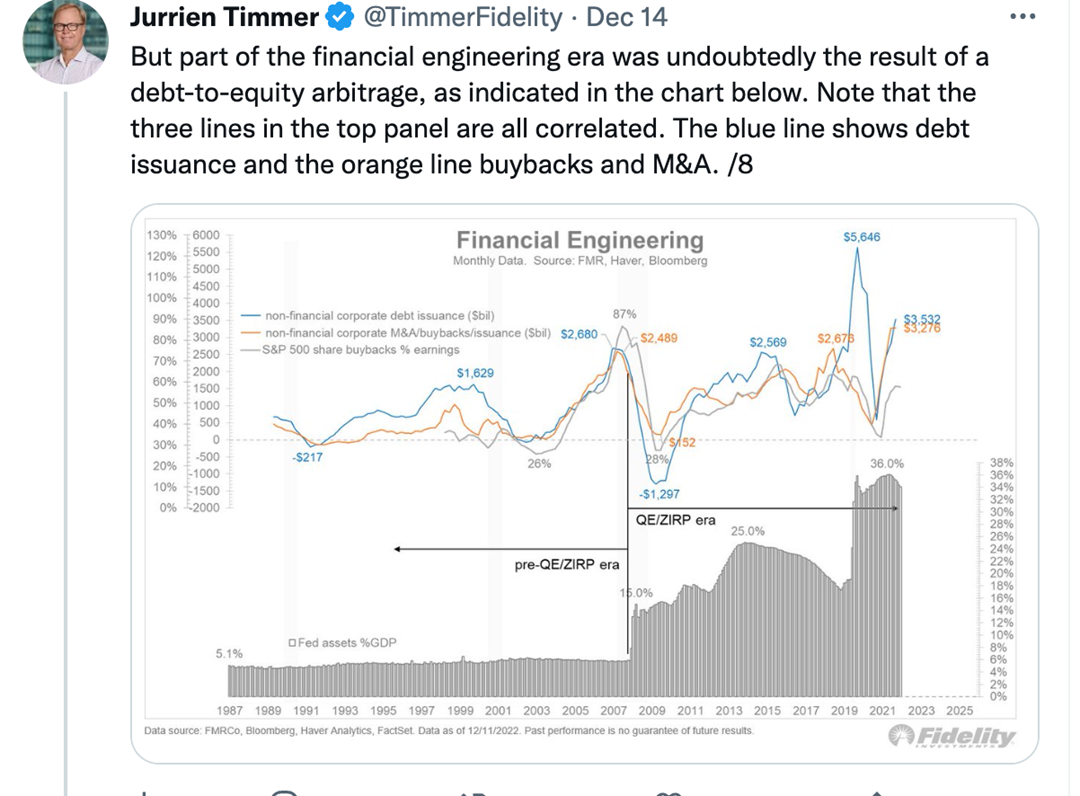

12. Falling interest rates drove the increasing use of leverage and financial engineering, which propped up asset prices, and suppressed volatility while increasing overall fragility. If higher structural inflation means higher rates and a more expensive cost of capital, what does that do to this tailwind? You can read Timmer’s full thread here.

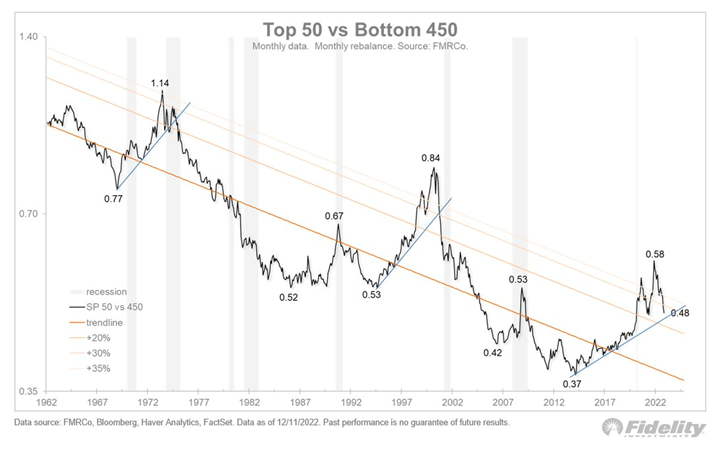

13. The mega-cap stocks were some of the most aggressive in buying back shares. They were also some of the biggest beneficiaries of globalization (cheap labor and EM growth), both of which helped drive concentration in these names to extremes. But it looks like mean reversion is on the way, which I wrote about in A Mutant Selling Deformity…(chart via @TimmerFidelity).

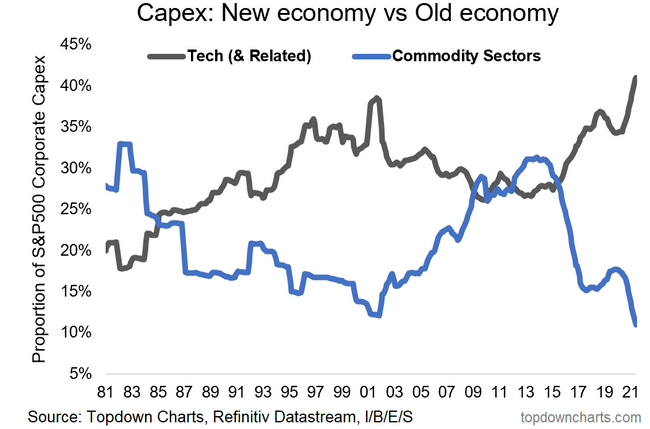

14. This was all part of a major CAPEX cycle, where capital crowded into “New” economy tech/growth stocks and SBF ventures, while “Old” economy commodity stocks languishedwith little access to financing (chart via @Callum_Thomas).

16. Higher structural inflation, rising geopolitical volatility, crowded positioning in equities with negative real expected 10-year returns, the bottom of a major CAPEX cycle in commodities… Own real assets.

**Note: We’re in the midst of a major macro regime shift. One that is only just starting to play out.

If you’d like to join us to tackle what is sure to be a Golden Era decade for global macro, make sure you enroll in theMacro Ops Collectivetoday. Enrollment will remain open until Sunday, January 1st.

The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world.

If you have any questions about our service and what it can do for you, make sure to click hereto schedule a free call with us.

Thanks for reading.

Stay safe out there and keep your head on a swivel.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.