May Central Bank Overview

May Central Bank Overview

It’s time for your central bank catch up. The link to the latest statement is at the bottom of each section, so just click there to read the bank’s central statement. Remember, there is no substitute for actually reading a central bank statement yourself and it will almost certainly be of great benefit to your trading. However, here is a summary analysis of the major central banks’ positions.

Reserve Bank of Australia, Governor Phillip Lowe, 3.60%, Meets May 2

RBA: Still in wait-and-see mode?

The RBA kept rates unchanged as expected at the April meeting and rates remain at 3.60%. The Board expects that some further tightening may be needed and is resolute in its determination to bring inflation back to target. The RBA decided to pause rates in April to see how the impact of previous rates works through the economy. It is in a ‘wait-and-see’ mode.

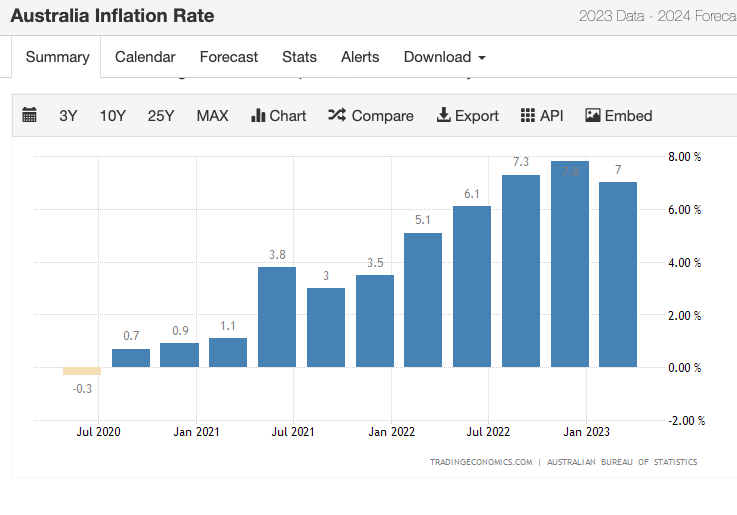

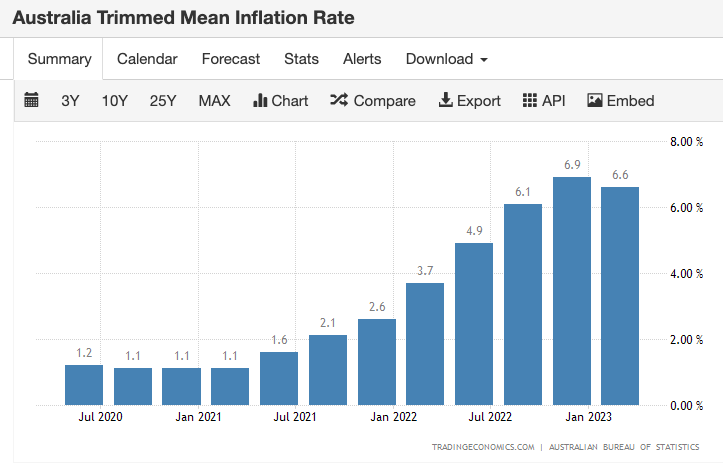

Peak inflation?

The RBA thinks it has reached peak inflation and is citing monthly CPI data suggesting that inflation has peaked. The headline and core inflation prints for Australia both show evidence of peaking inflation as outlined below, so that will be a welcome sign for the RBA.

This is significant that the RBA sees signs of inflation peaking and as long as these metrics keep falling the RBA will be able to keep rates unchanged. The next meeting date is on May 2, and short term interest rates are pricing a 91% chance of the RBA keeping rates on hold. So, no changes are expected again.

What to look for now

The RBA and the Fed are both meeting in the first week of May, so watch for a divergence in policy for a potential trade. If the Fed turns more hawkish and the RBA stresses that it feels inflation is peaked then that could open up a near-term move lower in the AUDUSD pair. One to watch for sure. See the full RBA statement here.

European Central Bank, President Christine Lagarde, 3.00%, Meets May 4

Hiked by 50bps in March, but is that the last of it?

The last ECB decision saw the ECB hike by 50bps. This hike was well signaled in advance, but just before the meeting, there were concerns that the banking crises from the US and Credit Suisse might prevent the ECB from hiking rates. However, the day prior to the last ECB meeting, Credit Suisse secured liquidity from the Swiss National Bank and intends to borrow up to $50 bln. FINMA also issued a statement in support of Credit Suisse saying that it ‘meets the higher capital and liquidity requirements applicable to systemically important banks’.

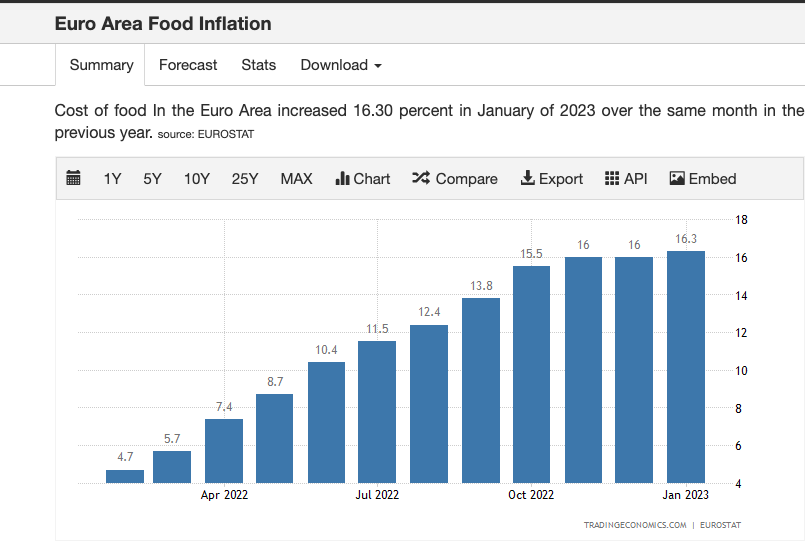

The ECB maintained that inflation is too high in the Eurozone and it expects it to remain that way for some time. The ECB stated that this inflation is increasingly coming from food, industrial goods, and services. Take a look below to see the steady rise in Euro area food inflation.

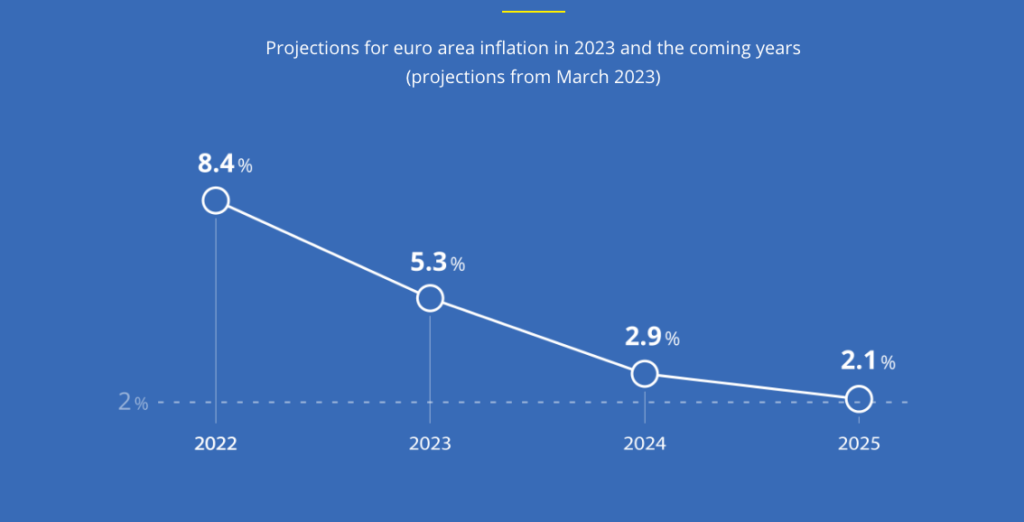

In the March meeting, the ECB is expecting Euro area inflation to fall to 5.3% this year and then down to 2.9% in 2024. However, note that the inflation projections below were done before the bank wobbles of early March and, therefore, are considered ‘stale’. They are also probably considered a touch too high now. The ECB, though, is stressing that it is maintaining its fight against inflation, so still expects any high inflation prints to increase speculation over more ECB rate hikes.

25 bps or 50bps hike?

Short-term interest rate markets are pricing in a greater than 1 in 4 chance of a 50bps rate hike. Euro core inflation is stubbornly high and the ECB needs to act to bring it down. The base case is that a 25bps rate hike is expected on Thursday, May 4, but do watch out for the forward guidance. Any EURUSD trades will also have to factor in the Federal Reserve’s meeting from the previous night. Watch for a divergence in policy expectations to drive prices. See the link for the press conference and statement here from the ECB.

Bank of Canada, Governor Tiff Macklem, 4.50%, Meets June 7

Bank of Canada holds rates as expected to 4.50%

Going into the Bank of Canada meeting it was not expected to be an eventful meeting. The Bank of Canada had indicated already it would be holding rates at 4.50% and there was no significant data prior to the meeting to indicate a shift from that strategy. The meeting was as expected with a few takeaways to note. The key point is, unsurprisingly, how the BoC is viewing its battle against inflation.

Inflation

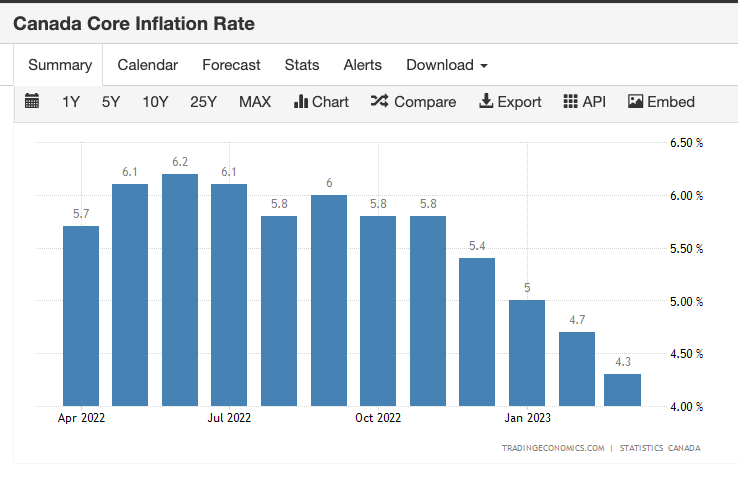

The Governing Council notes recent indication that inflation is falling and it expects inflation to fall to around 3% by this summer. However, the BoC recognised that core inflation around the world remains stubbornly high and that services, in particular, are showing inflationary pressures. This is due to the fact that the service rebound post-Covid is still working its way through global economies. During Covid people wanted manufactured products. Post-Covid people want to use the services previously denied to them. Core inflation and headline inflation are continuing to fall and both fell lower in the latest data from March. The core inflation print showed the lowest reading since January 2022.

What to look for going forward

As before, Canadian jobs data will continue to be important as the BoC noted that the labour market remains very tight. For central bankers when they are setting policy high employment means inflation pressure. Inflation, of course, will be important. Both the headline and core inflation continue to move lower step by step from last summer’s peak. The key tradable opportunities, therefore, will come from any out-of-consensus prints in either employment data or inflation data in the coming days before the next BoC meeting. The CAD at an index level remains within a 3-month range. Also, keep an eye on oil prices. Higher oil prices support CAD and the oil market is projected to tighten through 2023. Read the BoC’s full statement here.

Federal Reserve, Chair: Jerome Powell, 4.875%. Meets May 3

Federal Reserve: Last hike done?

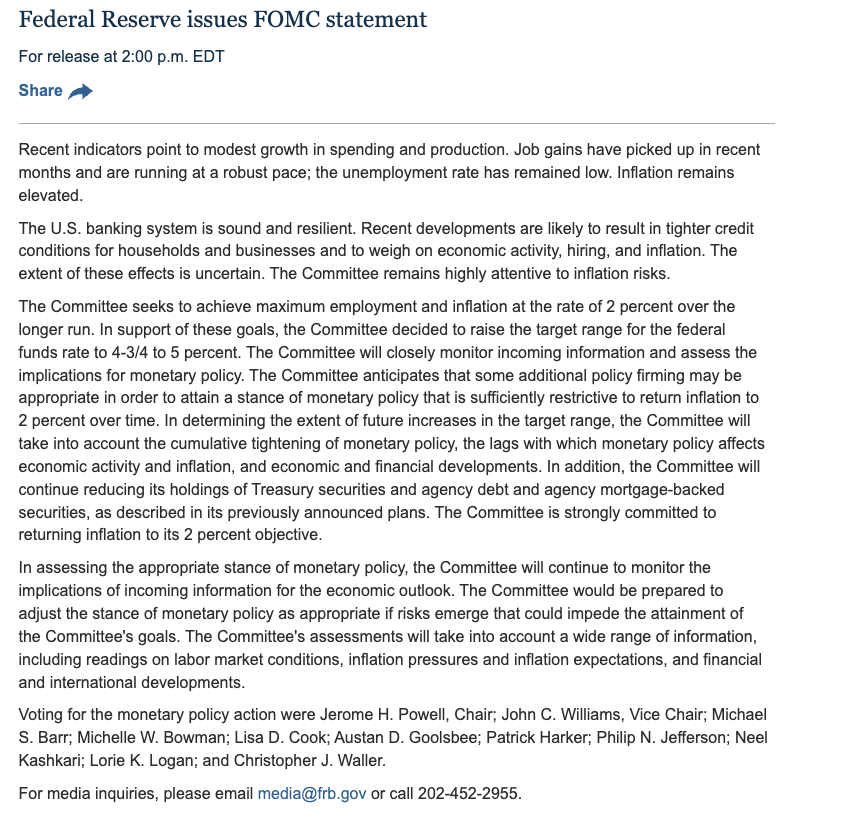

The Federal Reserve followed the ECB by hiking rates in its last decision. However, like the ECB, it also communicated that expectations of ongoing rate hikes should be reduced now, or at least it is keeping options open. The Fed played down banking contagion fears as it treads the fine line in trying to bring about a so-called soft landing. However, recent developments from First Republic Bank have meant some analysts see a greater chance of the Fed pausing rates in May and adopting a ‘wait-and-see’ approach. Banking sector strain is a huge issue for the global economy and will remain in critical focus, so will this be enough to cause the Fed to pause rates?

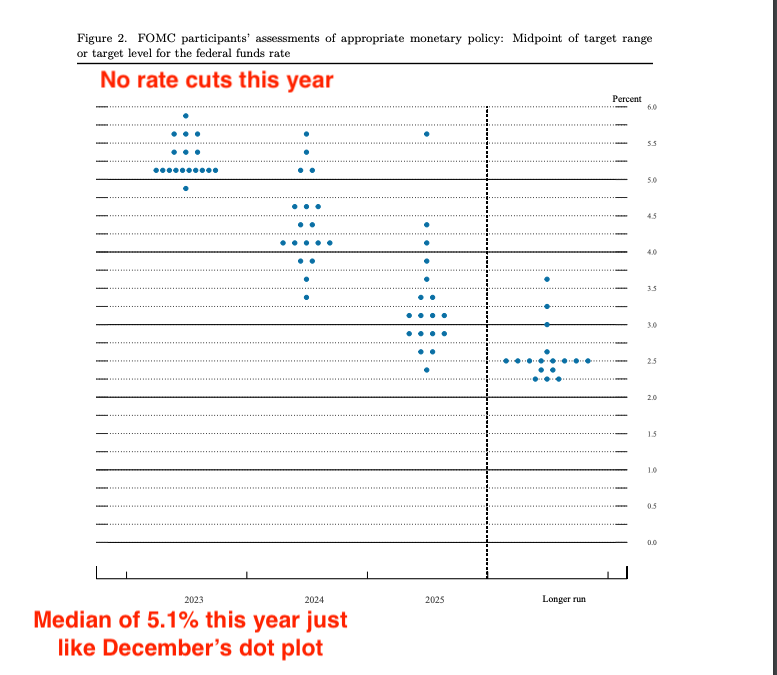

No rate cuts expected in 2023

The dot plot was always where the Fed would reveal what it really felt about the ongoing banking crisis. The from the prior meeting was the same as December’s dot plot. A median rate of 5.1% for this year and no rate cuts until 2024. Will that message be repeated again?

This was a pushback against the prior STIR pricing and was a more hawkish decision. The Fed is not expecting to cut rates and Powell repeated this in the press conference afterwards where he said, ‘Rate cuts are not in the Fed’s base case’. So, this was one of the reasons that stocks moved lower out of the press conference. STIR market rate cuts were priced out. When the statement was released market participants focused on the fact that the reference to ongoing rate hikes was removed. However, for May if the Fed is very hawkish watch stocks to potentially drop sharply lower. See the March Fed statement here and below. See the summary of economic projections here.

Bank of England, Governor Andrew Bailey, 4.25%, Meets May 11

Inflation battle lingers

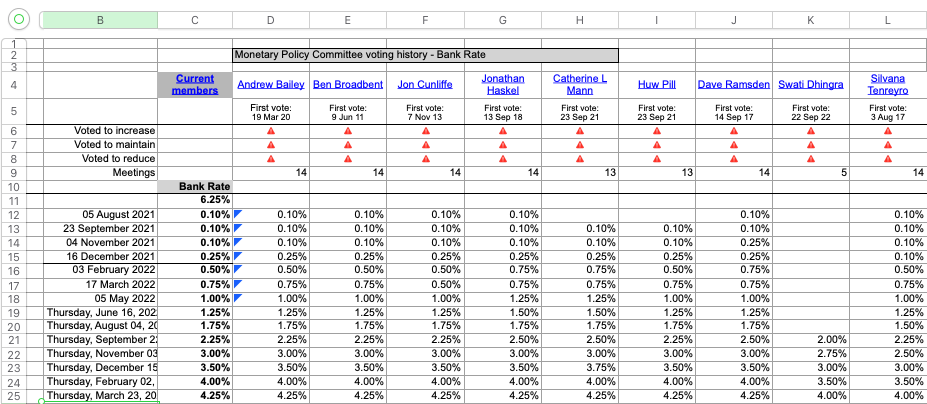

The Bank of England reflected confidence in its banking sector as it said that the Financial Policy Committee brief to the Monetary Policy Committee reported back that the UK banking system is resilient. So, this banking resilience gave the BoE confidence to hike rates by 25bps with a 7-2 vote split in the face of surprisingly high inflation. Dhingra and Tenreyo remained dovish dissenters citing to keep rates unchanged. This was entirely unexpected.

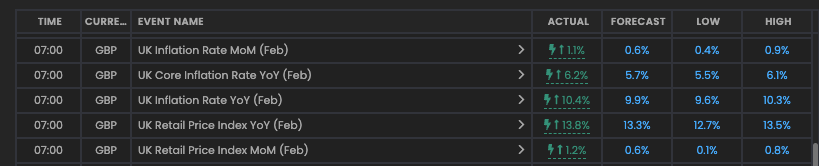

The Bank of England explained how the latest inflation data had taken the committee by surprise. February’s print shows the first increase in inflation in four months with the main pressure coming from the cost of food and non-alcoholic drinks. March inflation was still in double digits above the market’s expected of 9.8%.

Furthermore, it wasn’t just the headline that showed persistent inflation as the whole UK inflation set showed an aggregate beat exceeding economists’ maximum expectations. See below from Financial Source’s calendar.

Inflation is still ticking higher

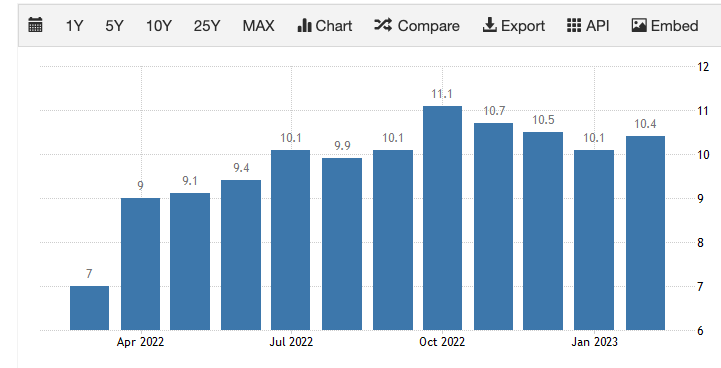

The UK is currently facing double-digit inflation, with headline inflation reaching 10.1% y/y for March and core inflation at 6.2% y/y for the same month. This has raised concerns that inflation could become entrenched in the economy. Additionally, the latest average earnings data for February came in at 6.6% 3M/yr, which exceeded economists’ maximum expectations, leading to more wage demands being met.

Given these circumstances, the Bank of England may need to adopt a more hawkish approach to hiking interest rates in the near term to curb inflation. The MPC may then need to reassess its stance on a case-by-case basis as new inflation data becomes available. The BoE recognizes the risks of high inflation becoming embedded in the economy and the BoE will likely need to act to address it. Will it signal another hike to come again even if it hikes again on May 11? Read the full BoE statement here.

Swiss National Bank, Chair: Thomas Jordan, 1.50%, Meets June 22

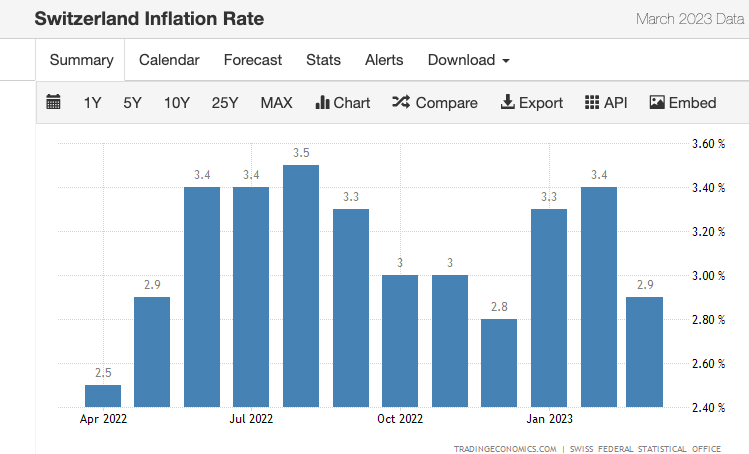

In the March meeting, the Swiss National Bank (SNB) hiked rates by 50bps as expected to bring interest rates in Switzerland up to 1.50%. The SNB, like central banks around the world, has been responding to an uptick in its domestic inflationary pressures. The February headline inflation print for Switzerland is at 3.4% for February and is moving back up to the August peak of 3.5%. However, the March print is now moving back down again with a 2.9% print.

However, the March reading for the core inflation rate showed an uptick to 2% which is above the high summer reading of 2%. On balance, there is nothing happening in Switzerland that is very different from the rest of the world, headline inflation falling, but the core remains stickier.

The takeaway

The SNB is expected to hike rates by 25bps at the next interest rate meeting and the terminal rate is currently at 2.00%. There is not a lot to focus on for the CHF apart from any surprise moves in inflation which will likely impact interest rate expectations. You can read the SNB’s full statement here.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, Meets April 28

BoJ fails to live up to yield curve end speculation

At the end of last year, the BoJ unexpectedly tweaked the Yield Curve Control band to +/- 0.50% in order to increase bond purchases to JPY 9 trillion in Q1 2023. At the time, the BoJ played down the significance of this move saying it was to improve market functioning and encourage a smoother formation of the entire yield curve. However, speculation is still firmly in place that the BoJ is preparing to exit its ultra-loose monetary policy in April this year when Kuroda retires and Kazoo Ueda leads the BoJ. Governor Kuroda has kept the yield control in place but he has now left office. Inflation in Japan is relatively low compared to inflation levels around the world even though the last reading in January was the highest in Japan since 1981 with a y/y reading of 4.3%. The BoJ, however, still doesn’t see the current inflationary pressures as sustainable, so it doesn’t want to hike rates to contain inflation like many other central banks around the world. To underscore the point BoJ’s Kuroda said, it is premature to debate the specifics of any exit from monetary easing; policy rate and balance sheet are the main things to consider when the debate begins. The exit should only be considered when the 2% inflation target is sustainably achieved. Most analysts still expect the BoJ to exit its ultra-loose monetary policy. If/when it does, it is likely to expect the JPY to strengthen.

No exit surprise expected from Governor Ueda in April

This piece was written just prior to the BoJ meeting and no surprises were expected from Ueda. You can read the full BoJ statement here.

Reserve Bank of New Zealand, Governor Adrian Orr, 4.75%, Meets May 24

RBNZ: Considered larger 75 bps hike

In the last RBNZ meeting, on February 22, markets were expecting a 50 bps rate hike. The surge in inflation had shown some signs of topping with January’s print coming in the same as the prior.

The QoQ reading was at 1.4% for January which was at the lower end of the recent range.

However, the RBNZ did not take comfort from these possible signs of inflation topping, and hiked by 50bps (as expected) and maintained its views for a terminal rate of 5.50%. The committee considered a hike of 75 bps and this was noted as a potential catalyst for sending AUDNZD lower prior to the event. The recent impact of Cyclone Gabrielle was seen as unlikely to impact the medium term monetary policy outlook although some short term prices spikes were expected as a direct impact in the near term.

Inflation still too high

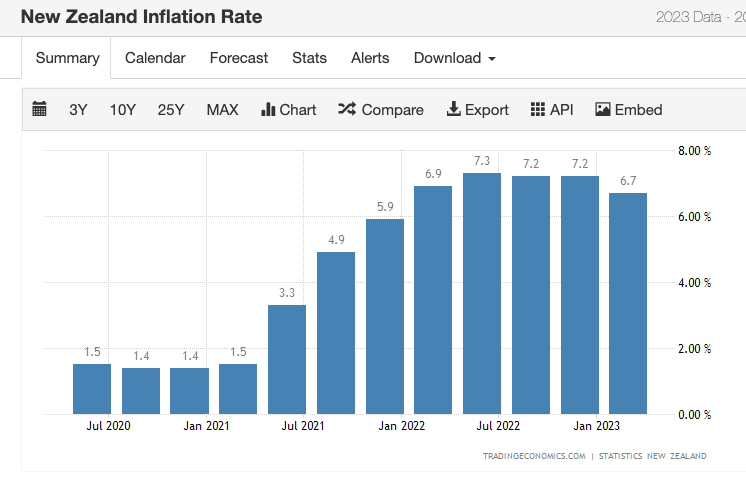

The recent pullback in inflation pressures was noted, but the RBNZ still considered core consumer inflation too high. New Zealand inflation data looks like it could have peaked with teh headline falling to 6.7% for February.

The takeaway

Going forward inflation data will be key and any big jumps lower in NZD inflation data will allow sudden weakness to creep into the NZD. This could be a good opportunity for short-term traders to look out for. You can read the full RBNZ statement here.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

20230428