Macro Tides Weekly Technical Review March 16th 2022

Macro Tides Weekly Technical Review

China, War Hopes, and the FOMC

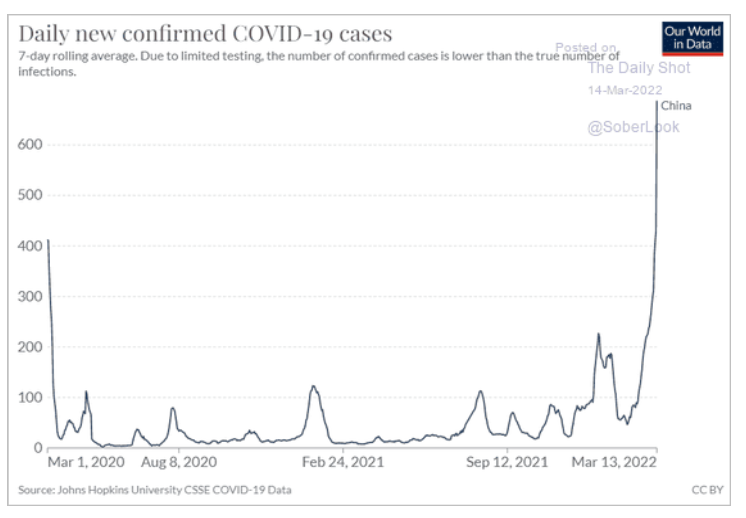

In October China’s most senior leaders will assemble at Beijing’s Great Hall of the People for the 20th National Congress of the Chinese Communist Party, which occurs every five years. The next meeting will be different than the prior 19 meetings in that President Xi will be ‘elected’ to an unprecedented third term. The path to his coronation will be made easier if China’s economy is improving. Toward that end China’s government tried Wednesday to reassure jittery investors by promising support for the real estate and technology sectors after regulatory crackdowns caused stock prices to plunge. This is a major reversal from Xi’s crackdown on real estate and large technology firms. The response in the Chinese stock market was immediate and many tech stocks soared by more than 25% in China and in the US. COVID infections have been hitting records and China has shut down cities to quell the outbreak, which raised concerns that a slowing Chinese economy would pile on to the global slowing due to the Ukraine War. The shift in policy indicates that China will do more to stimulate growth, and coincidently, make sure the economy is in good shape just in time for the big meeting in October.

Investors continue to hope that continued talks by Russia and Ukraine will lead to a cease fire. Russia has demanded that Ukraine recognize Russian sovereignty over Crimea, separate statehood from Ukraine for Donetsk and Luhansk, and guarantee that Ukraine will never join NATO by incorporating this pledge into its national constitution. It is unlikely that Ukraine will agree to these terms. The Ukraine War is likely to drag on for months.

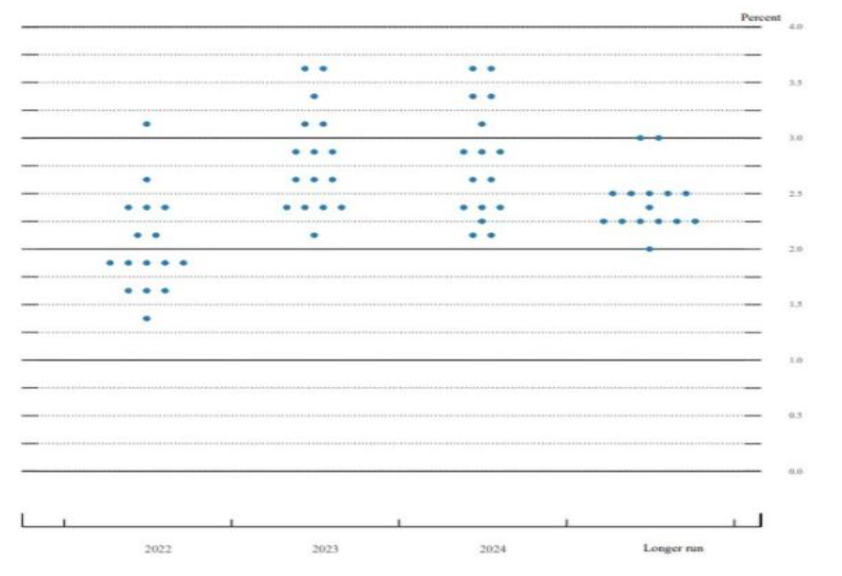

The FOMC increased the federal funds rate by 0.25% as expected, but the dot plot of individual members suggests that most of the members are on board with the FOMC increasing the funds rate 6 or 7 times in 2022. The S&P 500 dropped 95 points in reaction to the dot plot and the FOMC’s statement which was more hawkish than expected by Wall Street. The FOMC has earned a high level of skepticism after sticking to the mantra that ‘inflation will be transitory’ well beyond its expiration date. In the short run the FOMC will beat the hawkish drum.

In the March 14 Weekly Technical Review I noted that the market was oversold which could support an oversold bounce. “The market is oversold so another brief bounce is certainly possible. However, the bounces off 4200 (red line) have become progressively weaker, so a close below the green trend line (4160) could lead to a waterfall decline that brings the S&P 500 near 4000 sometime this week.” China’s intervention tossed the market a lifeline and a jolt which outweighed the message from the FOMC.

The market was deeply oversold at the January 24 low and the bounces since then have gradually worked off most of the oversold condition. The black line is zero and the 21 day Net Advances minus Declines Oscillator is expected to approach the red line before this rally terminates.

The S&P 500 rallied 302 points off the February low of 4115 to a high of 4417. An equal rally would target a high of 4460. The bigger picture has not changed. When this rally is over the S&P 500 is expected to at least drop below 4200 again, with a better than 50-50 chance of falling below 4000 still active.

Emerging Markets

China’s policy shift to provide more support for its economy is what I’ve been waiting for before recommending any Emerging Market ETFs.

I would recommend taking a 40% position in these ETFs. If a ‘normal’ position for you is 5% then a 2% position is warranted.

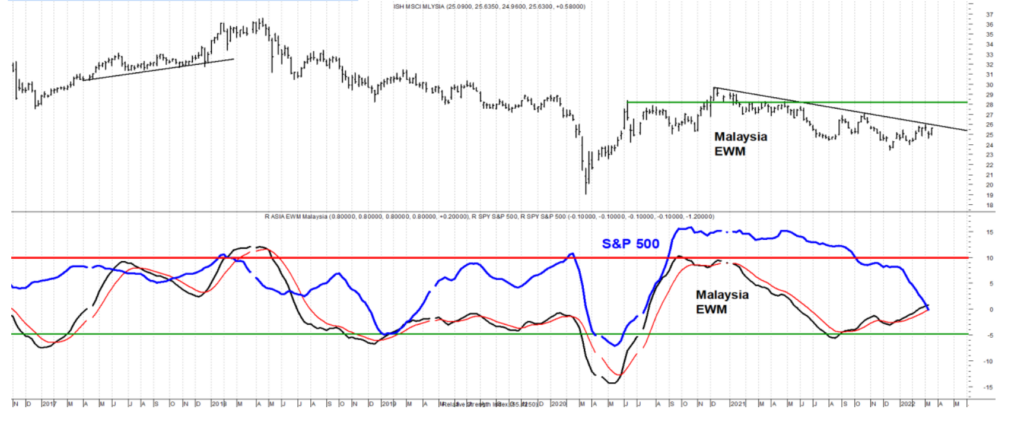

Malaysia

As the Relative Strength of the S&P 500 has been falling, the Relative Strength of Malaysia (EWM) has been rising. If EWM is able to rally above the declining black trend line, EWM has the potential of rallying to $28.00.

The improvement in Malaysia’s relative strength to the S&P 500 is apparent in the top panel of the daily chart. The MACD – RSI was modestly oversold and crossed the red trigger line today.

South Korea

The Relative Strength of South Korea (EWY) has dropped below the green horizontal line in the bottom panel, and EWY has fallen to an area of support (green horizontal line EWY). The expectation is that EWY’s Relative Strength will begin to improve and the support will hold.

The Relative Strength of EWY in the top panel has been going sideways since January 24. The MACD-RSI turned up today. EWY has the potential of trading up to $77.00 – $80.00.

The Daily Shot

A number of charts in this letter were from The Daily Shot. https://thedailyshot.com/.

In each week’s Weekly Technical Review I cover economic developments, monetary policy, S&P 500, Treasury yields, Dollar, Gold, Silver, Gold stocks, and when it is timely the Euro and WTI oil.

Check out MacroTides.com to learn more. If you would like a complimentary issue send an email to JimWelshMacro@gmail.com

Macrotides.com

jimwelshmacro@gmail.com

760-710-1956

20220317