Macro Tides – “Euro Strength and Outlook”

Foreign currency traders have taken a large long position in the Euro which has helped it rally +15.6% versus the Dollar since March 23. As discussed in the January Macro Tides I thought such a big increase in the Euro’s value would get the attention of EU policy makers. “The Euro has rallied +15.6% since bottoming on March 23 through December 30. A stronger currency makes European exports more expensive and increases deflationary pressures. This is neither good for economic growth or making progress towards the ECB’s goal of getting inflation up to 2.0%. There is a good chance that in the first half of 2021 ECB president Christine Lagarde will express concern about the Euro’s strength, which would give currency traders a strong signal to sell the Euro and potentially short the Euro.”

In early January the Euro rose to a six year high against the Dollar which did get the attention of EU policy makers. On January 27 Klaas Knot, who is the head of the Dutch central bank and a member of the ECB governing council, was interviewed by Bloomberg and was asked about the ECB’s inflation target and the strength of the Euro. “That is something we of course monitor very, very carefully. It’s one of the factors, not the exclusive factor, but one of the factors we take into account when arriving at our assessment of where inflation is going to go.” Klass went on to say that the ECB has the necessary tools, including interest-rate cuts, to prevent any further strengthening of the euro undermining inflation.

What Klass did not mention was jawboning by members of the ECB to communicate to foreign currency traders that it’s OK to sell the Euro. Klaas’s comment is almost verbatim those expressed by Mario Draghi in March 2014 which I discussed in the April 2014 Macro Tides. “At the ECB’s monthly news conference on March 6, Mario Draghi said that the strength in the Euro since July 2012 had shaved 0.4% off annual inflation. “The strengthening of the Euro exchange rate over the past one-and-a-half years has certainly had a significant impact on our low rate of inflation and, given current levels of inflation, is therefore becoming increasingly relevant in our assessment of price stability.” Foreign currency traders got the message after Draghi repeated his assessment after the May 8, 2014 ECB meeting. “The ECB’s governing council is comfortable to easing policy at their meeting in early June. The strengthening of the exchange rate in the context of low inflation is a cause for serious concern.” After peaking at 1.399 on May 8 the Euro plunged to 1.046 in March 2015.

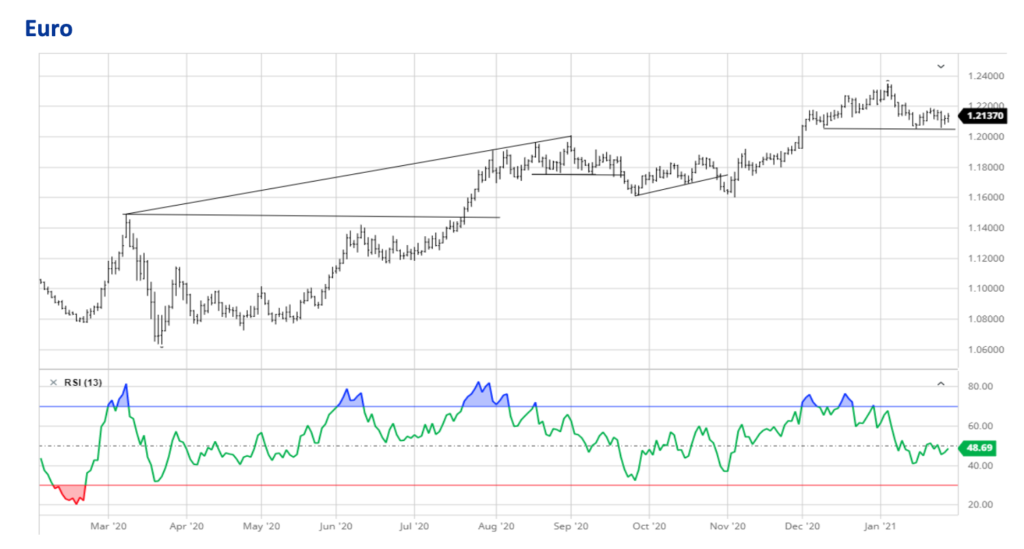

Just as in 2014 it may take more than one comment to get foreign currency traders attention. The high in early January was 1.2390 and any move above this level is likely to illicit more comments by a members of the ECB governing council expressing displeasure about the Euro’s strength. A decline below the horizontal trend line at 1.2050 should lead to additional weakness (chart below).

The Euro comprises 57.6% of the Dollar index so any weakness in the Euro will give the Dollar a lift in the short term. If the ECB pursues a weaker Euro through additional rates cuts or jawboning, the Dollar will rally despite record setting federal budget deficits and a large U.S. trade deficit. The trend in the Dollar is determined by more than just the economic fundamentals of the U.S., which demands a broader understanding of global economics than hyperbole statements about a looming Dollar Crash.

Jim Welsh