Is the Market Wrong on US Inflation?

Is the Market Wrong on US Inflation?

It was the Fed that originally got it wrong on US inflation seeing it as ‘transitory’. The Fed then started on a rapid path of rate hikes moving up in continuous 75bps moves and is expected to move up by 50bps on Wednesday. Furthermore, the Fed is set to signal more increases in 2023 as it brings rates up to 4.375% on Wednesday. However, has the market become too complacent surrounding the Fed’s path? That depends on the path of inflation from here.

The easy interpretation

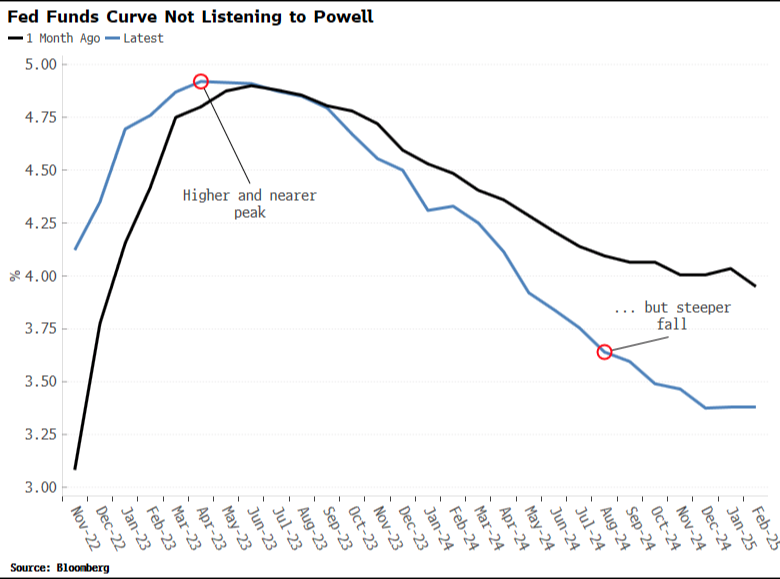

The ‘easy’ interpretation of what the Fed is doing is that it is hiking/has hiked aggressively and can now stay around 5% for a period before starting to cut rates around the end of 2023. The Fed can then cut by around 150bps plus as the US economy can recover. This is the standard ‘recession’ outlook. The current outlook is for a sharper rise in the Fed’s rates, but a steeper fall. Look at the blue line to see how the expectations have changed recently (blue line) from around a month ago (black line).

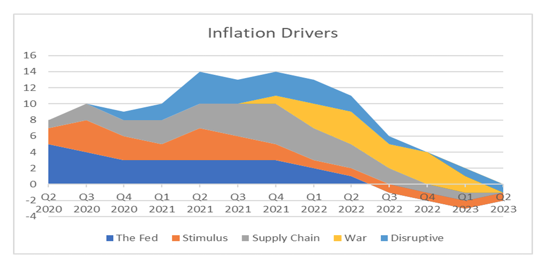

But is that ‘easy interpretation correct’? The problem is that the message is very mixed. Consider two points recently made in a Bloomberg piece. According to Academy Securites’ Peter Tahir, the near-term drivers of inflation have fallen. The Fed is hiking, the stimulus is falling, supply chain issues are resolving, and the Ukraine/Russia conflict may be peaking. All of which are showing facing inflationary drivers.

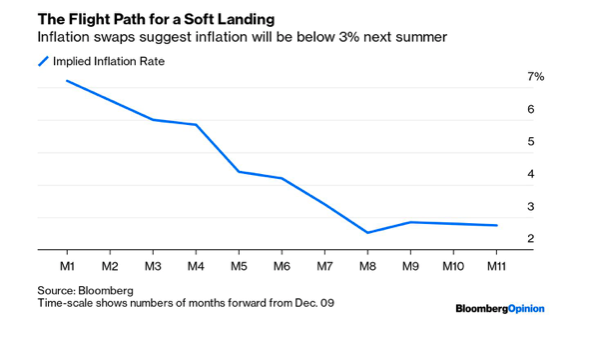

Secondly, Inflation expectations have also been falling as expectations for implied inflation swaps have fallen.

That’s the argument for inflation falling. However, the argument against it is that the latest PPI print from the US was strong with the PPI y/y headline beating expectations of 7.2% at 7.4%. The last NFP jobs print showed elevated wages and the 5-year US Michigan inflation expectations rose to 3% from 2.9%. The core PCE prints are also firmer, so jobs and inflation data are not yet showing a definite drop.

The conclusion

This makes it hard to know whether the market is correct on rapidly falling inflation. If inflation remains high then we may need to see another round of Fed hikes, a prospect that the market is assuming won’t happen. So, remember medium/long-term positioning is too tricky right now to confidently call and we need to see incoming labour and inflation data to get a clearer sense of direction. If the Fed wants to start adding extra doubt to that outlook then tomorrow’s Fed meeting is the time to do it. If that happens watch for a sharp leg lower in stocks, gold, and a run higher in the USD sending EURUSD lower.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

*Any opinions made in this material are personal to the author and do not reflect the opinions of HYCM. This material is considered a marketing communication and should not be construed as containing investment advice or an investment recommendation, or an offer of or solicitation for any transactions in financial instruments. Past performance is not a guarantee of or prediction of future performance. HYCM does not take into account your personal investment objectives or financial situation. HYCM makes no representation and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast, or other information supplied by an employee of HYCM, a third party, or otherwise. Without the approval of HYCM, reproduction or redistribution of this information isn’t permitted.

20221213