“FOMC’s Forward Guidance” – Macro Tides Weekly Technical Review January 26th 2022

Macro Tides – “FOMC’s Forward Guidance”

The FOMC believes that Forward Guidance is an important policy tool and will use the January 26 meeting and Chair Powell’s press conference to accomplish a number of goals. The FOMC will signal that the FOMC will increase the federal funds rate at the March 16 meeting. Signaling doesn’t mean the FOMC statement or Chair Powell will explicitly state that the FOMC will raise the federal funds rate but the message will be clear. Chair Powell will discuss how the Omicron variant has depressed economic activity and represents a downside risk so the FOMC will be data dependent. This is why a ‘surprise’ hike at the January 26 meeting is unlikely.

Concern that the FOMC will increase the federal funds rate by 0.50% at the March meeting arose after Bill Ackman suggested the FOMC should in a series of Tweets. “While it has become conventional wisdom that the FOMC will raise rates 3 to 4 times this year to mitigate inflation, the market expects 25 bp increments. The unresolved elephant in the room is the loss of the Fed’s perceived credibility as an inflation fighter and whether 3 to 4 would therefore be enough. The FOMC could work to restore its credibility with an initial 50 bps surprise move to shock and awe the market, which will demonstrate its resolve on inflation. The FOMC is losing the inflation battle and is behind where it needs to be, with painful economic consequences for the most vulnerable. A 50 bp initial move would have the reflexive effect of reducing inflation expectations, which would moderate the need for more aggressive and economically painful steps in the future. Just a thought.”

In recent months I have discussed how the FOMC needed to move more aggressively to restore some level of credibility after being completely wrong about inflation in 2021. In the January 17 Weekly Technical Review I noted that financial markets were underestimating how the FOMC was likely to respond to the surge in inflation. “Powell described inflation as a ‘severe threat’ and most people when confronted by a severe threat don’t react moderately. The FOMC is likely to move more aggressively than the markets expect.” While it is certainly possible that the FOMC increases the funds rate by 0.50% at the March meeting, there are reasons why they won’t. The FOMC realizes that it misread inflation last year but a 0.50% increase in the funds rate would suggest the FOMC is panicking. That’s not a good look. Instead, FOMC governors and district presidents will use every speech to speak with one voice and say the FOMC will do whatever it takes to bring inflation down. Chair Powell has already said, “If we see inflation persisting at high levels longer than expected, then if we have to raise interest more over time, we will. We will use our tools to get inflation back.” The FOMC will use speeches to convince markets that the FOMC is serious as part of its forward guidance.

One of the primary purposes of forward guidance is to avoid upsetting the financial markets. The notion that the FOMC would raise the funds rate by 0.50% to shock and awe the markets is counter to the point of forward guidance. As noted in the January 17 WTR, “By front loading rate increases by raising the funds rate in March, May, and June, the FOMC can lower the risk of staying behind the curve and ultimately being forced to raise rates too much in the second half of 2022 and first half of 2023 to play catch up.” The FOMC would then be able to use the March meeting to prepare markets for a second increase at the May meeting, and use the May meeting to set up the third increase at the June 15 meeting. Actions speak louder than words and moving at 3 consecutive meetings the FOMC will prove the FOMC’s resolve without having to shock markets.

The FOMC increased the taper from $15 billion a month to $30 billion at the December meeting which would end its monthly purchases by the end of March. There is a chance the FOMC could announce at the January 26 meeting that it is stopping its QE immediately. There would likely be a short lived knee jerk sell off in the stock market but it would quickly dawn on investors that ending QE immediately or in March is not that big of a deal. By ending QE immediately the FOMC would show through its actions that it is committed to bringing inflation down.

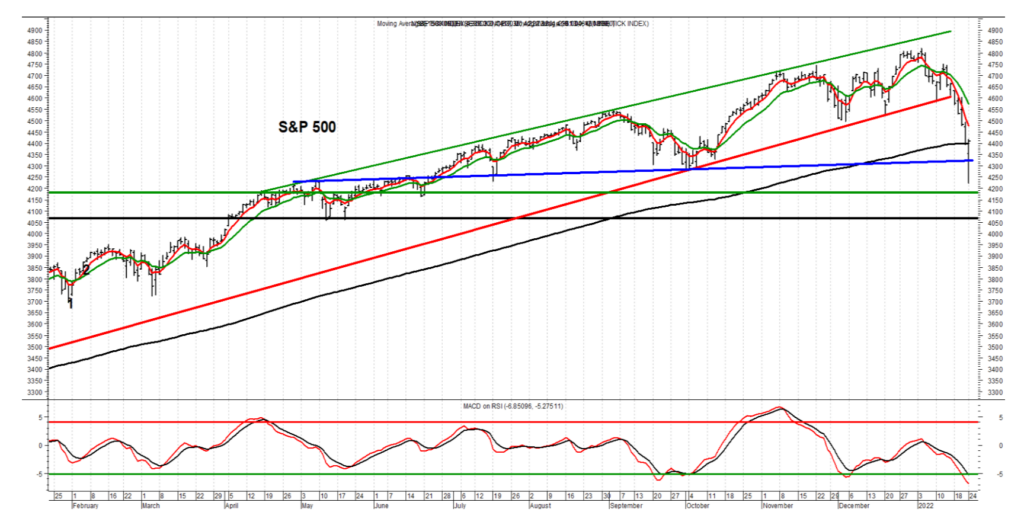

Stocks

As discussed with Blake Morrow in December, The expectation was that the S&P 500 would rally above 4800 in January and then experience a decline of -10% to -15%. On Monday January 24 the S&P 500 was down -10.0% from its high, while the Russell 200 was off by -20%, and the Nasdaq 100 was -18.3% below its peak.

Is the bottom in?

Will there be a lower low?

What does the price pattern in the S&P 500 suggest?

Treasury Yields

This is from the January 10 WTR, “This suggests that the 10-year may dip in the near term and then push above 1.808% to establish that positive divergence. If the 10-year climbs to 1.908% while it’s recording a positive divergence, a short term high could occur and signal that a decline in the 10-year yield was likely. The red horizontal line on the 30-year chart is at 2.23% so the 30- year may test this level as the 10-year is nearing 1.908%.” The 10-year dipped from 1.808% to 1.706% before rising to 1.874%.

Have Treasury yields peaked, or will the 10-year push above 2.0%?

Dollar

In December and in my weekly conversation with Blake Morrow, the Dollar was expected to drop below 95.51 before a rally would take hold. That’s exactly what transpired

Will the Dollar rally to a higher high?

Or is this rally just a bounce within the context of a larger decline?

Gold

Gold has been forecast to rally above $1815 and $1835. So far so good.

Can it rally to $1885 or even $1910?

Check out MacroTides.com to learn more. If you would like a complimentary issue send an email to JimWelshMacro@gmail.com

Macrotides.com

jimwelshmacro@gmail.com

20220126