Expectations, Implications and Possible Impacts on the Market

Expectations, Implications and Possible Impacts on the Market

Written by Michele ‘Mish’ Schneider

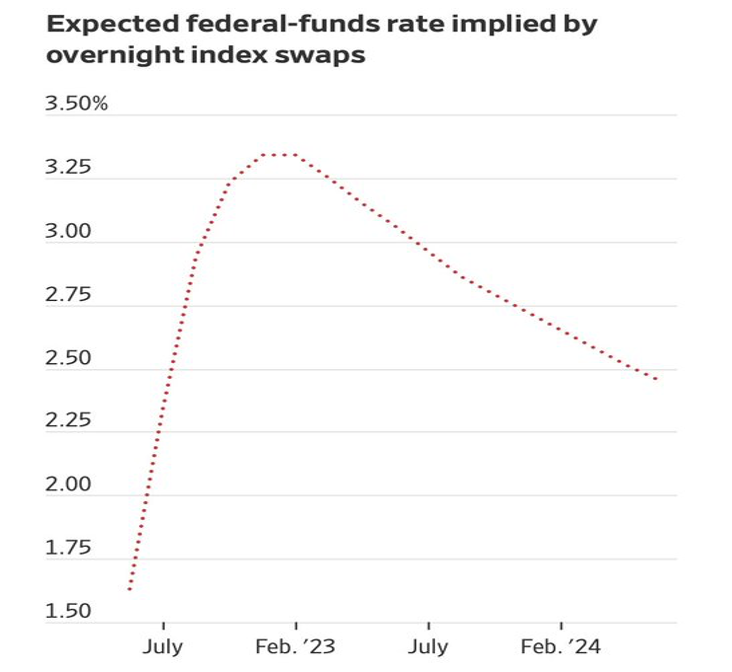

The chart posted is all about expectations.

Regardless of the talk on the new and stretched definition of recession departing from the textbook definition, investors believe that the Fed Funds rate is close to peaking and will begin to decline into 2023 and 2024.

Incidentally, I wrote a Daily on June 28th addressing this topic. I do remind readers of the textbook definition. I also remind readers why one could stretch the definition by observing this:

“Granny Retail (XRT) is not bullish, but she is holding steady and still taking money out of her purse. For the middle class, upper-middle-class, and wealthier folks, luxury vacations due to pent-up demand are still in style, and for many hard-working Americans, her purse strings are being spent out of necessity for items like food.”

Jerome Powell quietly stated that this week’s meeting could see a 50 bps raise rather than the 86% consensus it will be 75 bps. Furthermore he said that he expects to be less aggressive going forward.

However, will 3% yields or even 3.25% be enough to stave off inflation?

And, what will happen to the market even if inflation has plateued rather than peaked?

Why won’t anyone say “stagflation”, the most accurate term to describe the current economic macro?

Over the weeked I included 6 logical reasons to support why stagflation is a word that could tell investors where to put money.

If one follows the logical path we can assume a few things:

- 1. Yields remaining around 3% will not impact a 9.1% inflation rate

- 2. A weaker dollar will not help reduce inflation

- 3. With nary a recession (strong labor, ok housing market) nor economic growth (earnings mixed, reduction in corporate spending) in the near future, stagflation-a word rarely used, is the economic theme

- 4. The war in Russia-Ukraine is not ending

- 5. Oil supply remains low

- 6. China, still somewhat asleep, has yet to emerge hungry for raw materials.

Hence, we watch a few key indicators this week.

First, watch the yields and the high grade plus high yield bonds. (LQD red byt still in good shape.) (HYG even stronger than LQD, which makes sense given how many tech companies will report earnings).

If LQD and HYG remains firm that suggests more risk on.

Secondly, watch the consumer discretionary sectors. We need to see the consumers stay in the game. To date, Granny Retail XRT is off the highs yet holding above the key 200-week moving average.

Watch the dollar and the gold market-if gold continues to hold the major multiyear support, then we see a big gold rally coming.

Finally, watch the oil and energy market. Should crude oil join natural gas in a new bull run-commodities will soar while equities will suffer.

Putting this all together, the market is in a trading range. The yields are not expected to go much higher. Commodities are in support zones and one catalyst-geopoliticall or environmentally can take prices way higher.

Consumers are still out there. Housing has softenend but hardly collpased. And talk about new definitions, the labor market is strong while job openings are high and folks continue to quit their jobs.

What does that sound like to you? Seriously. We want to know.

Recession is pointless to debate, even the textbook definition could be manipulated (nominal GDP or real GDP).

We will also watch earnings for more indications.

ETF Summary

S&P 500 (SPY) 403 big resistance 390 support

Russell 2000 (IWM) 176.50 support to hold and now must take out 182.50

Dow (DIA) 322-323 resistance 316 support

Nasdaq (QQQ) 308 big resistance 293 support

KRE (Regional Banks) 60 key support

SMH (Semiconductors) 221 support 230 resistance

IYT (Transportation) 221 support

IBB (Biotechnology) support 120

XRT (Retail) 62.90 pivotal or the 50-DMA

Click here for a FREE report on the best calendar range setups for July and the second 1/2 of 2022

Get your copy of “Plant Your Money Tree: A Guide to Growing Your Wealth”

and a special bonus here

Mish in the Media

BNN Bloomberg 7-22-22

Coast to Coast With Neil Cavuto Fox Business 07-22-22

20220726