ECB: The Latest Bank to Take a Dovish Tilt

ECB: The Latest Bank to Take a Dovish Tilt

The ECB’s decision to hike rates by 75bps was expected, but the communication from the meeting was considered dovish as hints of a slowing rate hikes were read into some of the details. The first point that traders looked at was the change in the wording of the statement. The previous statement read, “the Governing Council took today’s decision, and expects to raise interest rates further”. In contrast, previously the text had read, “over the next several meeting the Governing Council expects to raise interest rates further”. The omission of the word ‘several’ led investors to believe that the ECB may be slowing the path of rates going forward.

The press conference & sources

Remember when you are trading the ECB statement you also have to allow for the Press Conference and sources which come out later. In the Press Conference, Christine Lagarde said that the APP reduction (Quantitative Tightening) would be discussed in December’s meeting. This was seen as more dovish that this would not be started until 2023 now. Sources afterwards said that the ECB does not start to plan to set the QT date in December, pushing the start of QT even further back. In a seeming contradiction to the statement sources also said that the ECB did not mean to imply a slower rate of hiking with ‘progress’ remark and played down the removal of the word ‘several’ from the guidance on further rate hikes. Given the decision was not unanimous, with 3 voting for only a 50bops hike, it seems probable that there was something in the decision to keep both the hawks and the doves happy. However, the market reaction the day after was clear. A lower peak rate is expected.

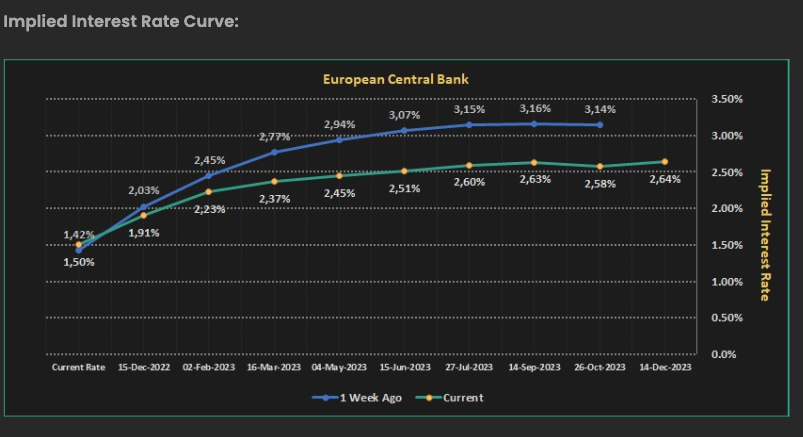

The peak rate

At the next interest rate decision a 50bps hike is expected. However, the terminal rate fell sharply with a rate now expected to be at 2.64% vs a previous high of 3.16%. See the financial source implied interest rate tracker below.

This confirms the ECB is moving to look at growth metrics more carefully and will be slightly more hesitant to hike rates aggressively. This does not really open up an obvious trade, but if the Fed gradually takes a slower approach to hiking then some EURUSD upside would be the logical outworking.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

*Any opinions made in this material are personal to the author and do not reflect the opinions of HYCM. This material is considered a marketing communication and should not be construed as containing investment advice or an investment recommendation, or an offer of or solicitation for any transactions in financial instruments. Past performance is not a guarantee of or prediction of future performance. HYCM does not take into account your personal investment objectives or financial situation. HYCM makes no representation and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast, or other information supplied by an employee of HYCM, a third party, or otherwise. Without the approval of HYCM, reproduction or redistribution of this information isn’t permitted.

20221101