Blue Line – Morning Express June 11th, 2021

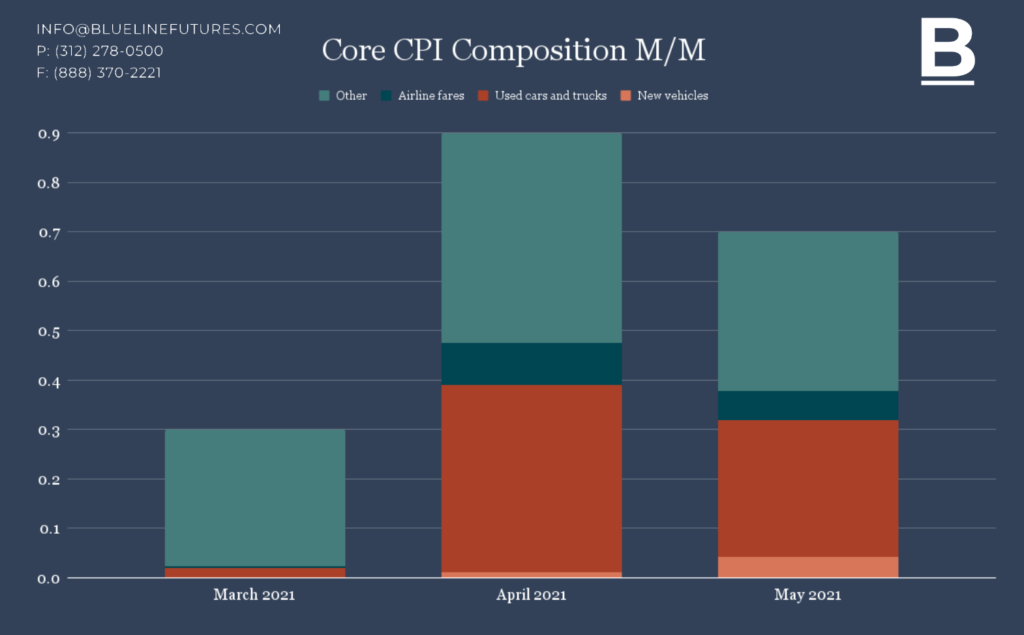

Yesterday’s inflation data was everything we anticipated. Not because we called for a hot read, but because the bond market is pricing in peak inflation. Core CPI for May was +3.8% YoY and +0.7% MoM, handily topping expectations. However, transitory factors such as the price of used cars and airfares are significantly impacting the rise. In fact, more than half the rise from April to May can be attributed to used cars and trucks, new vehicles, and airfares. Although there is still room for airfares to reach pre-pandemic levels, it is our belief they cannot continue to carry the rise in inflation from month to month at this pace and the bond market agrees with us. The yield of the U.S. 10-year reached a low of 1.428% overnight, the lowest since March 3rd, but one component is holding markets back from an all-out risk-on rally: U.S. Dollar strength.

A leading factor in U.S. Dollar strength is a bipartisan infrastructure agreement in Washington last night. The group agreed on a plan that includes only $579 billion in new spending, costing $974 billion over five years and $1.2 trillion over eight years. Whereas equity markets are finding solace in deal, the U.S. Dollar strength has strengthened on the bipartisanship and less spending which has eroded yesterday’s commodity gains. Separately, Reuters reported “infrastructure-related transportation bills moving through Congress” equaling $547 billion and $78 billion.

The Euro is also lower on the session for what we believe to be Euro-centric reasons. Remember, currencies must be paired against another currency. It is not just U.S. Dollar strength on its own, it is relevant to a pair. The ECB raised growth and inflation projections but reaffirmed their pledge for faster bond buying at its policy meeting yesterday. At the end of the day, the U.S. Dollar weakened on CPI’s transitory factors, but it has not been uncommon for markets to digest central bank news over 24 hours. The Euro is down nearly 0.5% today despite the German Bundesbank also raising forecasts. The British Pound is also weaker against the U.S. Dollar, although U.K. GDP edged beat by one tenth this morning, a deluge of economic data all missed. Commodity currencies, the Aussie and Canadian, are also lower.

U.S. Dollar strength is directly impacting commodities, both Crude Oil and Gold are about 1% off overnight highs. Traders must keep a close pulse on the energy space through today as Iran nuclear talks are set to restart over the weekend. Yesterday, Crude whipsawed violently on poor reporting as headlines stated the U.S lifted sanctions on Iran. However, the U.S. only lifted sanctions on a handful of Iranian officials. This was in order to grease the wheels ahead of this weekend’s talks and comes after the U.S. Secretary of State side hundreds of sanctions on Iran will remain in place. Both the IEA and OPEC increased their demand outlook for 2022, but each anticipates added supply. Iran talks will prove a focal point for this narrative and traders must be prepared for a wild Sunday night reopen.

E-mini S&P (June) / NQ (June)

S&P, yesterday’s close: Settled at 4238, up 19.50

NQ, yesterday’s close: Settled at 13,959.75, up 145.50

Technicals: We have a breakout in the S&P on our hands, but this must be confirmed on a weekly closing basis. With quadruple witching next Friday, such a breakout alludes to a potential melt-up to the 4300 region, but again, we must see this confirmed through today. Whereas the S&P has chewed through rare major four-star resistance and now must hold above, the NQ faces such resistance overhead at … Sign up for a Free Trial at Blue Line Futures to have our entire fundamental and technical outlook, actionable bias, and proprietary levels for the markets you trade emailed each morning.

Crude Oil (July)

Yesterday’s close: Settled at 70.29, up 0.33

Technicals: Crude’s whipsaw yesterday is helping to form a higher floor of support against Tuesday’s low. We do believe that Crude is heading higher and given the elevated floor of support, we can now define a better range of risk in order to increase our Bullish/Neutral Bias to an outright Bullish Bias; while above major three-star support at … Sign up for a Free Trial at Blue Line Futures to have our entire fundamental and technical outlook, actionable bias, and proprietary levels for the markets you trade emailed each morning.

Gold (August) / Silver (July)

Gold, yesterday’s close: Settled at 1896.4, up 0.9

Silver, yesterday’s close: Settled at 28.031, up 0.029

Technicals: The rise in the U.S Dollar has hampered Gold, but Silver is clinging to a gap higher from yesterday’s settlement in a very constructive manner. The only problem, Silver’s overnight high failed directly in front of at a trend line from the May 18th high and our major three-star resistance at 28.47-28.55. Silver has still been able to cling to some of these post-settlement gains and the session low is 28.09 as it climbs back. However, shifting dynamics in Gold after yesterday’s deluge of fundamentals is not uncommon and Gold has bled lower ever since the European open. We are hedging our risk in Gold by buying a put structures in the 30-year Bond, which has certainly squeezed shorts. Feel free to contact our trade desk at 312-278-0500 today or email info@bluelinefutures.com to find out the structure. Gold failed at strong resistance at 1903-1906.9 with a high of 1906.2. It is now decisively back below our Pivot, the recurring 1894.5-1896, and working through first key support at 1887.3. We have major three-star support aligning multiple levels, including a trendline from … Sign up for a Free Trial at Blue Line Futures to have our entire fundamental and technical outlook, actionable bias, and proprietary levels for the markets you trade emailed each morning.

You can sign up for a free trial here: https://www.bluelinefutures.com/free-trial

https://www.bluelinefutures.com