August Central Bank Overview

August Central Bank Overview

Major central bank rundown

It’s time for your central bank catch up. The link to the latest statement is at the bottom of each section, so just click there to read the bank’s central statement. Remember, there is no substitute for actually reading a central bank statement yourself and it will almost certainly be of great benefit to your trading. However, here is a summary analysis of the position of the major central banks.

Reserve Bank of Australia, Governor Phillip Lowe, 1.35%, Meets 02 August

RBA: A neutral 50 bps hike

In July the RBA hiked by 50 bps to 1.35% as anticipated. Just before the event, short-term interest rate markets saw an 80% chance of a 50bps hike, but economists were expecting a 50bps hike. So, there were no major surprises with the print. The ‘as expected’ feel echoed within the RBA’s statement with the RBA signalling everything that you would expect.

Domestic inflation was seen to be high, but not as high in Australia as in other countries. The latest inflation print is 5.1%y/y which is pretty much in the middle of the pack. The US and the UK are closer to 10% and the Swiss and Japan still have some of the lowest inflation readings around 2-3%. The RBA projects inflation to peak this year and then fall back towards 2-3%. They saw global supply chain issues being the main driver of inflation at this stage.

Unemployment is at a 50-year low in Australia at 3.9% in May and the RBA sees this tight labour market as encouraging higher prices. The RBA anticipates a lift in wages as job vacancies and job ads are both at a very high level. One interesting point was that the Board was unsure about how households would be responding from here. It recognises that although household budgets are under pressure from higher prices and higher interest rates housing prices have also declined. The RBA stated that household savings rates remain higher than it was before the pandemic and many households have built up large financial buffers and are benefiting from stronger income growth. So the RBA will be watching household data closer.

AUDUSD levels ahead of this week’s meeting

The bottom line is that the RBA still expects to take ‘further steps’ in the process of normalising monetary conditions (ex: keep hiking rates). This should keep the AUDUSD supported over the medium term as long as China’s outlook remains stable. However, with the Federal Reserve changing tact this week, will the RBA also switch to a more data-dependent outlook? Key AUDUSD levels are marked below:

Read the full RBA statement here

European Central Bank, President Christine Lagarde, 0.00%, Meets 22 September

The inflation challenge is growing

Slowing eurozone growth is continuing to weigh on the euro and the risk of fragmentation from highly indebted countries like Italy and Greece still remains. The ECB delivered a surprise 50 bps rate hike at their last meeting, but the growth concerns are more focused on the eurozone than an extra rate hike. This was particularly due to the fact that the ECB made it clear that the extra hike was to do with front-loading the hikes not raising expectations of a higher terminal rate. GDP growth at the time of writing is at 2.7% and that is lower than the UK’s, Australia’s (3.3%) and Canada’s (3.1%) GDP growth y/y.

However, the ECB is facing eurozone headline inflation of 8.1% and core inflation of 3.8%. Of the major countries, only the UK’s inflation is higher. The ECB is determined to act to get it under control which is why the hike came in at 50bps. Yet, many analysts project that the ECB will hit the brakes on hiking rates once slowing growth really bites the eurozone.

The new anti-fragmentation tool disappoints

The announcement of the new anti-fragmentation tool (Transmission Protection Instrument) did not lift the euro as the eligibility criteria still may make it hard for some of the more vulnerable eurozone countries to qualify. Since the meeting, the BTP/Bund spread has kept rising, so fragmentation risk is still present.

The EUR has a weak bearish bias, but the risk is further falls if the growth outlook worsens. The ECB are on a ‘meeting by meeting’ basis now, so expect data to potentially move the euro more in the coming weeks. This is even more so the case with the Fed also on a meeting-by-meeting basis. Watch out for EURUSD volatility on both growth and inflation data from the eurozone and the US.

You can read the full ECB statement here

Read the ECB press conference here

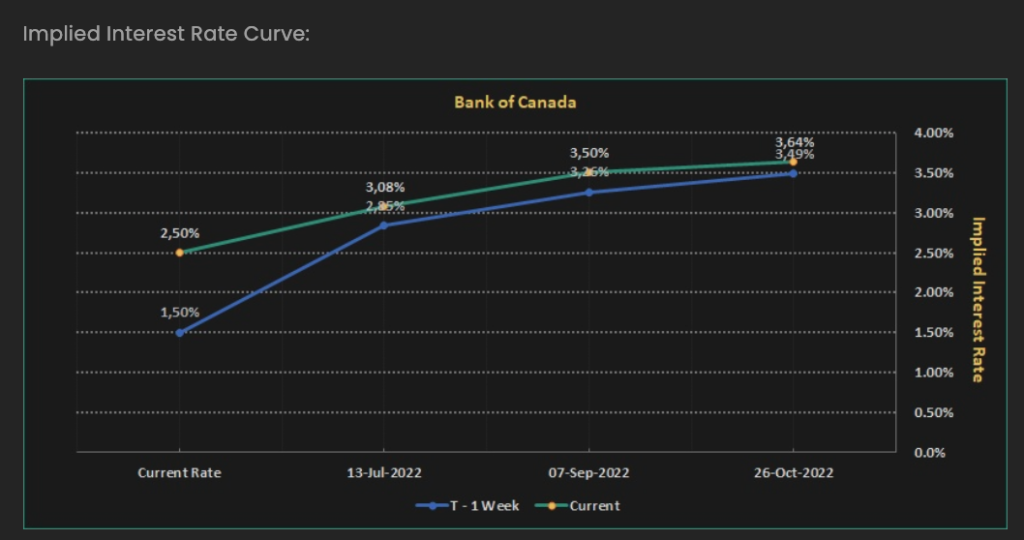

Bank of Canada, Governor Tiff Macklem, 2.50%, Meets 07 September

The Bank of Canada has front-loaded some of its interest rate hikes at the last BoC meeting in the middle of July hiking by a surprise 100bps. In June’s meeting, the BoC made a bullish twist as inflation pressure became more pronounced and the BoC stated that ‘pervasive’ input prices were making their way into the CPI data. See here.

Inflation pressures run the risk of becoming costly to remedy

The BoC stated that, ‘More than half of the components that make up the CPI are now rising by more than 5%. With this broadening of price pressures, the Bank’s core measures of inflation have moved up to between 3.9% and 5.4%’. Inflation has crept up significantly since earlier in the year and the BoC now sees a real risk of a wage price spiral. The BoC’s exact words were that there is now an increased risk of elevated inflation becoming entrenched in ‘price and wage setting’. The BoC goes on to say that the economic impact of ‘restoring price stability’ will be higher if that happens.

The BoC’s actions explained

In simple terms, the BoC is trying to act quickly and curb inflation before a wage price spiral clearly takes effect. This is why it surprised economists and short-term interest rate markets with a 100 bps rate hike. At the end of the week of the July 13 meeting, Short Term Interest Rate markets increased expectations for even higher rates going forward with a rate of 3.64% for October 2022. See here that difference from the end of that week from the Financial Source Terminal:

The takeaway

This means that the CAD may find buyers on deep dips, but a lot of the expectations for higher interest rates are now well priced in. So, the best opportunity would most likely come from signs of falling inflation or indications the BoC is looking to be less aggressive in its rate hiking policy. Any drops in the labour market data out this month could provide good opportunities to short CADJPY.

You can read the full BoC statement here

Federal Reserve, Chair: Jerome Powell, 2.375%. Meets 21 September

USD: Peak Bullishness

Federal Reserve: Kept to expectations

Heading into the last Fed meeting we were expecting the key focus to be on growth and this was what Giles Coghlan, Chief Currency Analyst, shared with Benzinga in his interview just before the FOMC meeting. You can also check out the USDJPY sell outlook that looked very attractive from a seasonal point of view. The first line of the rate statement recognised that growth was slowing when it stated that, ‘recent indicators of spending and production have softened’. However, there was not much of a reaction to this statement as it also said that the committee ‘anticipates that ongoing increases in the target range will be appropriate’.

The press conference saw the moves into USD selling

It was the press conference where Jerome Powell showed the shift. The meetings would now be conducted on a ‘meeting by meeting basis’ to consider incoming data. Ok, it seems innocuous enough of a statement, but the context is key. In June there were signs of a slowing US economy, but the Fed stressed tackling inflation. Now the Fed recognises a slowing economy and is being more ‘data dependent’. Translated this means that the Fed will consider the pace of hikes and terminal rate depending on how the US economy fares. The day after the Fed meeting the US entered a technical recession with two consecutive quarters of contracting GDP numbers.

This was the extra fuel that USD bears needed as the more signs of slowing growth then the more likely the Fed is to be less aggressive in hiking rates. This will mean that the USD can continue to retrace some of the recent gains.

The takeaway

The main takeaway from the meeting is that US growth metrics are going to be very important for the USD going forward. This week we have US ISM services and manufacturing PMI prints coming up. If they surprise to the downside then expect more USD weakness. One market that has really gained from the drop in the USD has been the USDJPY as US 10-year yields pushed lower through the 2.75% level.

Read the full Fed statement here

Bank of England, Governor Andrew Bailey, 1.25%, Meets 04 August

BoE takes another dovish hike to 1.25%

Inflation and growth a problem

The problem that the BoE has, alongside many other central banks, is how to control inflation without slowing growth. Inflation is now expected to move above double digits this year. Future energy prices are set to gain again with Ofgem’s utility price caps set to be substantially higher when they are reset in October 2022. This is seen as an upside risk for inflation as energy prices are a quick proxy for inflation expectations.

In its June meeting, the Bank of England hiked rates by 25 bps to 1.25% last week in a move that was widely anticipated. Headline inflation is expected to move into double digits and growth is expected to turn negative in 2023. This stagflationary environment has been weighing on the GBP for some time as the BoE starts to push back against aggressive STIR market rate hike pricing. The BoE dropped its guidance from May on the future path of tightening. In May’s statement, it had said ‘some degree of future tightening in monetary policy may still be appropriate in the coming months’. By dropping this it is signalling that it doesn’t expect to keep tightening. However, the exact path will depend on the pace of inflation.

Inflation, inflation, inflation

The BoE thinks it can get on top of inflation with its current hiking cycle. The BoE stated that ‘CPI inflation was projected to fall to a little above the 2% target in two years’ time, largely reflecting the waning influence of external factors’. In other words, the cooling of the economy and high inflation will be impacted by the rise in interest rates implemented by the Bank of England.

Is a slower path now ahead for the BoE?

After the meeting markets priced in six 25 bps rate hikes as opposed to seven 25 bps rate hikes prior to the meeting. This is still steeper than the BoE is indicating, but the exact path ahead will be dependent on upcoming inflation data. If inflation continues to rise then that means more aggressive pricing can be expected.

Consumer confidence falls

Higher taxation, rising living costs, and soaring energy bills have all meant a squeeze on real household disposable incomes. Unsurprisingly the BoE stated that consumer confidence has fallen. The BoE expects this to now drag on growth which has been recognised by the committee. It did this by revising the medium-term growth outlook lower. The 2023 growth was revised down (and negative) from 1.25% and is now -0.25%. This is what sunk the GBP post the BoE. This means the BoE may now need to pause the hiking cycle around the summertime and potentially cut rates in 2023.

The BoE meets this week

This week the BoE meeting is on Thursday and markets will be looking to see if the BoE brings forward its 2023 recession projection. Investors will be expecting another dovish hike from the BoE this week on Thursday with STIR markets pricing in an 87% chance of a 50 bps hike.

You can read the full BoE policy report here

Swiss National Bank, Chair: Thomas Jordan, -0.25%, Meets September 22

The latest SNB decision was a shock one. For years the SNB has been battling against deflation and trying to keep the CHF from strengthening. No economists going into the SNB meeting expected the SNB to move on rates. This was because no one thought the SNB would hike rates before the ECB did. However, the central bank announced on June 16 that, the SNB is tightening its monetary policy and is raising the SNB policy rate and the interest rate on sight deposits at the SNB by half a percentage point to −0.25% to counter increased inflationary pressure’. The move by the SNB before the ECB is a significant shift. The SNB no longer has the reference to the CHF being ‘highly valued’ and the need for FX intervention to address it. This hike was all about one thing, fighting inflation.

SNB gets tough on inflation

The SNB acted to combat spreading inflation in a bid to keep inflation out of Swiss goods and services. The second line of the SNB’s statement stated, ‘the tighter monetary policy is aimed at preventing inflation from spreading more broadly to goods and services in Switzerland’. Linked to this is the idea that the Swiss, like the RBA and the BoE and the Fed, does not want to see a ‘wage-price’ spiral. Giles Coghlan, Chief Currency Analyst, was speaking about this on the Times Radio and you can listen to his segment here which starts at around 08:40.

Although the SNB revised its inflation forecast higher it still sees it dropping around the middle of next year.

Inflation tackler

All of this means the SNB is tackling inflation on the front foot and it doesn’t want inflation to go into wages. With inflation at 2.9% in May the SNB is trying to slow that down as quickly as possible. This does open up a USDCHF sell bias for now. If the US starts to show falling inflation then USDCHF could move sharply lower. Look at the large monthly reversal candle on the USDCHF.

You can read the full SNB statement here

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, Meets 22 September

There has been a shift in the pressure for the BoJ, but not its policy. The Yen has seen a serious amount of depreciation this year as the yield differentials between the JGB’s and US treasuries have kept the JPY weak. The weakness in the JPY has been amplified by the rise in oil prices. See here for four things to know when trading the JPY. There has also been growing speculation that the BoJ may have to exit its very loose monetary policy stance as the weakness in the yen begins to hurt the Japanese domestic market. However, in the July meeting the BoJ tasted that, ‘it also expects short- and long-term policy interest rates to remain at their present or lower levels’. So, interest rates remain at -0.10%. The Yield Curve Control (YCC) was maintained to target 10-year JGB yields at around 0.0% and the vote on YCC was made by 8-1 votes with the only dissenter being Mr Katoaka once again.

The BoJ looks vulnerable to a change of direction

Going into the last two BoJ meetings the obvious concern was the JPY weakness. JPY weakness has been extreme recently as the US10Y yields kept pushing higher on US inflation fears. However, the key aspect of this is whether there will be action from the BoJ. For years Japan has struggled to see any inflation, so with inflation rising around the world, it was interesting to see that the BoJ now does expect consumer inflation to rise. It also notes that short-term inflation expectations have risen. However, this is mainly attributed to energy prices and commodity gains. Both of these factors are expected to fade and medium-term inflation is expected to fall back lower again.

The excessive FX moves are now a risk to the BoJ

One standout factor to look out for is any FX intervention from Japan. The BoJ and the Japanese Gov’t let markets know that they are concerned about the JPY weakness. So, at some point, there could be a large amount of JPY strength if the Japanese Gov’t suddenly intervenes. This means traders should be cautious about staying short of the JPY as a sharp retracement could occur unannounced. The fall of US yields last week on expectations of a less aggressive Fed should help the USDJPY pair to drift lower in now medium term.

You can read the full BoJ statement here

Reserve Bank of New Zealand, Governor Adrian Orr, 2.50%, Meets 17 August

RBNZ: Slowing growth ahead?

Heading into the last RBNZ meeting short-term interest rate markets were pricing in a 100% chance of a 50 bps rate hike and a 67% chance of a 75 bps rate hike. The RBNZ delivered that 50 bps rate hike and affirmed the aggressive path of rate hikes from May’s meeting. As a reminder here is the RBNZ’s May projection is to raise the OCR rate (interest rate) to a level that brings consumer inflation down:

- * May projection for the OCR for Sep 2022 at 2.68%,

- * May projection for the OCR for June 2023 now at 3.88%,

- * May projection for the OCR for Sep 2023 now at 3.95%.

The RBNZ then saw the interest rate dropping in June 2025 to 3.5%. Although the decision was broadly in line with what was expected we did caution before the July 13 meeting that the main focus for the meeting was likely to be the future path of growth. This was especially after we noted a research piece from the Bank of New Zealand which projected that New Zealand could enter into a recession in 2023. The BNZ’s head of research warned that the latest ANZ Bank’s survey of business opinion was ‘littered with indicators that fit with our view that the economy is headed into recession’.

Slowing growth hints did make it into the July statement as the RBNZ said, ‘Members noted that while there are near-term upside risks to consumer price inflation, there are also medium-term downside risks to economic activity’. The main message from the RBNZ was that price pressures remain persistent enough to carry on with their rate hiking outlook from May. However, the RBNZ did note the downside risks.

The takeaway

This means that going forward any further signs of New Zealand’s economy slowing down could result in further expectations of the RBNZ recognising these downside risks. This could weaken the NZD. The latest business confidence data out last week showed that business confidence was not as bad as expected. So, if the RBA is more bearish on Tuesday watch for some AUDNZD selling.

You can read the full RBA statement here

HYCM clients can access the Seasonax product in order to analyse over 25,000 currency pairs, indices, commodities, as well as individual stocks. Please contact your account manager for a free trial. Certain products & services mentioned herein may or may not be available to all clients depending on which HYCM Capital Markets Group entity their trading account(s) adheres to.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

20220801