“A More Hawkish FOMC Message” – Macro Tides Weekly Technical Review November 1st 2021

Macro Tides – “A More Hawkish FOMC Message”

A More Hawkish FOMC Message

Markets have become conditioned to expect a Dovish FOMC statement after every meeting and for Chair Powell to reinforce an accommodative message during his press conference. This puts the FOMC in a bind when the time to be less dovish and accommodative arrives. We’re there.

The FOMC places a big emphasis on consumer’s inflation expectations as a good predictor of future inflation. The FOMC changed its policy framework in August 2020 when it adopted Average Inflation Targeting. By telling consumers that the FOMC won’t raise rates if inflation rises above 2.0% for a brief period of time, the FOMC hoped that low expectations would give way to higher inflation expectations. I think the FOMC has it backwards. Inflation expectations go up after consumers experience inflation when they fill up their gas tank, shop for food in a grocery store, and see prices increase for many of their favorite services. Consumers won’t expect higher inflation to go up, if that’s not their personal experience just because a group of academic economists tells them they will tolerate inflation above 2.0% for awhile. The notion that FOMC pronouncements could change consumer’s expectations seemed driven by hubris more than common sense.

At this point it’s immaterial whether inflation expectations are rising due a FOMC policy change or a Pandemic induced fiscal bacchanalian splurge coupled with a breakdown in supply chains globally. According to the Conference Board 1 year inflation expectations are the highest since 2008, and the 10-year Breakeven Rate has almost matched its high from 2006.

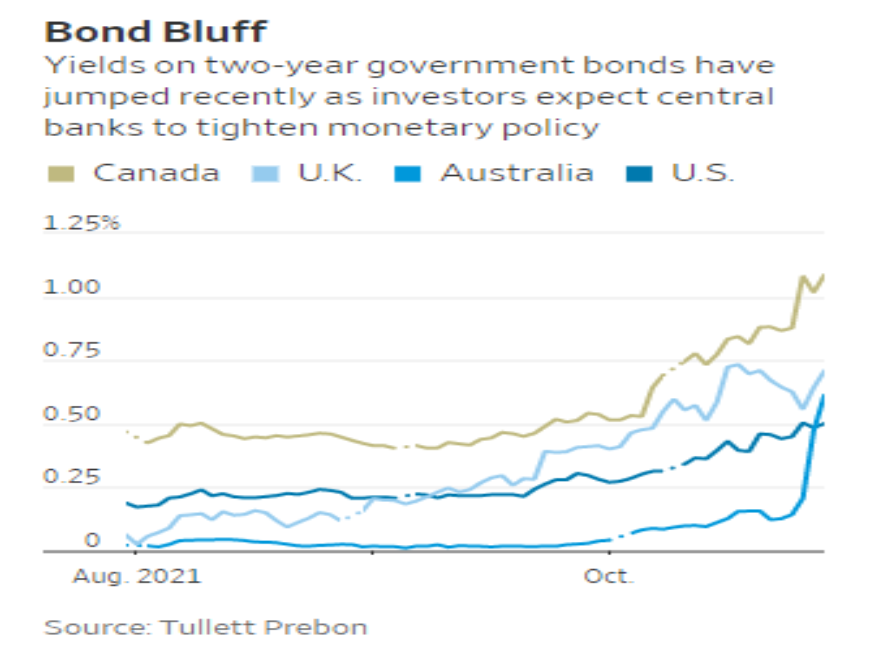

The drivers behind the surge in inflation in the US are global and central banks have started to change course. Last week the Bank of Canada decided to end its QE buying immediately. The BOC believes that tapering is unnecessary and decided to go cold turkey. On October 6 the Reserve Bank of New Zealand hiked its policy rate to 0.50%. The Bank of England indicated in early October that it may have to increase its policy rate sooner than expected since inflation is double its 2.0% target and headed higher.

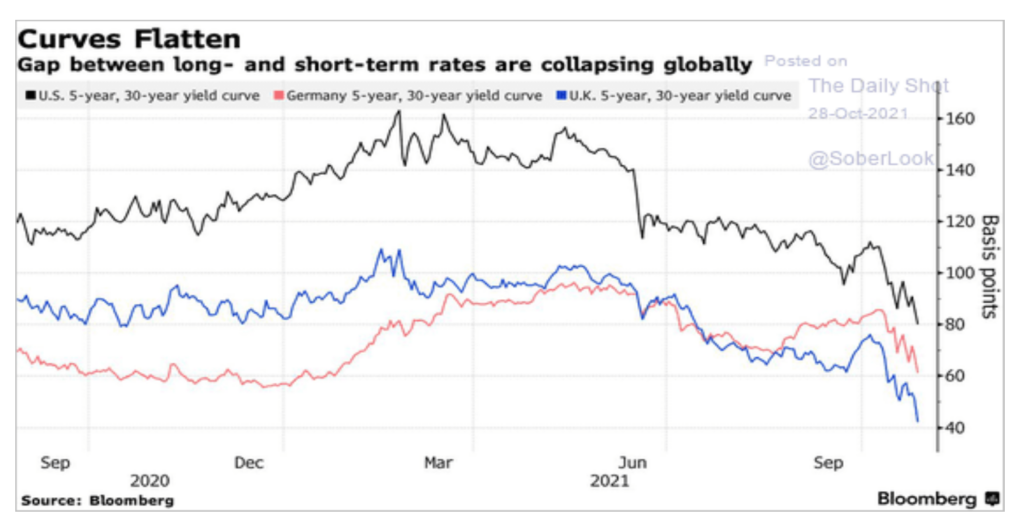

Government bond markets are responding to higher inflation and the change in the policy tilt by these major central banks. Short term rates have exploded higher in the past month as measured by the 2-year bond yield.

The increase in 2-year rates has caused spreads to narrow significantly in the last 4 weeks. Long term bond yields haven’t climbed as much as the 2-year yield which has also contributed to the narrowing. If longer term bond yields are falling in response to softer economic data in Q3, the global bond market is in for a rude awakening. The US economy is being held back by supply chain problems and unemployed workers’ unwillingness to go back to work.

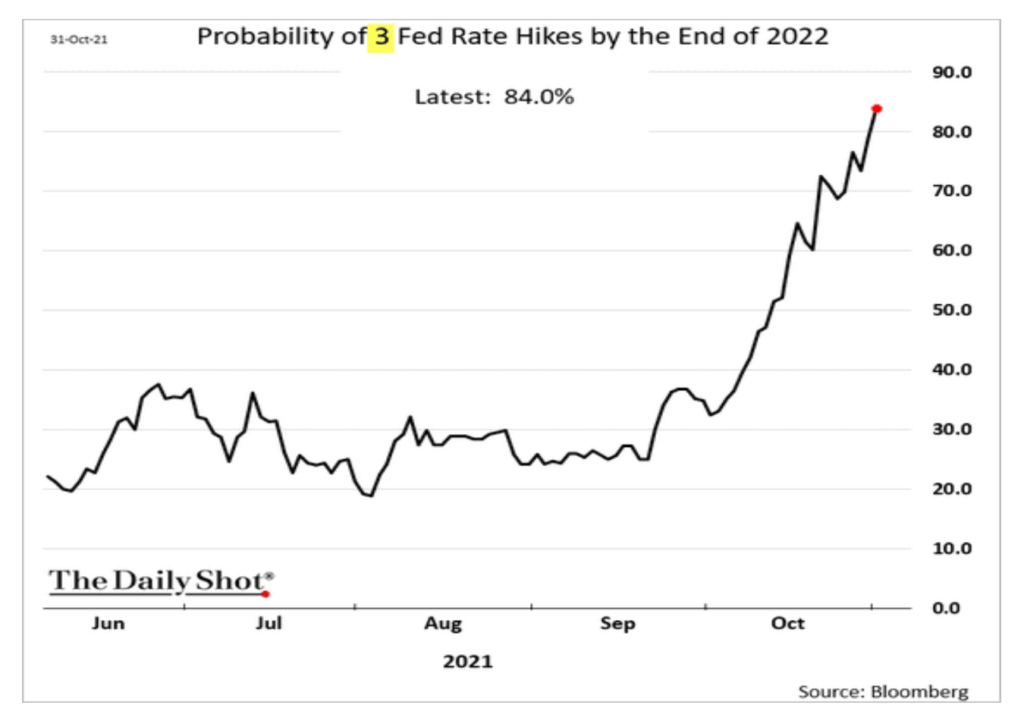

The short end of the Treasury market is pushing the 2- year Treasury yield aggressively higher and pricing in rate increases well before the FOMC’s dot plot which has indicated 2023 at the earliest. The federal funds futures market thinks the FOMC will raise the funds rate 3 times before the end of 2022!

The FOMC will have a less dovish statement and Chair Powell will emphasize that the FOMC has the tools to keep inflation in check and won’t hesitate to use them. Chair Powell will make it clear on November 3 that the FOMC won’t hike rates until the number of unemployed workers has dropped significantly. The FOMC won’t know until the second quarter whether Reverse Base Effects are bringing headline inflation down, supply chain problems are receding, wage growth is moderating as labor shortages fade, and if oil prices have stopped going up. As discussed in the November Macro Tides inflation is going to get worse in the next four months, but it seems like the federal funds futures market is way ahead of the FOMC.

Treasury Yields

| The expectation is that the highs in Treasury yield established in October are likely to last for awhile. This is an aggressive forecast since the long term trend in Treasury yields is up. As discussed last week the inter market divergence in October between the 10-year and the 30- year Treasury yield suggested yields could fall and so far they have. The October 21 Special Update suggested it was time to sell the remaining 35% of TBF which is the 1 to 1 inverse Treasury bond ETF at $16.83 after selling 65% at $16.84 on October 12. There is a chance the 30-year Treasury yield could dip below 1.85% before the counter trend rally is over. I will |

| attempt to reestablish the position in TBF since higher yields are likely to move up after this dip. |

Stocks

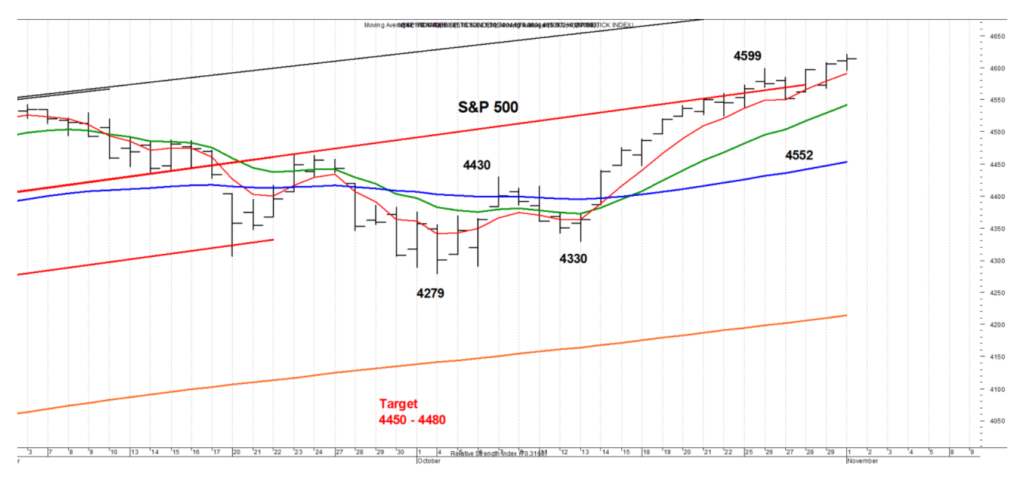

Last week I discussed two paths the S&P 500 might take and the S&P 500 appears to have confirmed the second pattern. “A second pattern would develop if the S&P 500 pulls back by 50 to 75 points (wave 4) and then rallies to a higher high (wave 5). This would change the existing pattern from a 3 wave up move to 5 waves up. This would pretty much eliminate the prospect of a decline below 4270. After 5 waves up the S&P 500 would have another pullback, but it would only be a retracement of the entire 5 wave rally from 4270 to whatever the high for wave 5 proves to be.” The S&P 500 fell 47 points from 4599 to 4552 which is a bit shallow but shallow declines have been a hallmark of this market. The S&P 500 quickly rallied to a new high, which can now be labeled wave 5. However, until the 5 day moving average (red) drops below the 13 day moving average (green) the trend is up. The 13 day MA closed at 4541 on November 1 and is climbing by 12 points a day.

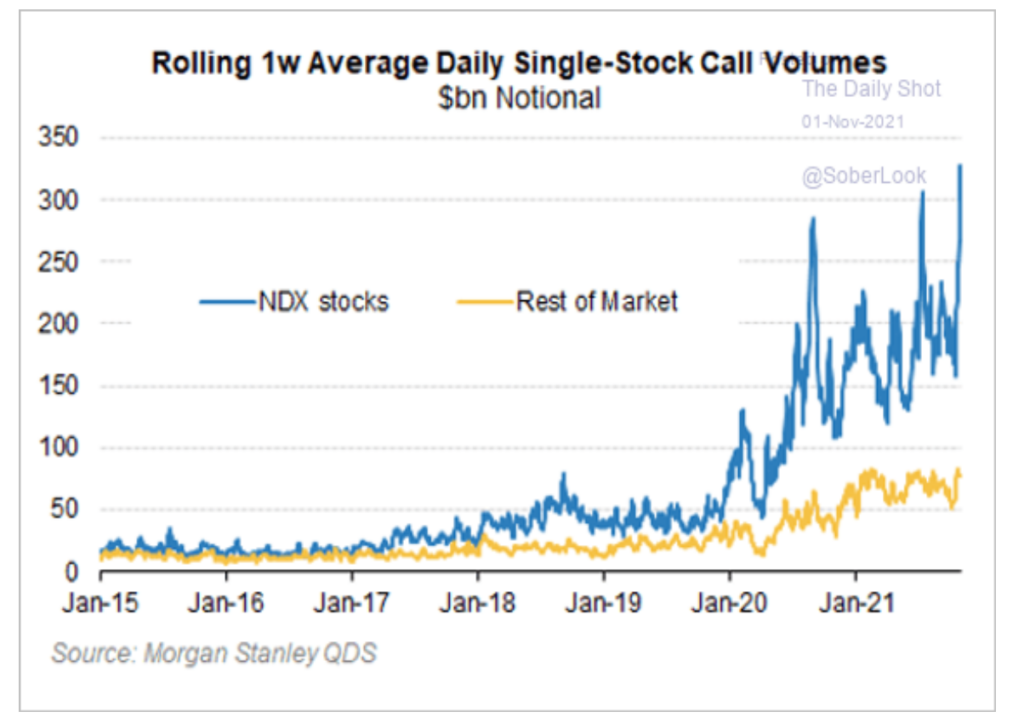

Short term Call Option traders have returned with a vengeance in the last 3 weeks, with the volume of Calls on Mega Cap stocks dwarfing Call option buying for the rest of the market. As discussed previously, this cohort likes to buy call options with an expiration of less than 2 weeks. A small investor may not be able to buy Amazon, Tesla, Microsoft, Facebook, or Apple, but they can afford an out-of the-money call option. This morning 35,000 Tesla call options were purchase at the $1200 strike prices when Tesla was trading at $1138. These options will expire on Friday November 5. This represents rampant speculation but the amount of money involved forces the dealer community to buy Tesla’s stock to hedge the short call option position. This is a self feeding loop that is pulling the market higher. To those ‘investing’ for extremely short time periods, nothing matters other than momentum.

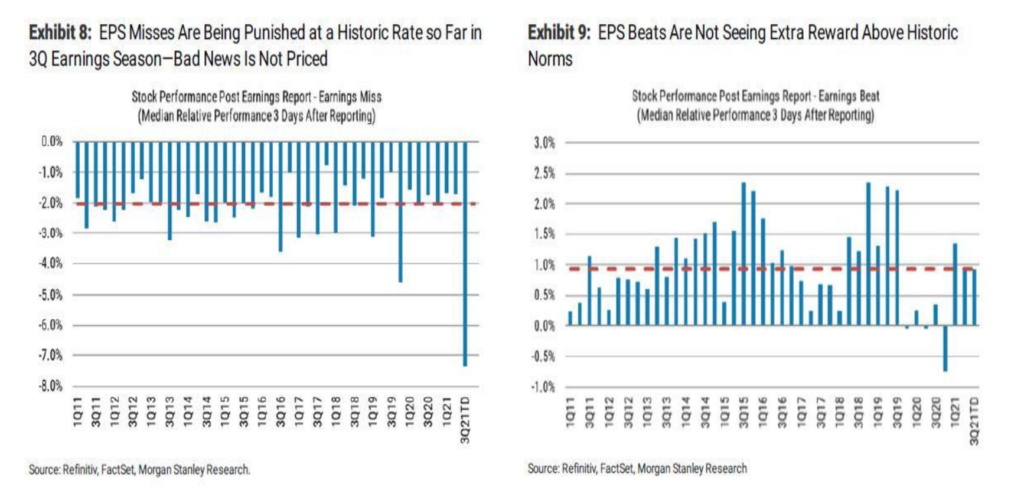

Good earnings aren’t getting the love they normally do and misses are getting spanked in the days after companies report earnings. Companies that miss fall 3.5 times as much as in the past (red dashed line left). Companies that beat have been going up less than they have in the last 9 years.

The Relative Strength of the Russell 2000 to the S&P 500 has languished since peaking in early March, as the Russell 2000 chopped around in a range between 2130 and 2360. The Russell 2000 closed today at 2358 and appears ready to finally breakout of the range. I will send a Special Update tomorrow if the Russell 2000 follows through to the upside. A confirmed breakout should be followed by at least an 8% rally.

Once the S&P 500 completes wave 5, a pullback that retraces at least 38.6% of the move up from 4270 is likely before a rally to 4900 or higher kicks in.

Dollar

The correction in the Dollar is progressing. The Dollar could drop to 93.00 (very likely) or 92.50 which is the 50% retracement of the rally from 89.54 to 94.56. The 61.8% retracement is 92.10.

Gold

Gold has been expected to rally up to $1835 but it first needs to get above the rising trend from the May 2019 low. That upward sloping line is near $1816 today and will continue to rise. Once Gold closes above this trend line a quick pop to the significant resistance at $1835 should follow. The key is getting above $1835 as that would open the door for a move up to $1880 – $1910. I’m inclined to be a seller if Gold nears $1900. Gold should hold above $1770 is this is going to play out. Gold traded down to $1773 on October 92. Traders are long the Gold ETF IAU from $32.94 and lower the stop to $33.50 from $33.60.

Silver

Silver spiked up to $24.76 and has so far held above important support at $23.50. A close above $24.55 should lead to a rally up to $25.30. SLV could reach $23.25 if Silver rallies above $25.00.

Gold Stocks

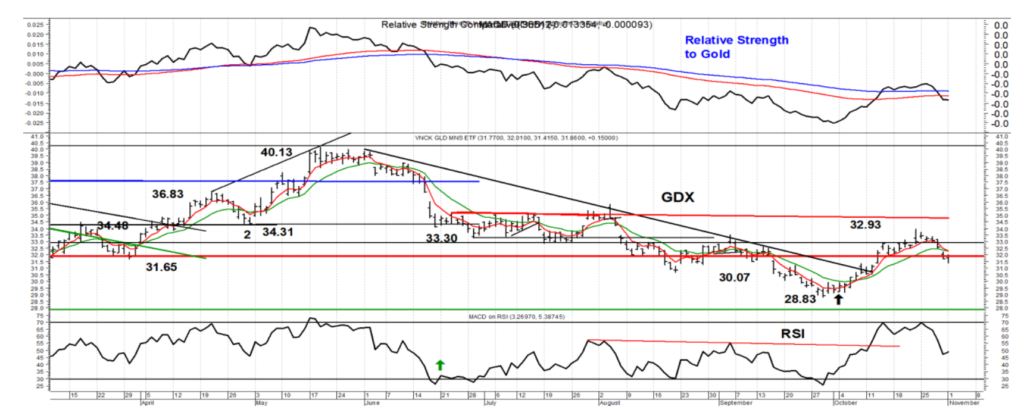

GDX has exceeded the resistance at $33.00 – $33.25 which suggests it can move up to $34.50, especially if Gold tests $1835. If Gold rallies to $1880 – $1910 GDX could rally to $37.00. I recommended GDX at $29.10 but it only fell to $29.17. There is a gap at $31.36 that GDX may fill before the rally resumes.

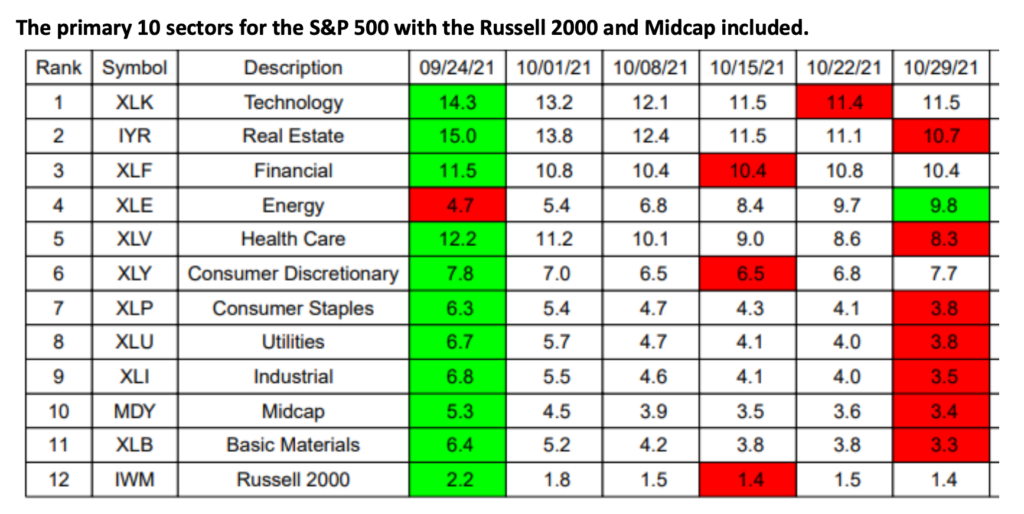

Tactical U.S. Sector Rotation Model Portfolio

Relative Strength Ranking

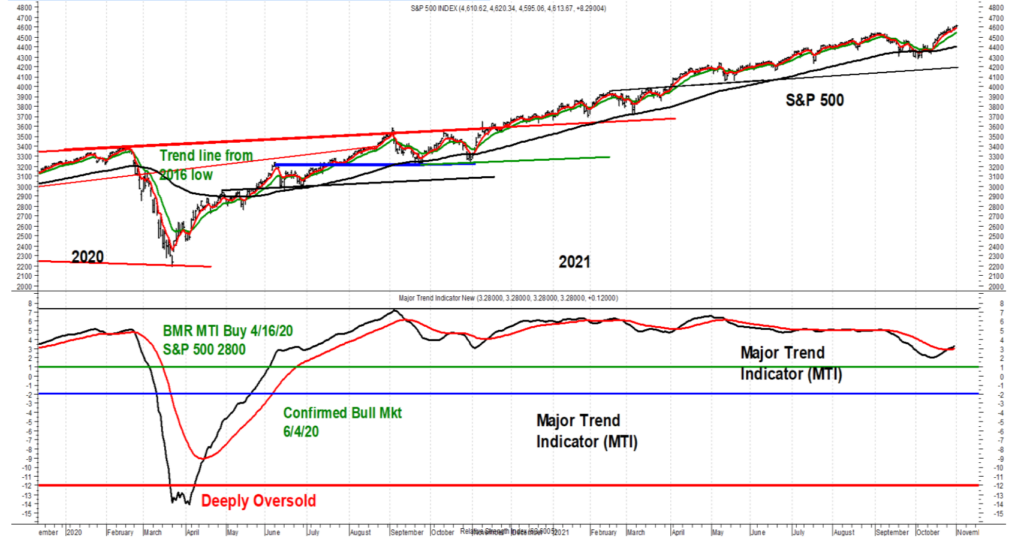

The MTI generated a Bear Market Rally (BMR) buy signal when it crossed above the red moving average on April 16, 2020 when the S&P 500 closed at 2800. A new bull market was confirmed on June 4, 2020 when the WTI rose above the green horizontal line. With the MTI still holding above the green horizontal line, the risk of a bear market is low. The decline in Q3 GDP is overstating the degree of economic weakness.

Macrotides.com

jimwelshmacro@gmail.com

20211102